Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Welcome to Week 1 of our three-part series on evaluating deals! Today, we’re covering the first of three key areas investors consider when they’re assessing an opportunity: the company’s overall market. We’ll teach by example, using some of the most common metrics top VCs and angels use as they conduct due diligence.

Before we jump in, a quick note: just because many experts look at a certain metric or quality doesn’t mean you need to do the same. Everyone’s approach to investing is a bit different, and it’s up to you to make it your own. Don’t take this as advice (it isn’t)–take it as one of many different perspectives you can use to form your own due diligence process.

Now, back to today’s topic. Any time you look at an investment opportunity on Republic, you should be able to find that company’s overview of the market they serve (or aim to serve).

First, let’s clear up the difference between a sector, an industry, and a market.

A sector is a wide-ranging segment of the overall economy. Some examples: energy, healthcare, technology, etc.

Within a sector, there are many different industries. So if we look at the tech sector, some industries might include consumer electronics, AI, robotics, and so forth.

Finally, a market is a specific audience or consumer base. For example, the market for a smartphone app might include all smartphone users.

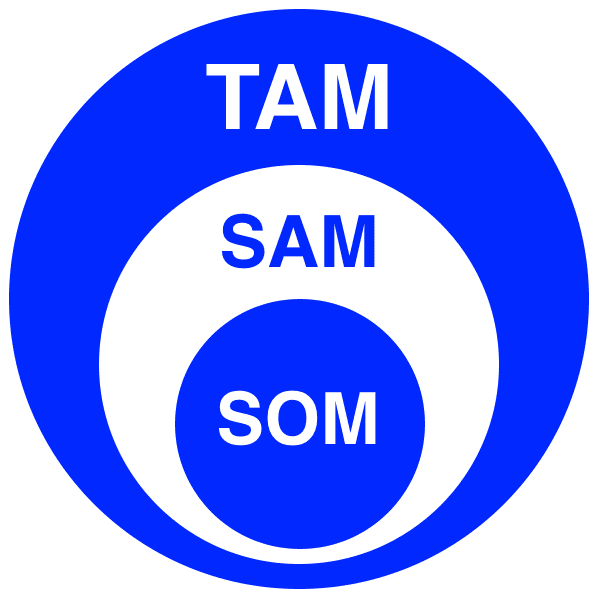

As you start doing your own market research, you might run into a few commonly-used acronyms. In case you aren’t familiar, here’s a quick rundown of what they mean:

Total addressable market (TAM): The size of the overall market, without any realistic restrictions in place. For example, if a company sells smart speakers for cars, the TAM might include every compatible car in the world.

Serviceable addressable market (SAM): This is the segment of the TAM that’s even possible for a company to go after, usually based on geographic location. So if this imaginary speaker company only sells its products in the U.S., the SAM might include every compatible car in the U.S.

Serviceable obtainable market (SOM): This is the portion of the SOM that a company can realistically reach. For our hypothetical example, this would only include compatible cars within the U.S., with owners who want and can afford smart speakers, and who the company is able to reach with marketing.

Not every offering page will use the same terminology… and not every offering will list out all three of those different market portions. You should, however, be able to find at least some mention of the market size–and from there, it may be worthwhile to do some digging of your own.

Today, we’ll cover three of the main things top VCs look at when evaluating a deal:

The size of the market a company operates in

Whether that market is growing or shrinking (and how fast)

And how many other players, or competitors, are angling for market share.

Let’s get started with the first question investors typically ask:

How big is the overall market?

It may sound obvious, but market size can be one of the most significant metrics angel investors use to choose (or rule out) opportunities. Simply put, the bigger the market, the more revenue a company can theoretically bring in, if all goes according to plan.

Think about it this way: let’s say that a hypothetical startup develops a new medication that can completely eliminate any headache within 30 seconds. According to the World Health Organization, up to three-fourths of all adults aged 18 to 65–over 200 million people in the U.S. alone–have reported a headache within the past year. That’s an absolutely massive potential market.

