Austin's Top Chef competitor to open Mexican eatery in tr...

·

Apr 30, 2021

A taste of the Yucatan is coming to the Rainey Street District, care of an Austin-based top chef. Chef Gabe Erales, curre...

Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Explore new investment opportunities:

View companies raising now

A study in urban sophistication, 44 East Ave, a 49-story, 322-unit residential condominium has been designed to make the most of the unique location and to fully capture the spectacular views of Lady Bird Lake and downtown Austin — a bridge between the natural environment and the city. Every detail of each floor plan has been carefully considered and designed to take advantage of the expansive view from each home.

A multitude of gathering spaces comprise over 13,000 square feet of beautiful common areas and amenity spaces, all designed by award-winning architect Michael Hsu Office of Architecture. Outside, “green” exterior walls and massive heritage trees blend seamlessly with the lake, park, and Austin’s downtown.

The lobby is highlighted by the glass atrium which amplifies the neighboring park, water, and urban settings.

* All images are renderings

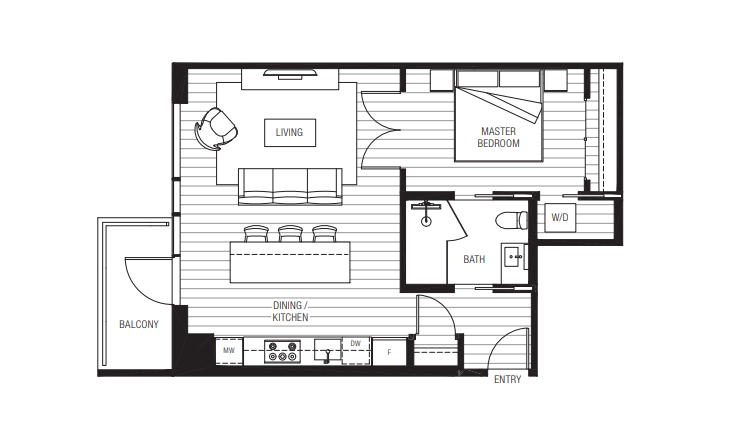

Unit #2211, a 768 square foot, one bedroom, one bath apartment with South-facing views of Lady Bird Lake.

The kitchen includes premium Bosch appliances with Itakraft millwork and cabinetry that is both elegant and more efficient than is typically found in condominium homes.

The elegant bathroom includes engineered stone tile blanketing the walls and floor.

* All images are renderings.

Unit 2211 | 768 Sq. Ft. | 1 Bedroom | 1 Bathroom

Unit 2211 | 768 Sq. Ft. | 1 Bedroom | 1 Bathroom

Compound is the easy way to build a diversified portfolio of beautiful apartments in some of the world's best cities. Compound slices each apartment into 100,000 equity interests so investors can realize the economic benefits of ownership without the hassles and headaches. Receive potential dividends from rental income and build wealth through potential appreciation.

