Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Opportunity

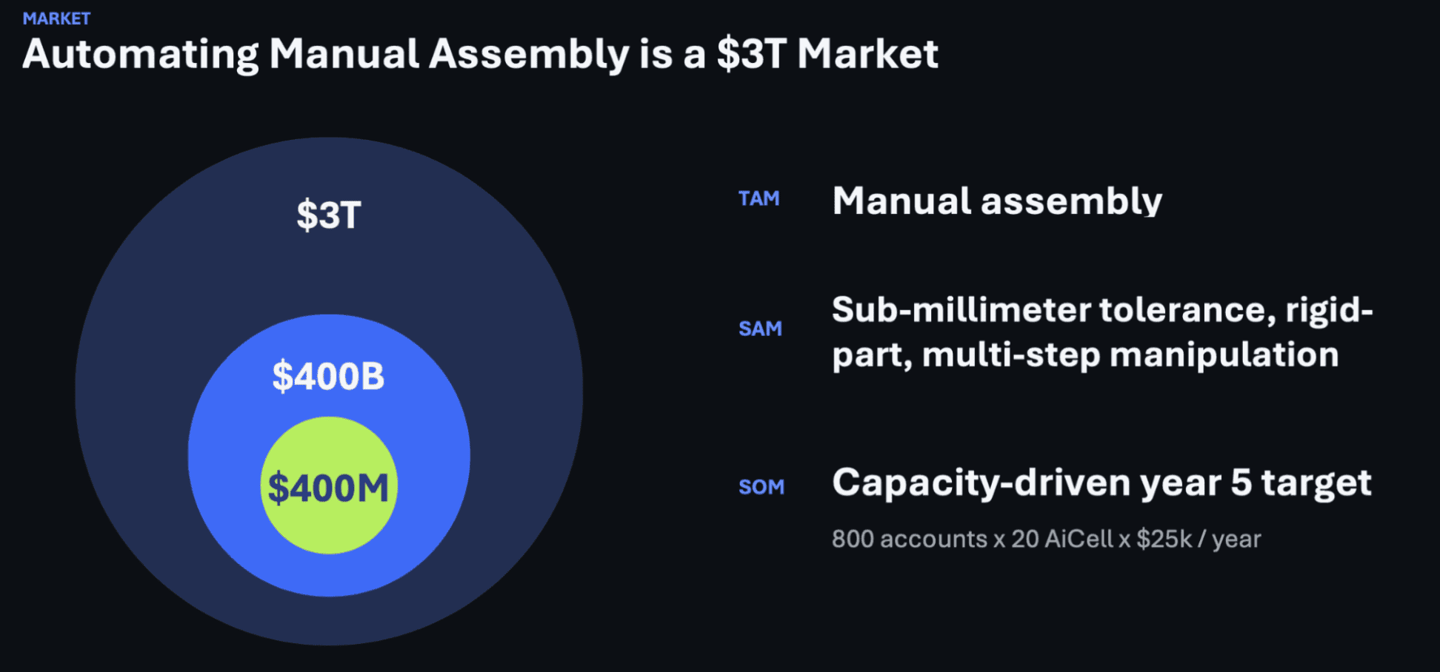

A $3 Trillion market is opening for flexible robotics

Global manufacturing faces a structural crisis. Up to 80% of production remains manual, yet the conditions that made manual labor economical are rapidly eroding. That’s in large part why 95% of manufacturers plan to invest in AI or machine learning by 2030.¹

Manufacturers need small-batch, build-to-order, onshore production. Traditional industrial automation is too rigid and expensive to deploy at that pace. Cognivix is the AI/computer vision layer that makes flexible automation economically viable.

The $3 trillion market for automating manual assembly includes a $400 billion serviceable market focused on sub-millimeter tolerance, rigid-part, and multi-step manipulation.

¹ Develop

Problem

Manufacturing is local, on-demand, and personalized

Manufacturers are under pressure to produce closer to customers, respond faster to demand, and support more product variation. That means smaller batches, frequent changeovers, and less tolerance for long automation setup cycles.

