Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Problem

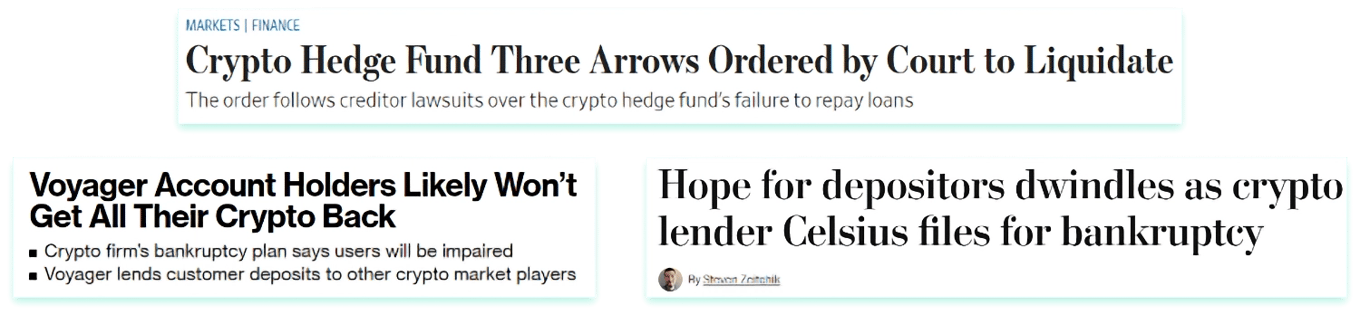

Credit market failures

Large lending businesses are opaque institutions, and historically relied on as trusted credit experts. On the back of market failures, credit market structure is rapidly changing:

- Demand for Transparency

- Elevated Underwriting Standards

- Risk Management Optionality

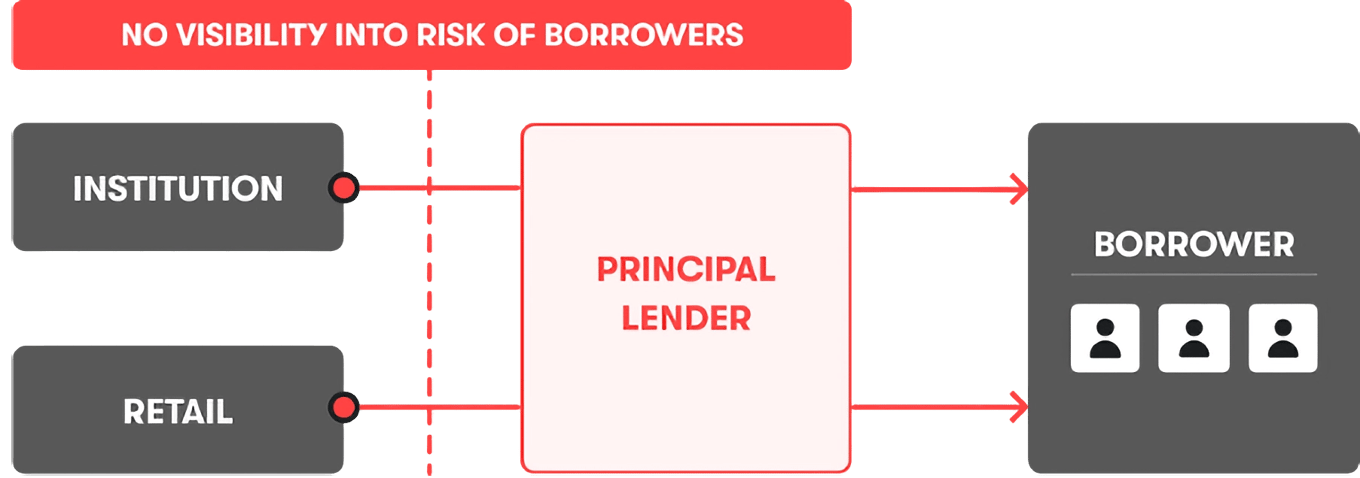

Current uncompetitive & opaque market |

|---|

|

Solution

Credora is an end-to-end lending solution

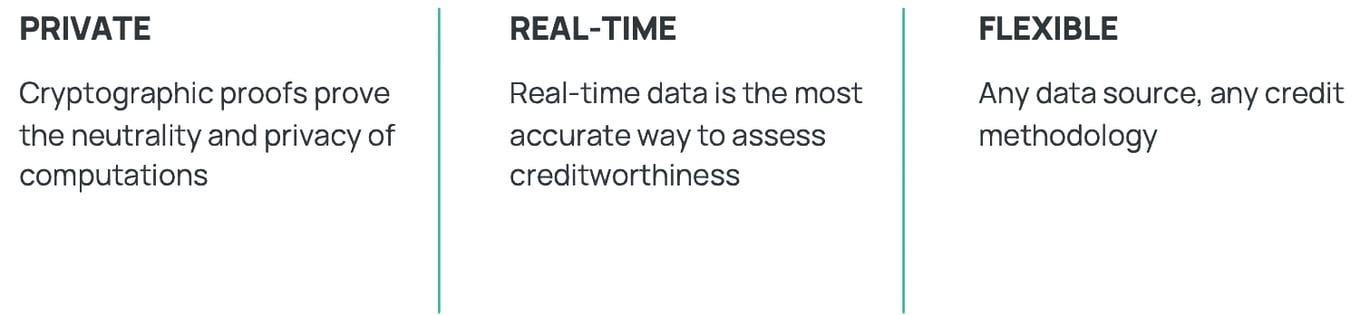

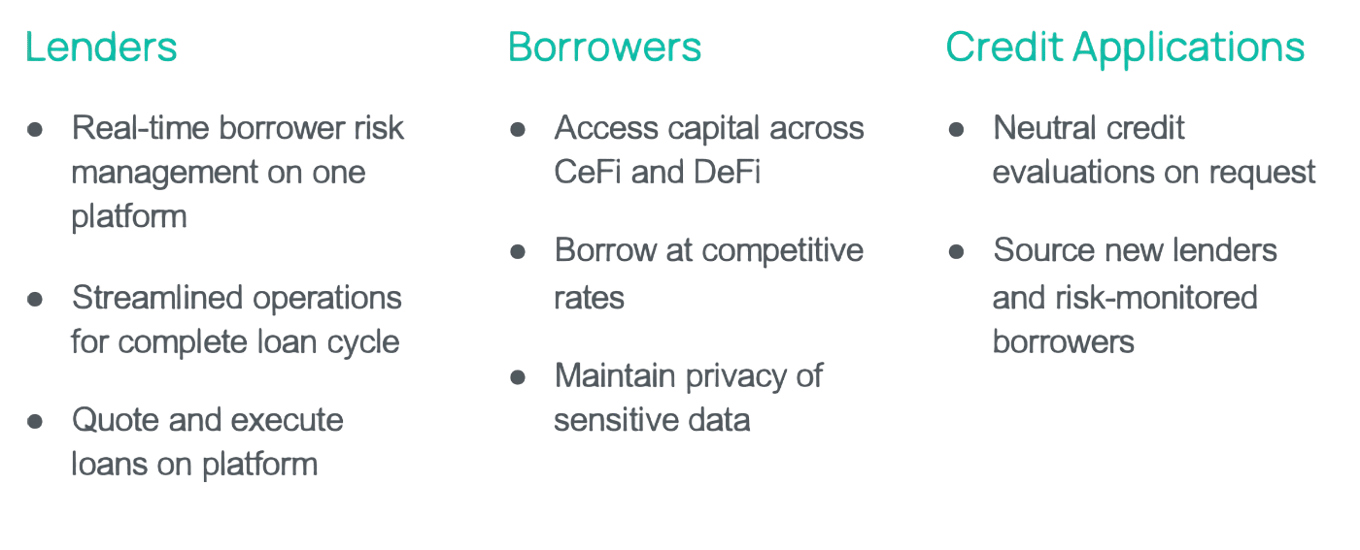

Credora is a technology company that enables superior credit risk management in crypto and ultimately traditional markets. Their product facilitates comprehensive and real-time counterparty credit risk assessments using provably private and neutral infrastructure.