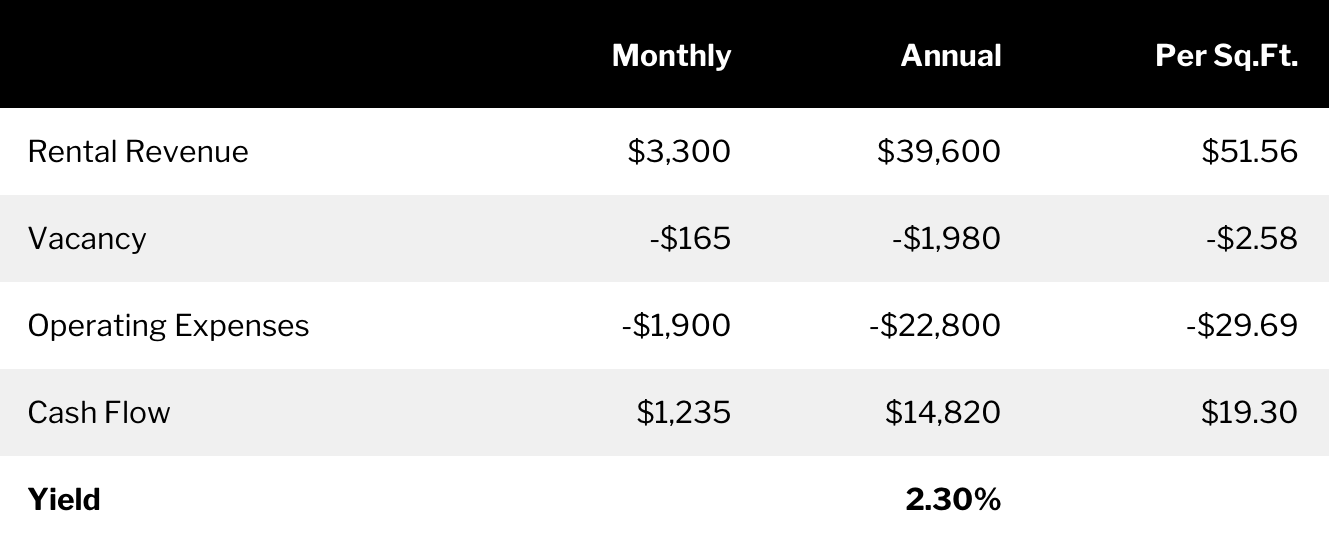

On January 7th, 2020 we entered into a purchase and sale agreement to acquire unit 2211 for $570,750. We have estimated a total capitalization for the acquisition to be $645,000 which includes closing costs associated with the purchase of the property, offering costs, (for this offering and other equity offerings), fees paid to Republic, and operating and capital reserves. In the event that we have overestimated the total capital required, we intend to distribute any excess capital to investors. The closing of the acquisition is expected to take place in the Fall of 2021.

Following the completion of the purchase and sale, we intend to lease the apartment and operate as a traditional rental unit. Once the property is rented, we intend to make semi-annual dividend payments based on cash available.

* All financial figures are estimates only. These estimates are not based on actual investment results and are not guaranteed of future results.

We intend to hold the property for a period of 3-5 years after we complete the acquisition. Total return on investment will consist of a combination of current income that will be received during the time we hold this property and capital appreciation that may be realized when we sell the property.

44 East Avenue, Austin, Texas

Austin is the "Live Music Capital of the World", the capital of Texas and also the home of the University of Texas at Austin. Over the past 25 years, Austin has emerged as a center for technology and business. A number of Fortune 500 companies have headquarters or regional offices in Austin, including Amazon, Apple, Google, and Whole Foods Market. Dell's worldwide headquarters is located in the nearby suburb of Round Rock.

Inc.'s recently published “50 Best U.S. Cities for Starting a Business in 2020,” Austin topped the charts at number one (which surprised nobody). Rankings considered a number of factors, including job creation, early-stage funding deals, and population growth, among other indicators.

It isn't just the corporate and startup types who love Austin, but plenty of celebrities are choosing to make Austin their homes, too. Matthew McConaughey, Ciara, Owen Wilson, Sandra Bullock, Lance Armstrong, Andy Roddick and Elijah Wood are long-time residents.

The Rainey Street Historic District is a neighborhood of historic homes, many of them bungalow style, in downtown Austin. Rainey Street is lined with craftsman houses that are actually bars, string-light covered patios, food trucks, craft cocktails, and a constant stream of people looking to party.

But fear not, Rainey Street has definitely not lost its charm; homey bungalows and fairy lights line the patios. This area embodies the ideal combination; giving you neighborhood feels and an itch to party all at the same time.

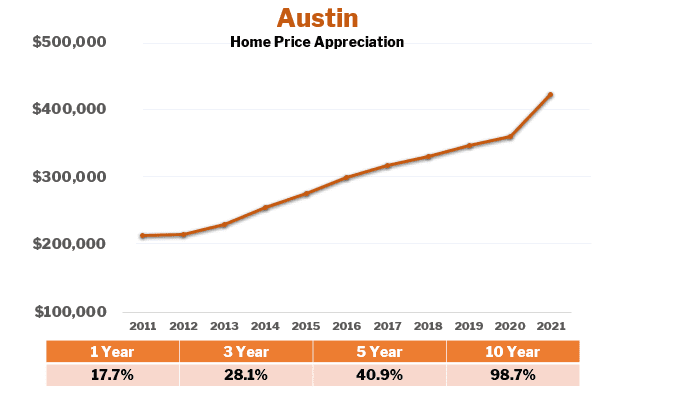

Home values in Austin have appreciated by 98.7% over the past 10 years including 17.7% over the past year.

* Zillow Home Value Index (ZHVI) for the Austin MSA: A smoothed, seasonally adjusted measure of the typical home value and market changes across a given region and housing type. Based on data as of 3/31/21.

$443.71K

44 East must achieve its minimum goal of $32.25K before the deadline. The maximum amount the offering can raise is $443.71K.

Learn more

Crowd IPA

Crowd IPA (Interests Purchase Agreement) is a simple agreement to acquire membership

units of a limited liability company.

Learn more

No additional cash outlays or capital calls are required. In the rare event that shortfalls exceed the reserves, then Compound can lend money to the project to fund the shortfall.

Compound does not charge any asset management fees. We also do not take a piece of the profits.

At the end of every year, investors will receive an annual 1099-DIV.

Compound typically engages local property management firms to handle leasing and day to day property management. In addition, most of our properties are in full service condominium buildings that provide maintenance services.

You are investing in a single condominium unit, the ownership of which has been divided into 100,000 equity interests. For example, if you buy 10,000 interests, you would own 10% of that condominium’s stock.

Compound Asset Management, LLC ("Compound"), a subsidiary of Republic Real Estate, is a real estate asset management company led by an experienced team of real estate veterans. Compound is the managing member of Compound Projects, a real estate investment company that acquires and manages residential condominiums in major U.S. real estate markets.

Invest in the app