Traditional robot automation was built for stable, high-volume production. Deploying a new robotic task still requires programming, integration work, fixtures, tuning, and dedicated engineering resources. In mixed-volume production, the time and cost often erase the benefit.

Manufacturers lack a solution that combines the speed of software deployment with the precision of industrial robotics for this class of tasks.

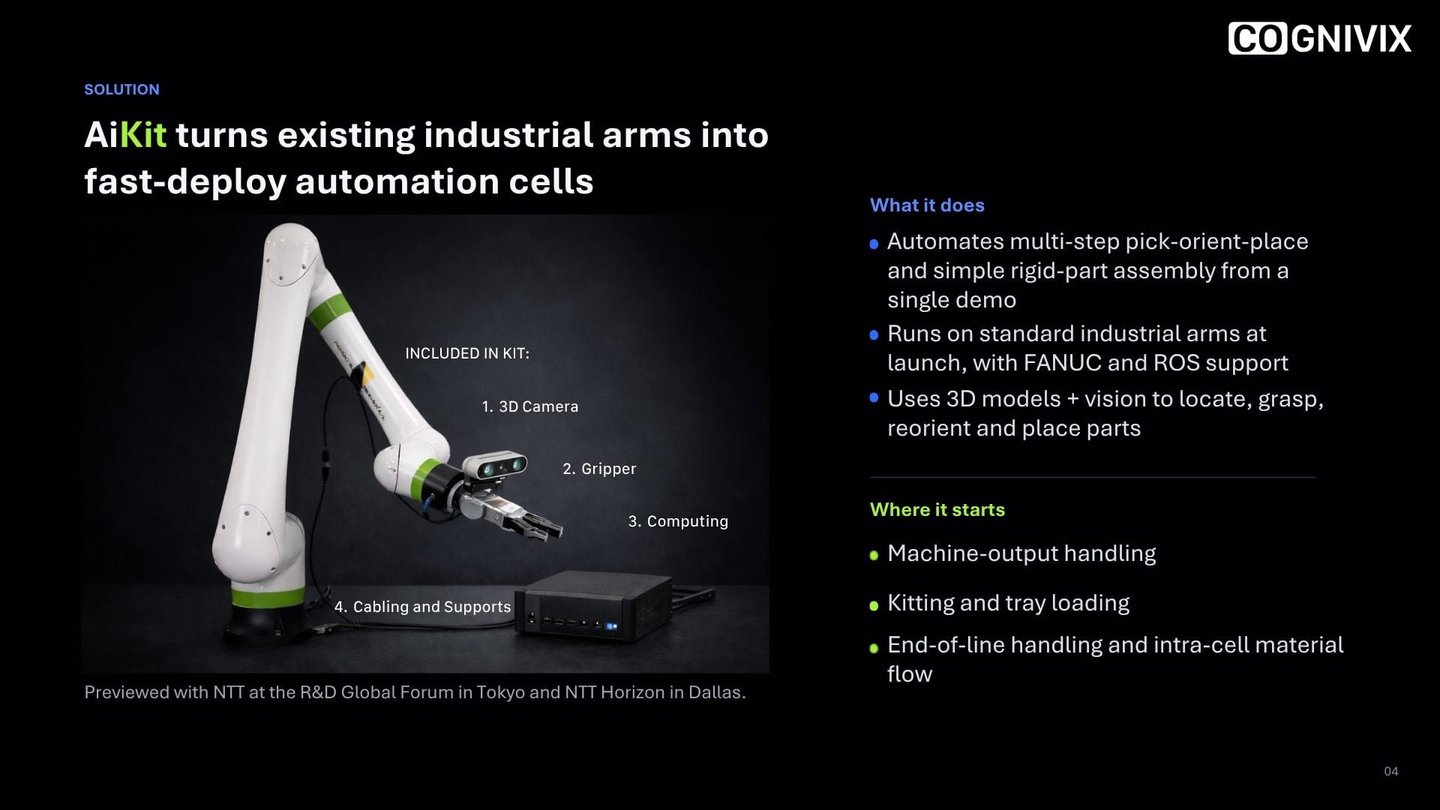

Solution

AI-powered robotics that learns from a single demonstration

Cognivix’s AiKit is a zero-integration OS that turns industrial robotic arms into fast-deploy automation cells without writing a line of code.