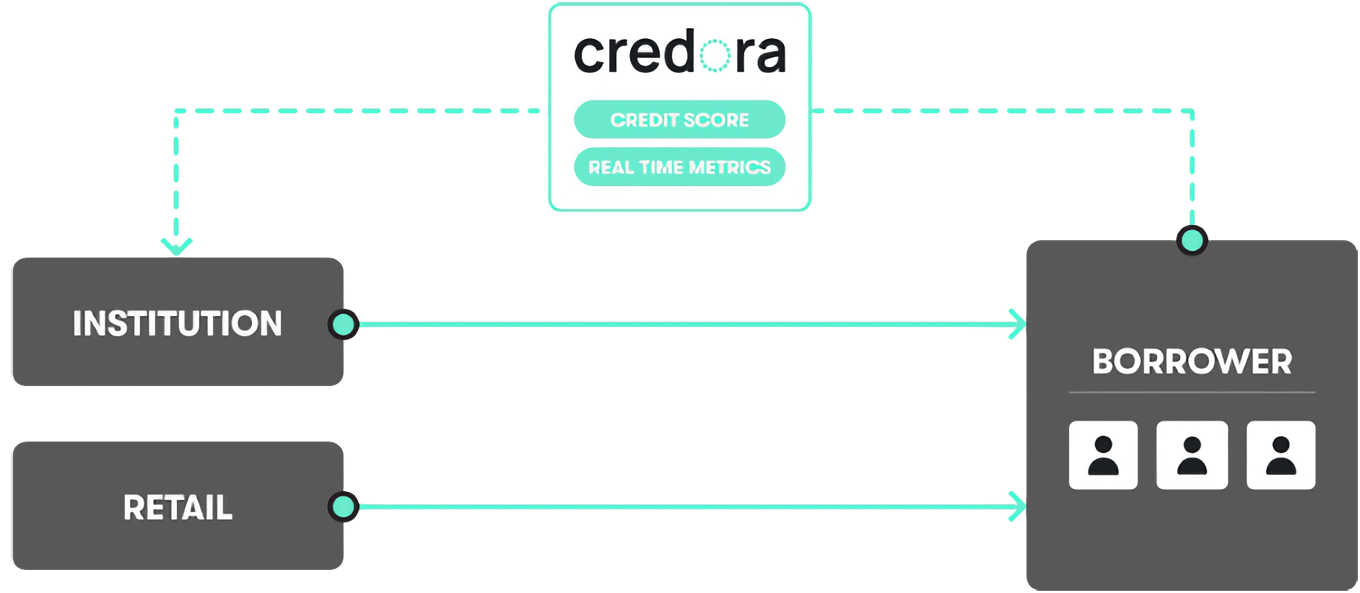

Private "Credit Oracle" unlocks secure undercollateralized lending |

|---|

|

Credora reimagines market dynamics |

|---|

|

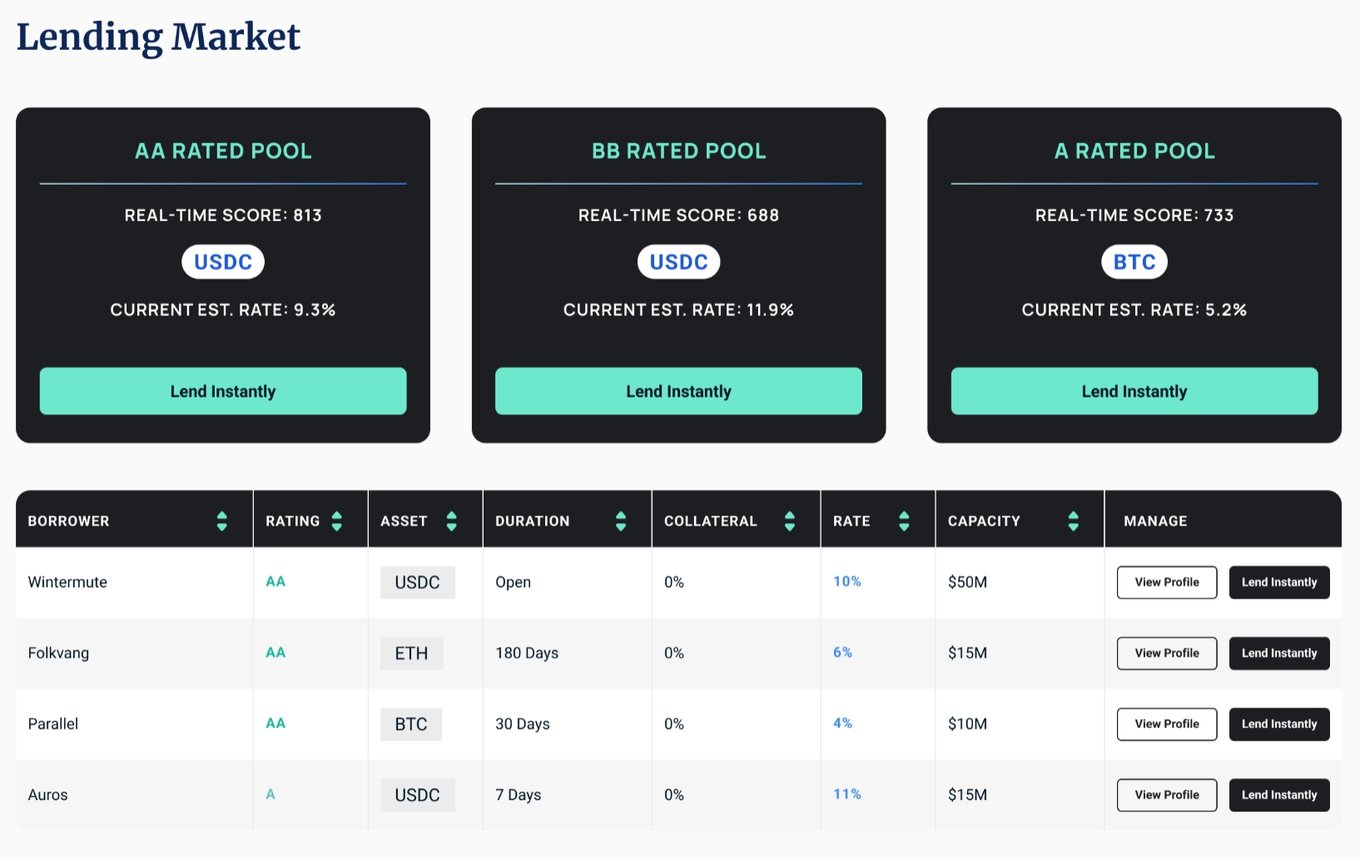

Product

A unique data-driven platform

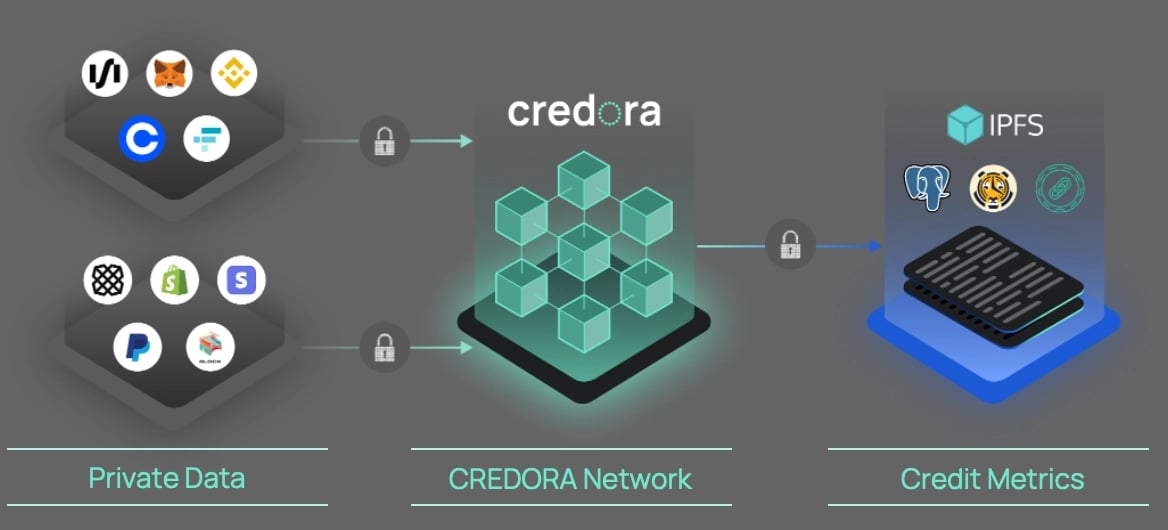

Capturing real-time data distinguishes Credora from traditional lending businesses. Credora aggregates KYB information, financial statements, and real-time portfolio information on borrowers, running only a