Meet Jet Shark: The four-seater semi-submersible boat

·

Mar 6, 2023

Custom boat builder Rob Innes has revealed his newest semi-submersible boat, the Jet Shark Model Q.

Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Explore new investment opportunities:

View companies raising now

Jet Shark brings the three dimensional capabilities of an aircraft to the boating world, allowing people to enjoy the ocean the way aquatic creatures do. Jet Shark is not a submarine that slowly "sinks" beneath the water. Instead, it "flies" underwater, remaining positively buoyant at all times.

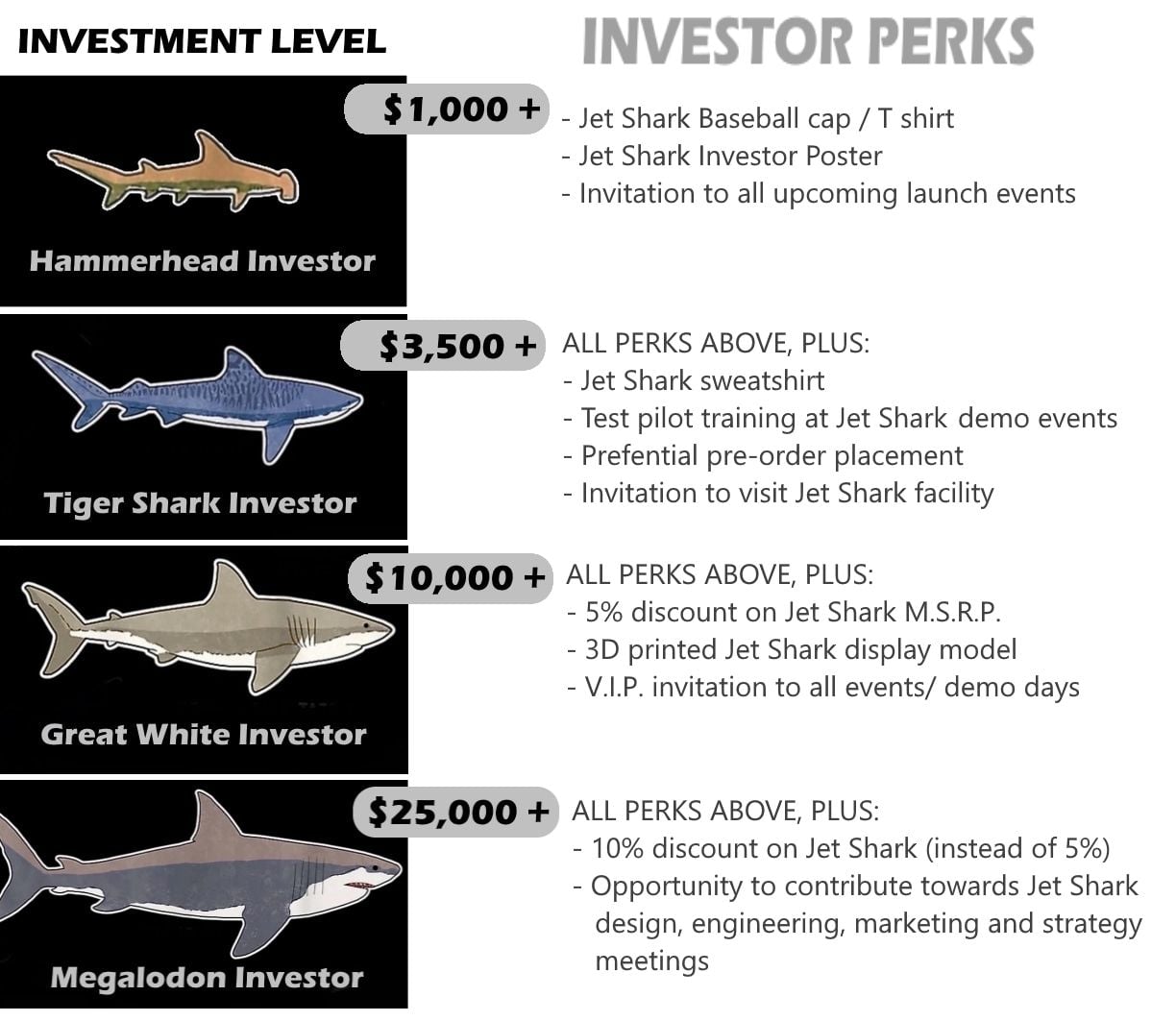

Now, we are offering investors the opportunity to support Jet Shark Inc; an all new, startup company with a huge growth potential! Your investment will help to bring this exciting new vessel to the mass market, and allow you to share in the prosperity along the way. So, what type of Investor Shark are you?