The workflow involves three steps:

A human demonstrates the assembly task once

AiKit uses the demonstration, 3D models and physical AI to extrapolate a manipulation sequence with sub-millimeter precision

Any demonstrated task is deployable across multiple robots within five minutes

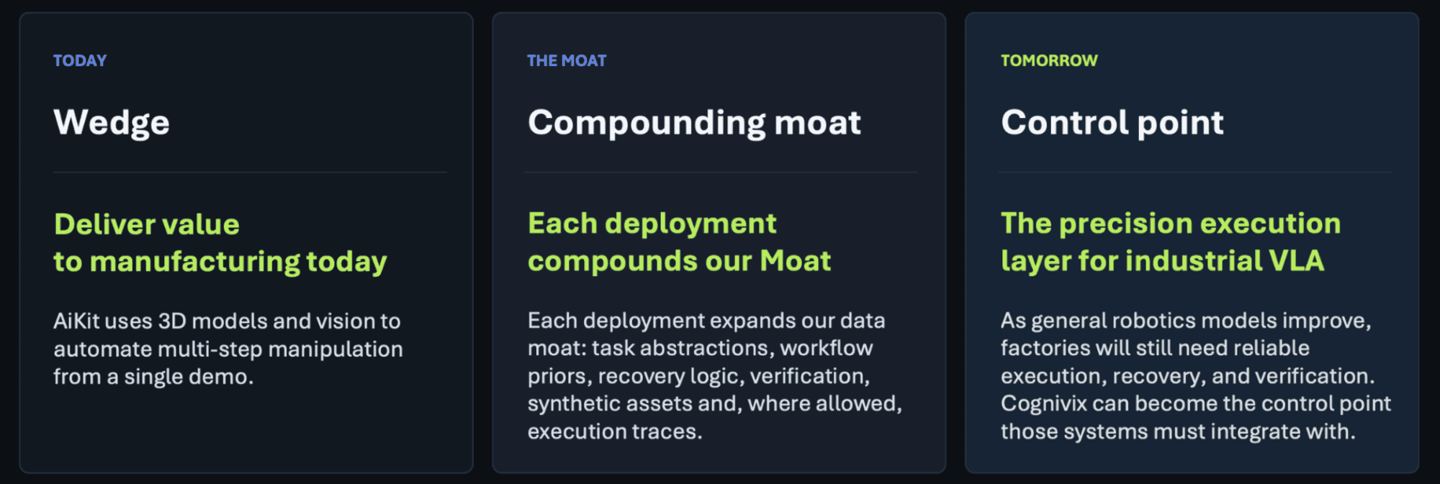

Roadmap

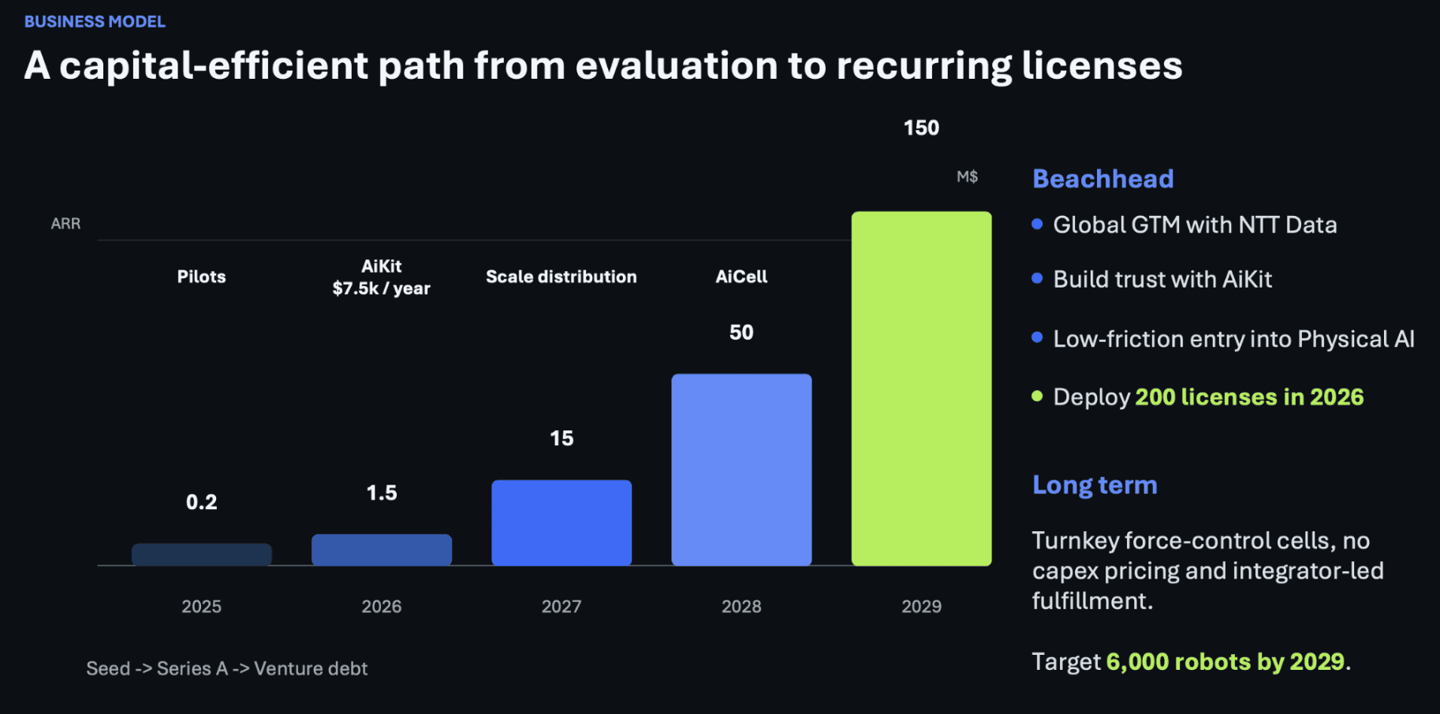

Targeting $150 million ARR and 6,000 robots by 2029

Cognivix’s vision is to become the precision execution control layer for industrial robotics.

Its 12-month execution plan is focused on three milestones:

- Shipping AiKit

Deploying 200 licenses

Reaching $1.5M ARR

From there, the roadmap expands distribution and product value:

2027: Launch the NTT Data global channel

2028: Introduce a higher-value AiCell product

2029: Target $150 million ARR and 6,000 robots

Business Model

A capital-efficient software model bringing Physical AI to industrial robots

Clients enter through the AiKit DevKit, a compact robotic development kit that lets manufacturers prototype, debug, and validate automation tasks offline before deploying them on production robots.

The DevKit includes three months of AiKit software and converts to annual per-robot licenses of $10,000 - or $7,500 after discount / reseller fee.

Cognivix generates recurring software revenue (ARR) without carrying the burden of enterprise sales or hardware fulfillment:

AiKit opens new applications that expand FANUC hardware opportunities

Enterprise sales are driven by NTT Data

Traction

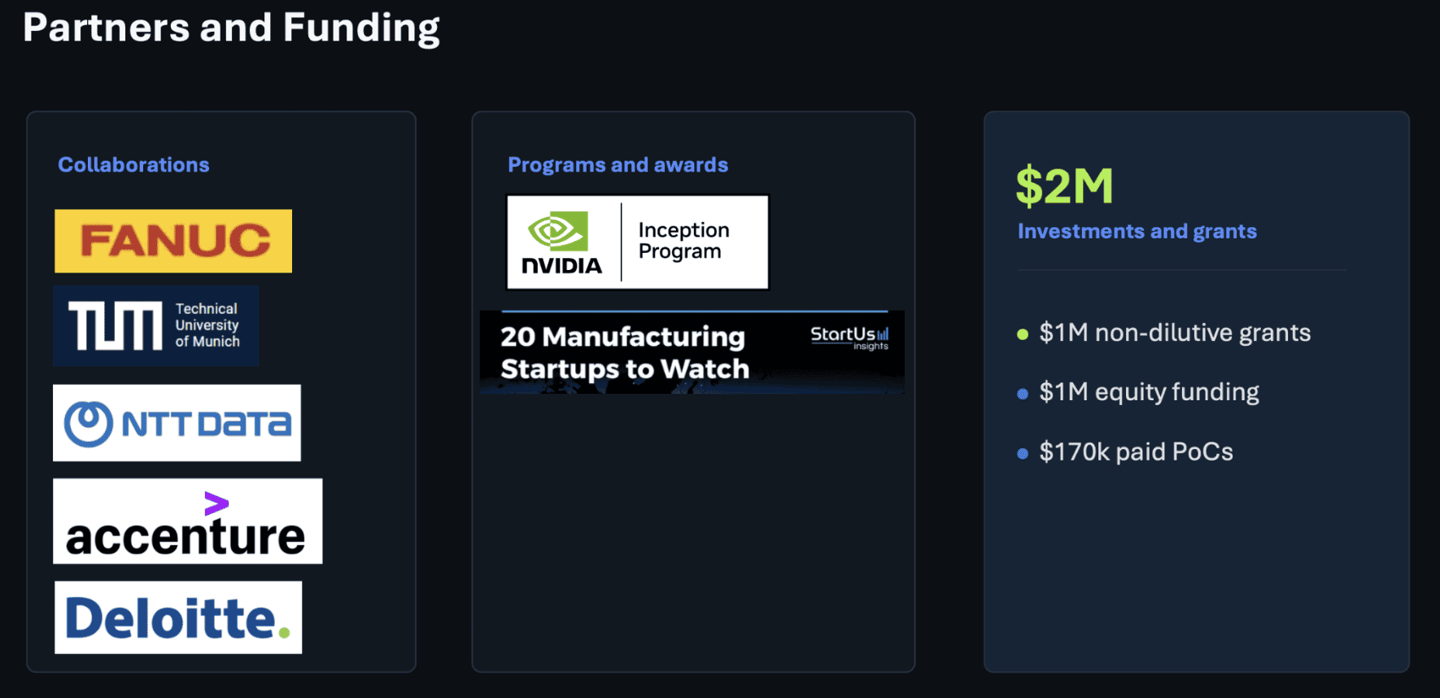

$2 million in investments and grants and multiple partnerships

Cognivix has secured $2 million in total investments and grants, including $1 million in non-dilutive grants and $1 million in equity funding, through its affiliate in Europe.

AiKit has been publicly showcased alongside NTT Data and FANUC at numerous trade fairs and events and validated through $170k in paid PoCs. As a member of the NVIDIA Inception Program, they were recognized as one of the “20 Manufacturing Startups to Watch.” by StartUs Insights

Collaborations span FANUC, NTT Data, Technical University of Munich (TUM), Accenture, and Deloitte.