specific set of computations on granular data while keeping it completely private. For trading firms, trade and portfolio information is incredibly sensitive. They analyze this information directly from the venues, and cryptographically validate privacy.

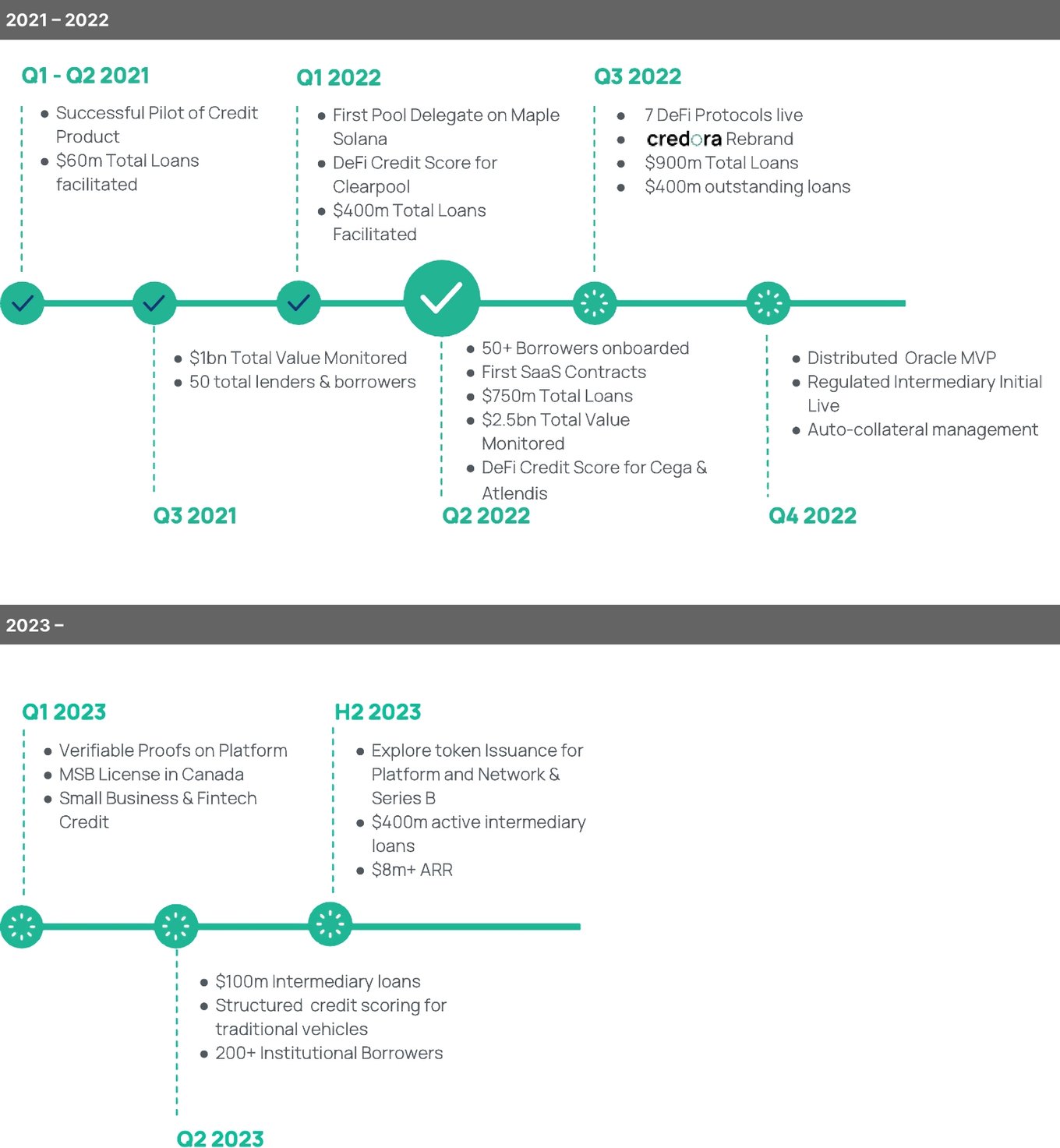

Credora operates a Maple Solana pool (operating as a Pool Delegate), and provides credit metrics for multiple protocols (operating as a Credit Oracle), including Clearpool, Ribbon, Atlendis, and dAMM.