On the other hand, if that same startup developed a medication to treat an incredibly rare condition they’d probably be limited by the small number of potential customers they could serve.

Of course, overall market size is not a direct indication of a company’s future upside. However, it can be a useful starting point to conceptualize just how much growth is possible for the company.

Which brings us to another important point: early investments in startups typically mature over a long timeline. Exactly how long it might take for a company to go from seed funding to an exit event (like an IPO, merger, or acquisition) varies depending on multiple factors, like market conditions, what industry the startup is in, how experienced its founders are, and so forth.

In short: it’s impossible to map out an exact timeline for these types of investments, but most will take at least three to five years to mature. Which is why…

It’s not just about a market’s size right now…

It’s also important to think about how big that market will be months or even years from now.

Generally speaking, VCs like to see that a company’s target market is not just big today… but projected to grow steadily over the coming years as well.

Some (but not all) deal pages will tell you directly whether a company’s market is growing (and at what rate). Here are a few common abbreviations you might see used:

YoY (year over year): growth from one year to the next–e.g., 2021 vs. 2020

QoQ (quarter over quarter): growth from one quarter to the next–e.g., Q1 2022 vs. Q4 2021 vs. Q3 2021 and so on

CAGR (compound annual growth rate): the mean annual growth rate over a period of time longer than one year

Even if an offering page doesn’t list market growth, you can often find that data yourself by looking up market research for the company’s specific product or service. Some common sources of market data include Nielsen, Statista, and McKinsey.

Needless to say, more often than not, a shrinking market may signify some kind of shift in consumer behavior or demand away from that particular subsector. Still, many experienced angel investors (including Jason Calacanis) caution against using market size as the sole reason to turn down a deal.

As he once said on his podcast, this approach assumes that markets only grow and shrink over time… but fails to account for startups that drive the creation of new markets. Uber, for example, never really served the exact same market that traditional taxicabs did; rather, it carved out the brand-new ridesharing market, which grew to a value of more than $38 billion in 2021.

In short: as long as a company isn’t doing the same old stuff in a stagnant market, there may still be plenty of upside potential, if its product or service is unique enough.

Uniqueness is another key quality to look at when evaluating a deal—especially when it comes to established markets. This part of the process can be boiled down to a simple question:

How crowded is the company’s market?

In an ideal world, a company would be the only player operating in a massive market (billions or even trillions of dollars in size).

That kind of monopoly is incredibly rare. Even some of the world’s biggest companies have competitors—for example, Airbnb competes with Vrbo, Homestay, and others (plus indirectly with hotels, bed & breakfasts, and travel sites).

But when Airbnb raised its first round of seed funding, back in 2009, it was the only company offering both “standalone” vacation home rentals (meaning a customer would rent the entire property) and shared-space rentals (like the startup’s namesake: an air mattress on someone’s floor).

This is a great example of a competitive differentiator—some unique characteristic that separates a product or service from those already in the market. If a company isn’t actively creating new territory for itself, it’s vital to have one of these differentiators; otherwise, we’re talking about a small, early-stage company going after the same resources and customers larger, more established businesses have already claimed.

A competitive differentiator doesn’t necessarily need to be something as clear-cut as a 100% novel idea. Often, the reason that one startup succeeds while the others lag behind is much more nuanced. One of the most common reasons? Having the right leadership.

A great idea is only one part of the picture when it comes to running (and hopefully growing) a startup. No matter how promising an idea seems, any company needs a founding team that has what it takes to execute that vision.

In fact, studies show that founder skill is a significant factor when it comes to a startup’s chances of success. There’s a reason that the startup founders are stereotyped as visionaries with unbelievable hustle: that stereotype is an accurate portrayal of many of the most famous founders in history, including Mark Zuckerberg, Steve Jobs, Jeff Bezos, and many others.

Next week, we’ll dive into the many different ways investors assess a startup’s founding team.

Until then, click here to check out all our offerings closing between now and May 1st.

The discussion will appear here.