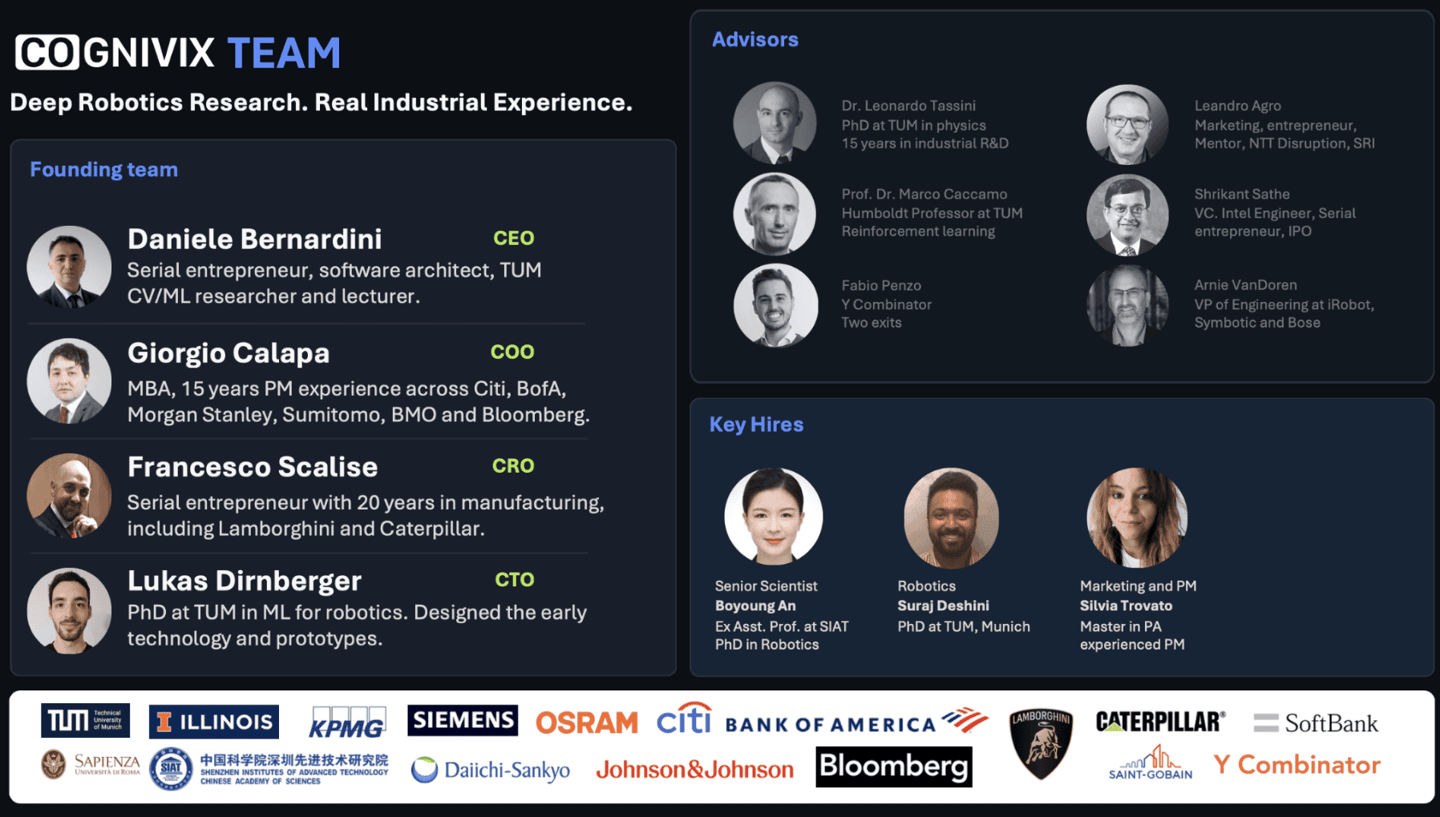

Leadership

Depth across robotics research, industrial operations, and enterprise commercialization

The founding team has collected decades of Industrial, Enterprise and R&D experience across Siemens, Caterpillar, Lamborghini, TUM, Citi, Bank of America, Morgan Stanley, Bloomberg.

Advisor bench includes a Y Combinator-backed founder with two exits, a SRI product expert featured in Wired and NYT, the former VP of Engineering at iRobot and Symbotic, and high profile operators from Venture Capital, Industrial R&D and Academia.