Credora operators can pull any data source and run any credit methodology |

|---|

The Credora Infrastructure combines fast privacy-preserving calculations inside secure enclaves, proving neutrality and privacy using cryptographic proofs.  |

Over the past year, Credora sought partnerships with credit protocols to create a more transparent credit infrastructure. Protocols allow capital allocators to better understand their ultimate exposure. In comparison to the CeFi lenders, the construction of a loan portfolio is publicly visible. Alongside credit protocol partners, Credora quantifies the risk of an individual borrower through the distribution of credit metrics. The Credora rating methodology is public, and currently, they are on the 6th version of it.

Credora's end-to-end lending solution |

|---|

|

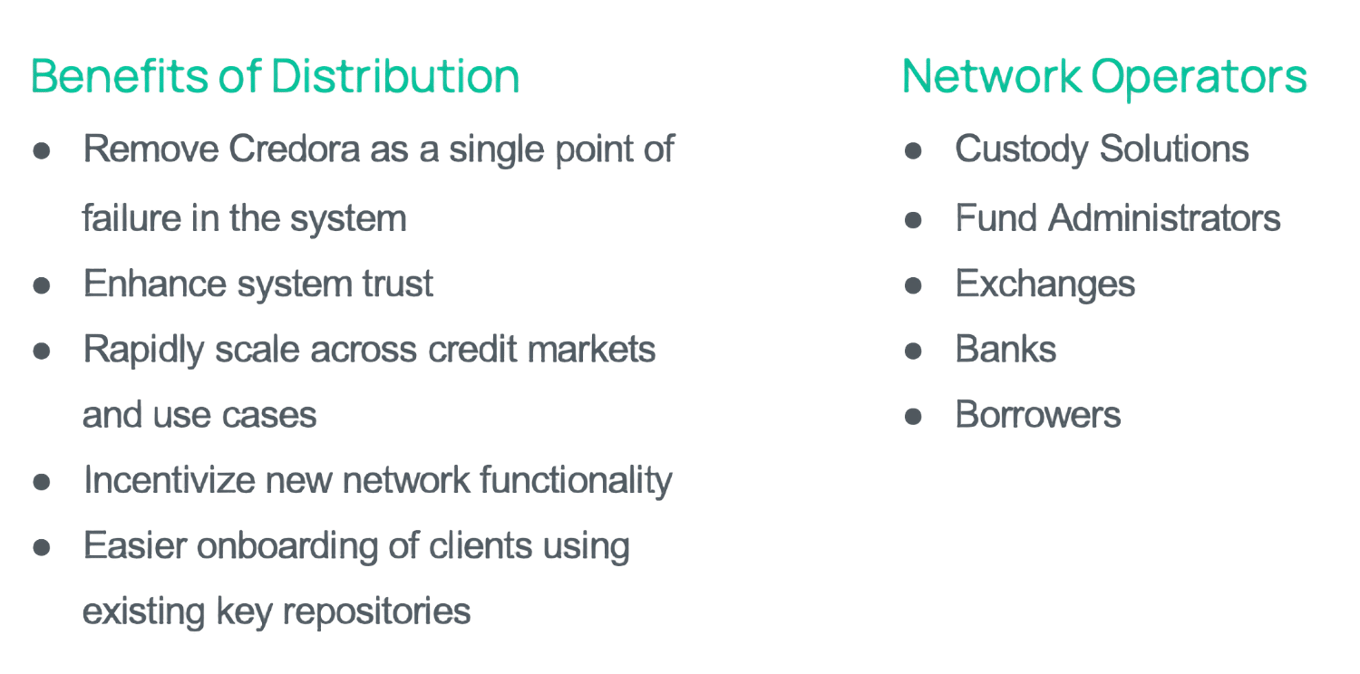

The Credora Network: Robust proofs allow others to run Credora nodes |

|---|

|

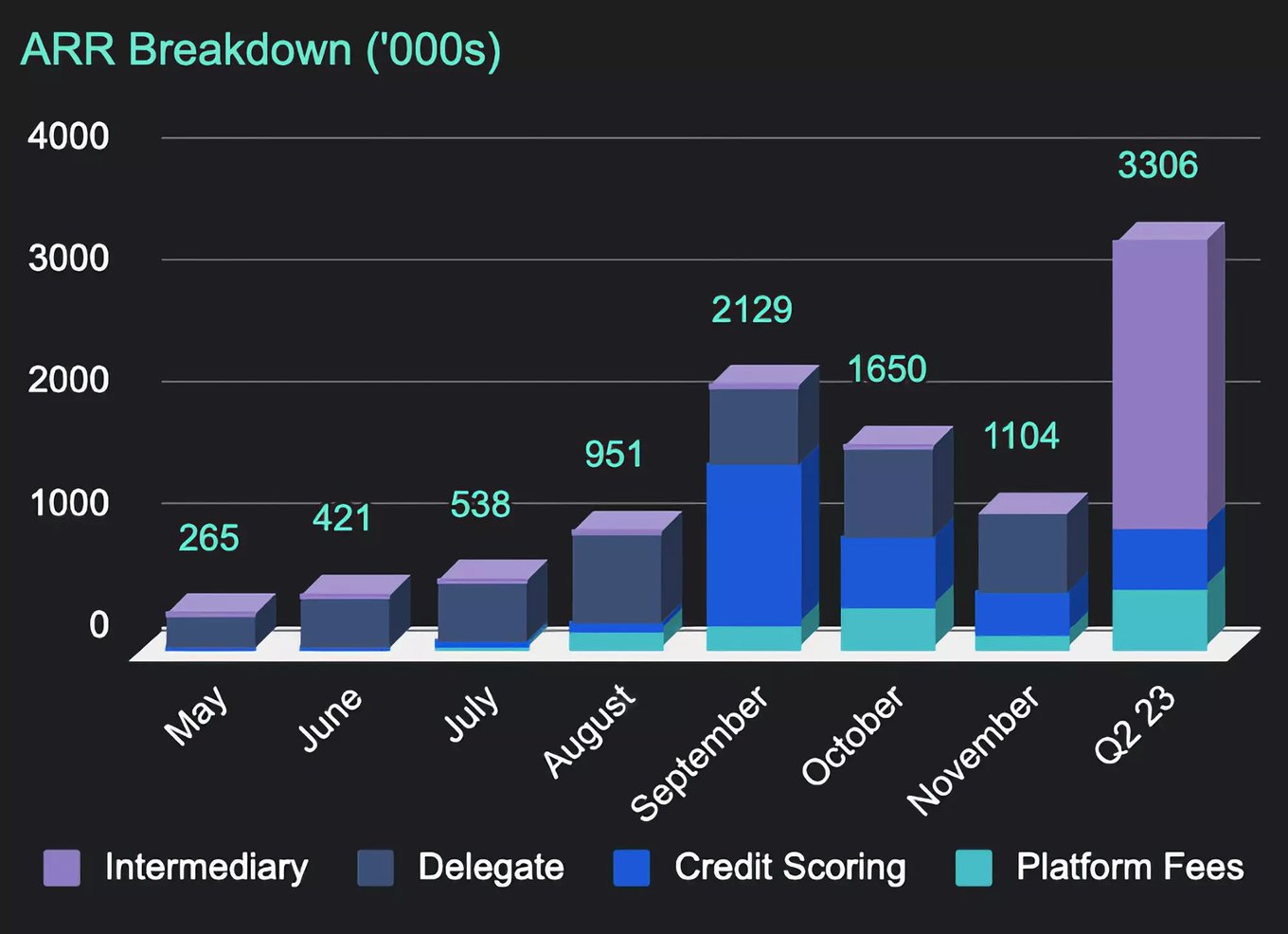

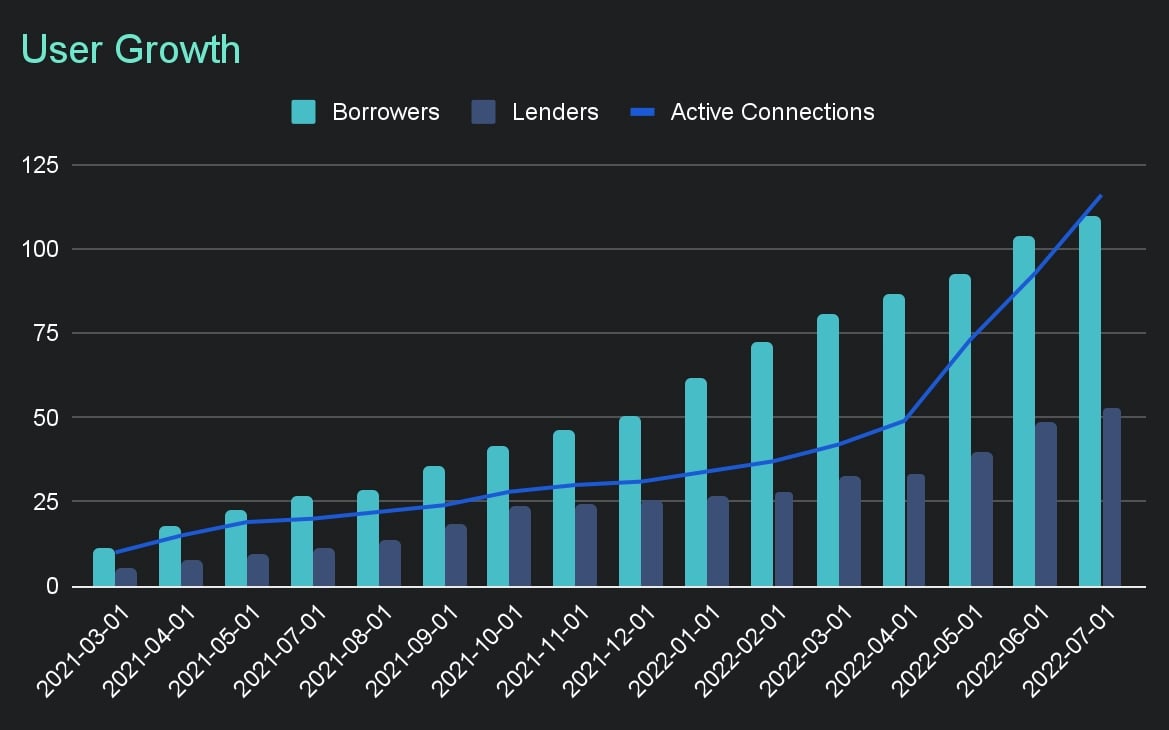

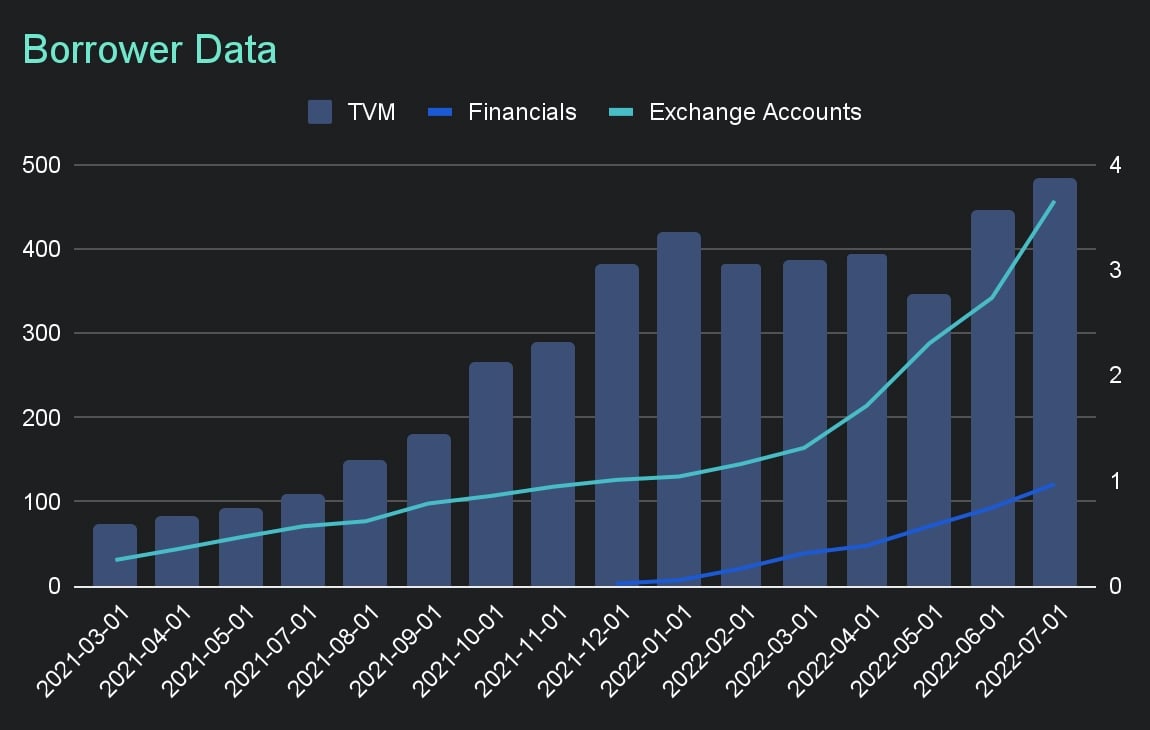

Traction

Revenue, user growth, & volumes continue to scale in a challenging market

Credora currently has 80 borrowers, 25 lenders, 25 CeFi integrations, and 16 DeFi integrations. They have facilitated $1B in loans and monitor $4B in assets.

| Credora users |

|---|

|

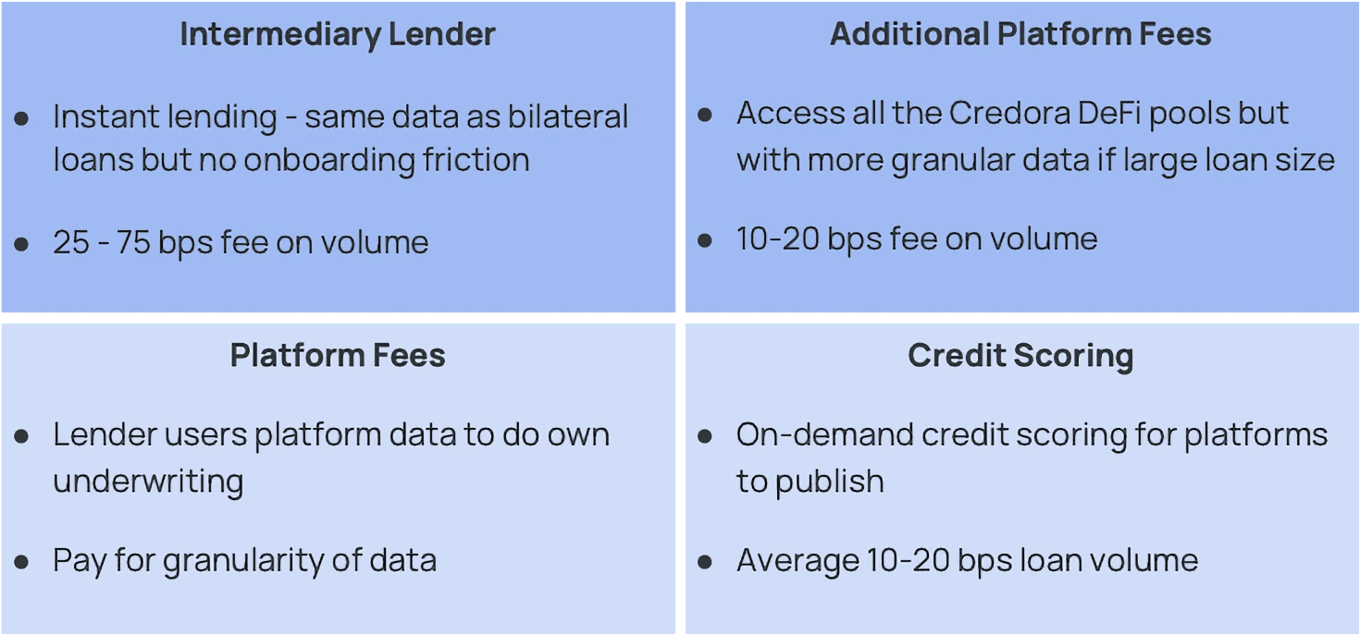

Business model

Sticky data allows Credora to upsell users on additional services

Intermediary for institutional lending |

|---|

Bermuda DABA License (Q4 22) allows Credora to be regulated intermediary.

|

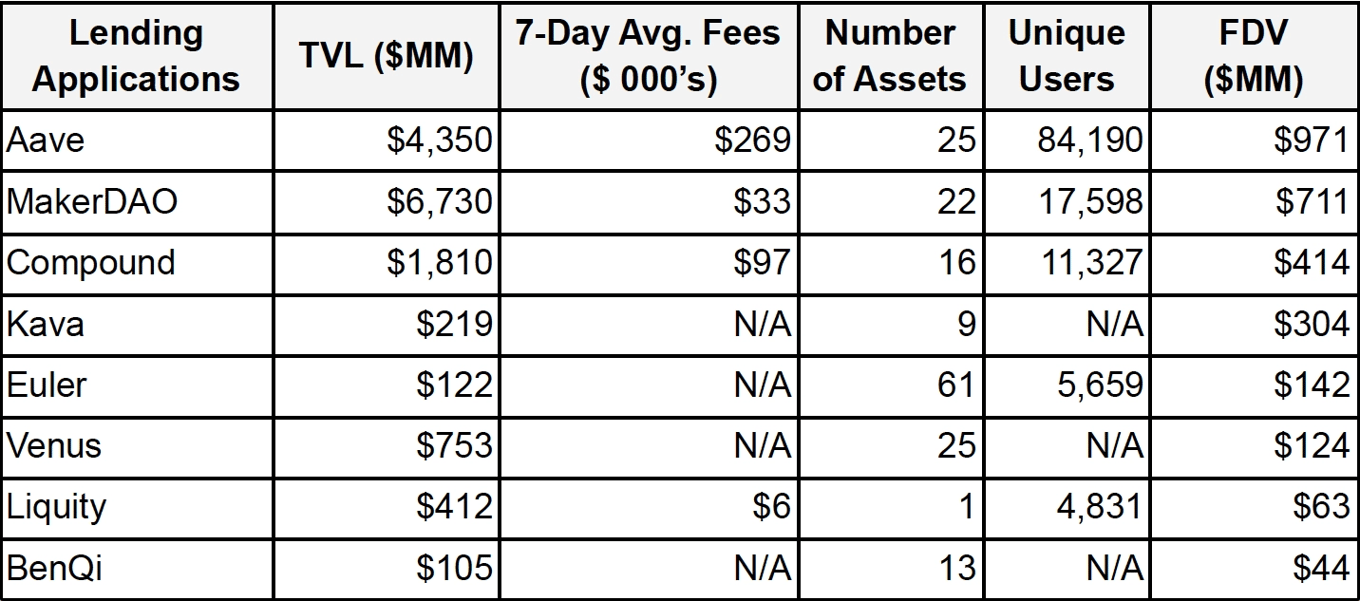

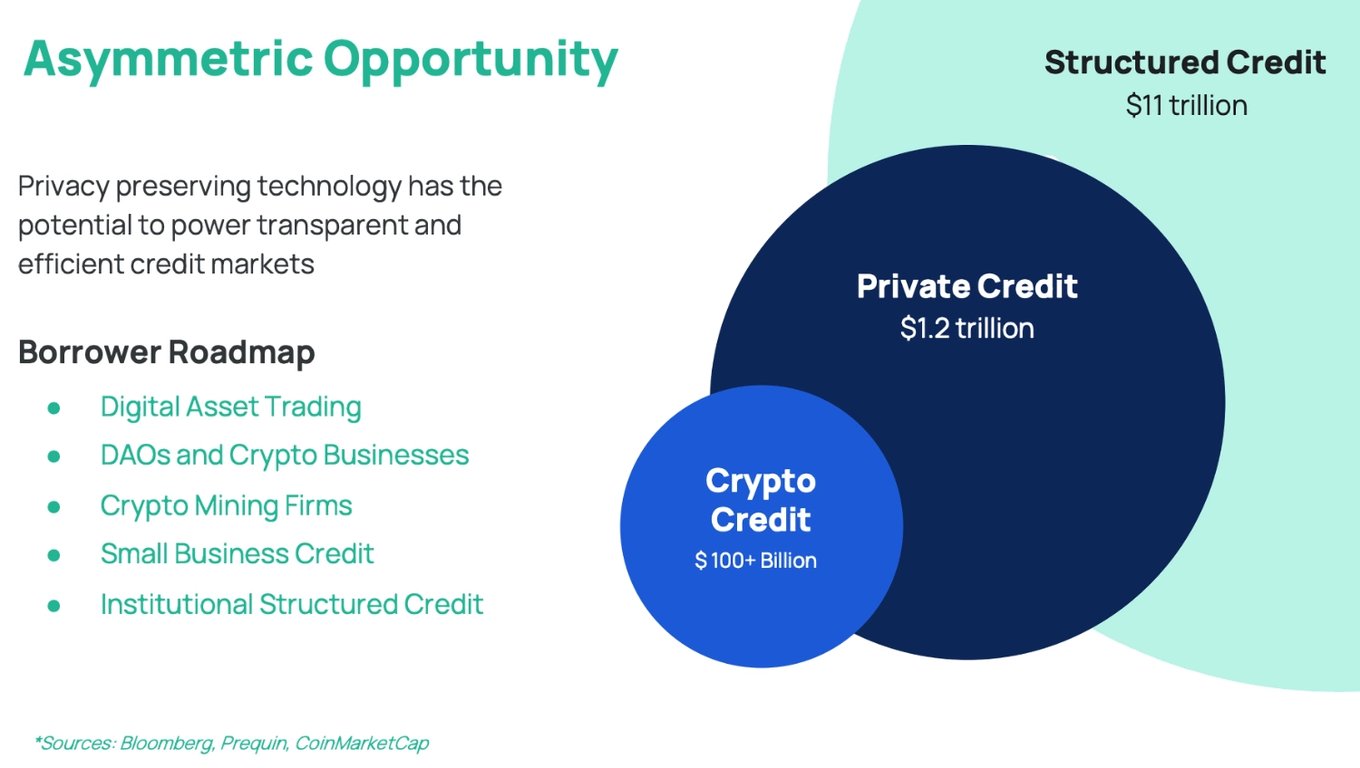

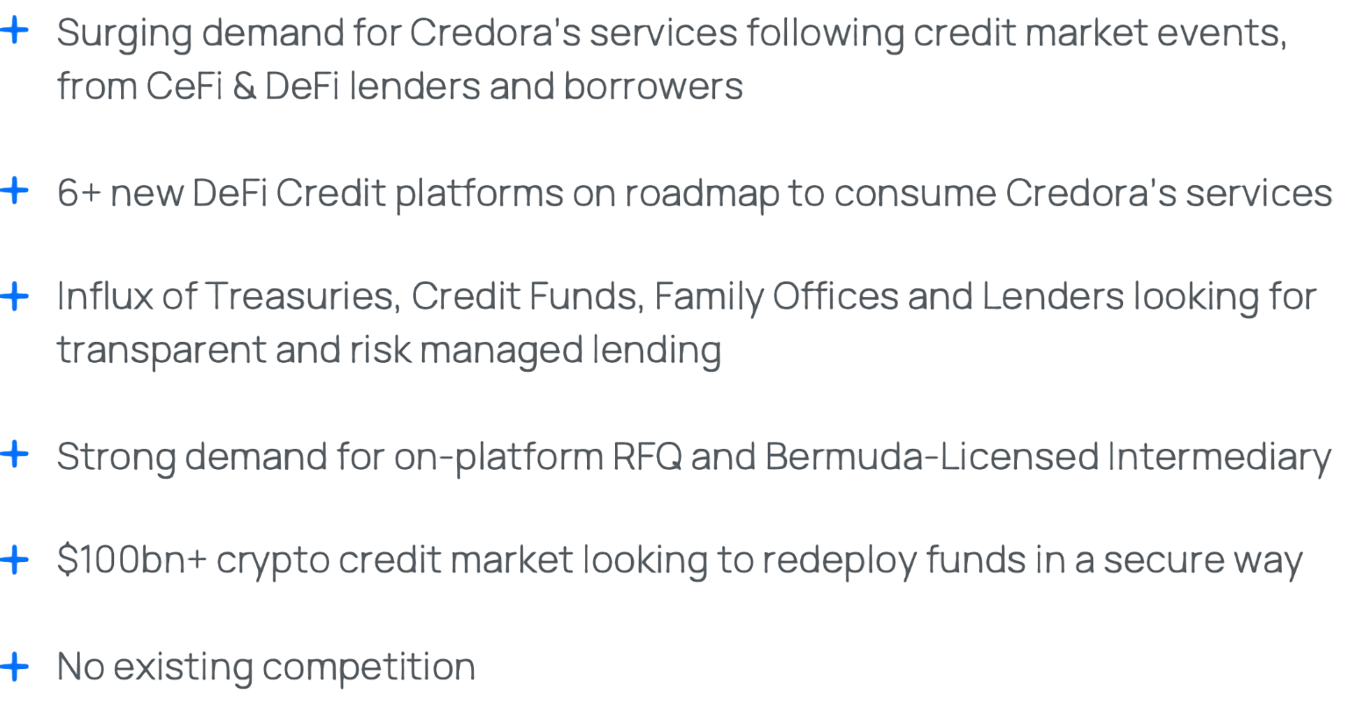

Market

Market Size / Industry Landscape

There is enormous demand and need for lending and borrowing within the crypto ecosystem as evidenced by the sheer amount of TVL and borrowing happening on major lending platforms. Moreover, a major pain point within crypto is that uncollateralized lending is difficult due to the anonymous/pseudonymous nature of the blockchains. Below are some of the largest lending platforms operating in crypto today.

Beyond using Credora as an oracle for credit scores, the technology can also be applied to other industries and verticals. For example, Credora could be used for ratings, audits, and credit quality reports that Moody’s and S&P currently perform.

Competition

Unique positioning

Credora has a unique advantage since it’s the one and only credit score provider in the DeFi space. In a short period of time, they have established themselves as the market leaders and have facilitated over $785M in loans, monitor over $3.85B in TVL, and integrated with 25 CeFi institutions and 16 DeFi platforms. In addition to their strong traction, Credora has also built some impressive technology built around zero-knowledge proofs that increases transparency and reduces credit risk while protecting the privacy of sensitive data. This technology stack will hopefully provide them with a competitive advantage while also allowing them to expand into other segments..

Risk factors

- There will likely be increasing amounts of competition in this space, not just from other credit scoring firms, but also other zero-knowledge based oracle solutions

- Beyond crypto, there will also be increased competition from traditional firms entering the space who have much stronger brand recognition and operate in a fully-regulated manner

Vision and strategy

Credora has three major growth drivers

1. Credit Scoring

- Becoming the market leader for credit scores within crypto and a core piece of infrastructure that lenders and borrowers rely on for debt.

- Credora charges a loan facilitation fee based on the volume of loans that it helps to facilitate, so as crypto lending grows, Credora will benefit as well

2. Alternative Financial Scoring

- While credit scores were the first implementation of Credora’s technology, theoretically the mechanism can be generalized to produce other types of scoring or audit reports - e.g., audits, credit quality ratings, proof of reserves, etc.

3. Data Monetization

- As Credora integrates with more crypto protocols and facilitate increasingly more loans, it will begin to create a database of financial data, which it can then monetize and charge fees on

Future Credit Facility Marketplace

With DCG’s Genesis declaring bankruptcy a better model needs to replace its centralized trust based borrow/lend facility. There are still and there always will be demand for borrowing and lending not just in the digital asset space. As time goes by Credora is looking to enter the traditional finance marketplace as well. Credora has now gotten licenses in Canada and Bermuda to become the next place facilitating these loans in a trust minimized and safe way with their ZK innovation.

| New paradigm for credit lending |

|---|

|

Funding

Series A extension

$7M round with $5M raised.

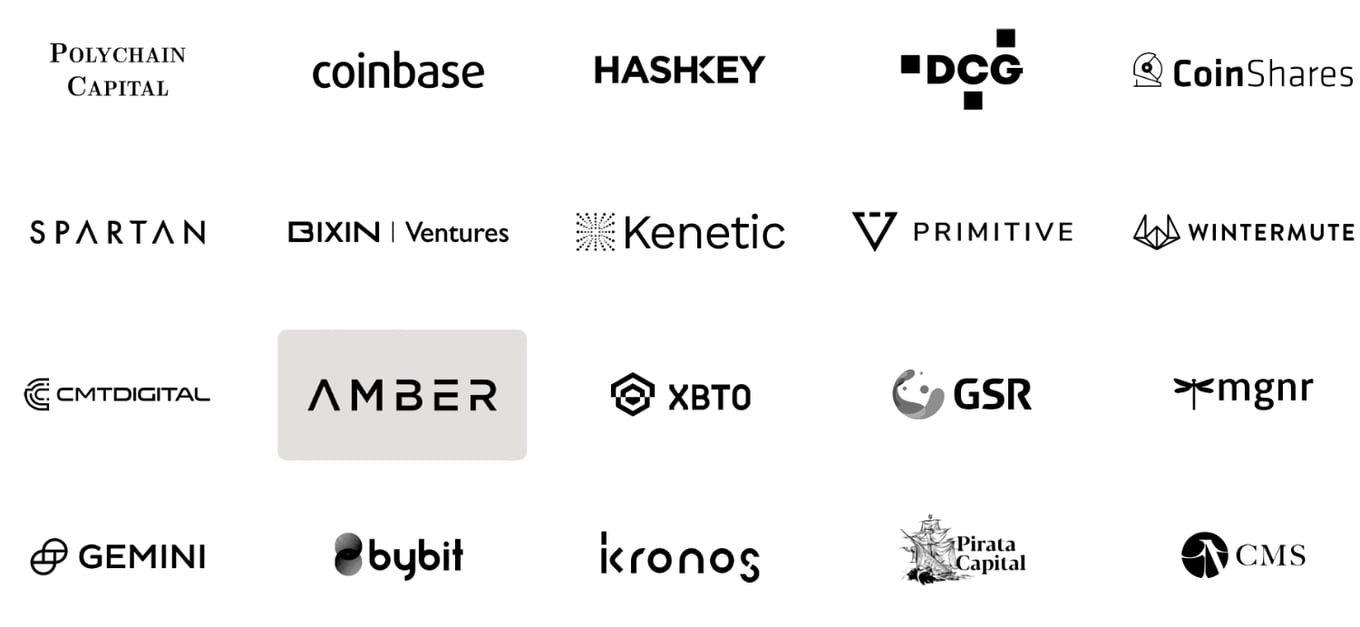

- Series A Lead: Coinbase, HashKey, Spartan Group

- Others: Polychain, Primitive, MGNR, Kenetic, CMS, GSR, Wintermute, Pirata Capital, Kronos Research

Founders

Darshan Vaidya, Co-Founder & CEO

Darshan began his career as an oil options trader at UBS and then went on to be a market maker at Mako Global where he traded options on the Euribor, Sterling, and Eurodollar options, trading longer-dated and Mid-curve options. He then left to join Magpie Capital as their CIO where he ran the market making and derivatives trading operations for the fund, offering bespoke hedging for large institutional cryptocurrency clients through options & swaps. While at Magpie, he also built & managed the algorithmic strategy for the fund, offering liquidity across various cryptocurrency derivatives exchanges.

Matthew Flicke, Co-Founder & COO

Matthew began his career as an intern at Cantor Fitzgerald where he was in the Intellectual Properties Division. He then went on to be an FX Trader at Morgan Stanley where he traded Asia Ex-Japan Spot, Forward, NDF, and G10 Spot. Matthew was most recently at OKCoin where he was their Head of Capital Markets.

Arne Hollum, Co-Founder & CTO

Arne began his career at Stagiair (ING) where he was working on Applied AI and Machine Learning in Fixed Income trading and building a Multi-Objective optimization and automated RFQ negotiation system. Afterwards, Arne joined m-wise where he was a Senior Data Modeler before going back to ING to work as a quant trader/developer.

|