Although the Seabreacher (predecessor to the Jet Shark) have achieved huge commercial success, they do have several limitations:

The all new Jet Shark is specifically designed tor both the recreational and commercial tourist market. It is larger, has a greater capacity, is comfortable, reliable and more profitable for dealers and commercial operators!

Recreational market:

Commercial market:

We are THE dominating force in the high-performance, submersible watercraft market. Our previous vessels have had an impeccable safety record and are US Coast Guard and European CE compliant; just like any regular boat. No special license or registration is required to own or operate these unique boats!

Designing, testing, and refining numerous vessels over the last 25 years has given us the exclusive knowledge, technology, and expertise in this highly specialized market.

Jet Shark Inc. is anticipating huge growth in 2024 and this is the perfect time for savvy investors to jump in on this new expanding market!

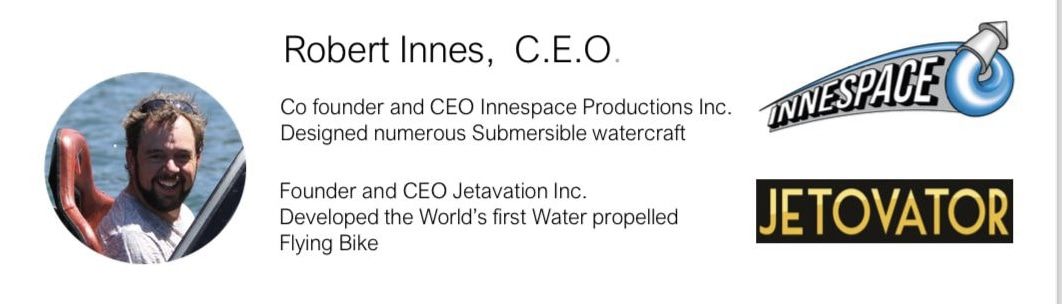

Jet Shark Inc. Founder and CEO, Rob Innes has had a successful career bringing unique boats and water sports toys to market. In 2008, he was the co-founder of Innespace Productions Inc.; the builder of the hugely popular SEABREACHER submersible watercraft. He also founded Jetavation Inc. in 2015, designing and building the JETOVATOR; the world’s first water-propelled, flying bike.

Rob has designed and built several vessels for the Film and TV industry and worked with movie director James Cameron on developing bespoke diving / flying watercraft for the AVATAR movies. He has also worked on several military projects for USSOCOM and the Navy Seals, including designing and building a submersible Jet ski prototype.

The crew at Innespace Productions Inc. have been custom building submersible watercraft for over fifteen years. They will be a key asset in the production and delivery of the first Jet Shark vessels.

Suppose the Company converts the Crowd SAFE as a result of equity financing. In that case, you must open a custodial account with the custodian and sign subscription documentation to receive the equity securities. The Company will notify you of the conversion trigger, and you must complete the necessary documentation within 30 days of such notice. If you do not complete the required documentation within that time frame, you will only be able to receive an amount of cash equal to (or less in some circumstances) your investment amount. Unclaimed cash will be subject to relevant escheatment laws. For more information, see the Crowd SAFE for this offering.

Suppose the conversion of the Crowd SAFE is triggered as a result of a Liquidity Event (e.g. M&A or an IPO). In that case, you will be required to select between receiving a cash payment (equal to your investment amount or a lesser amount) or equity. You are required to make your selection (and complete any relevant documentation) within 30 days of receiving notice from the Company of the conversion trigger, otherwise, you will receive the cash payment option, which will be subject to relevant escheatment laws. The equity consideration varies depending on whether the Liquidity Event occurs before or after an equity financing. For more information, see the Crowd SAFE for this offering.

We are using Republic's Crowd SAFE security. Learn how this translates into a return on investment here.

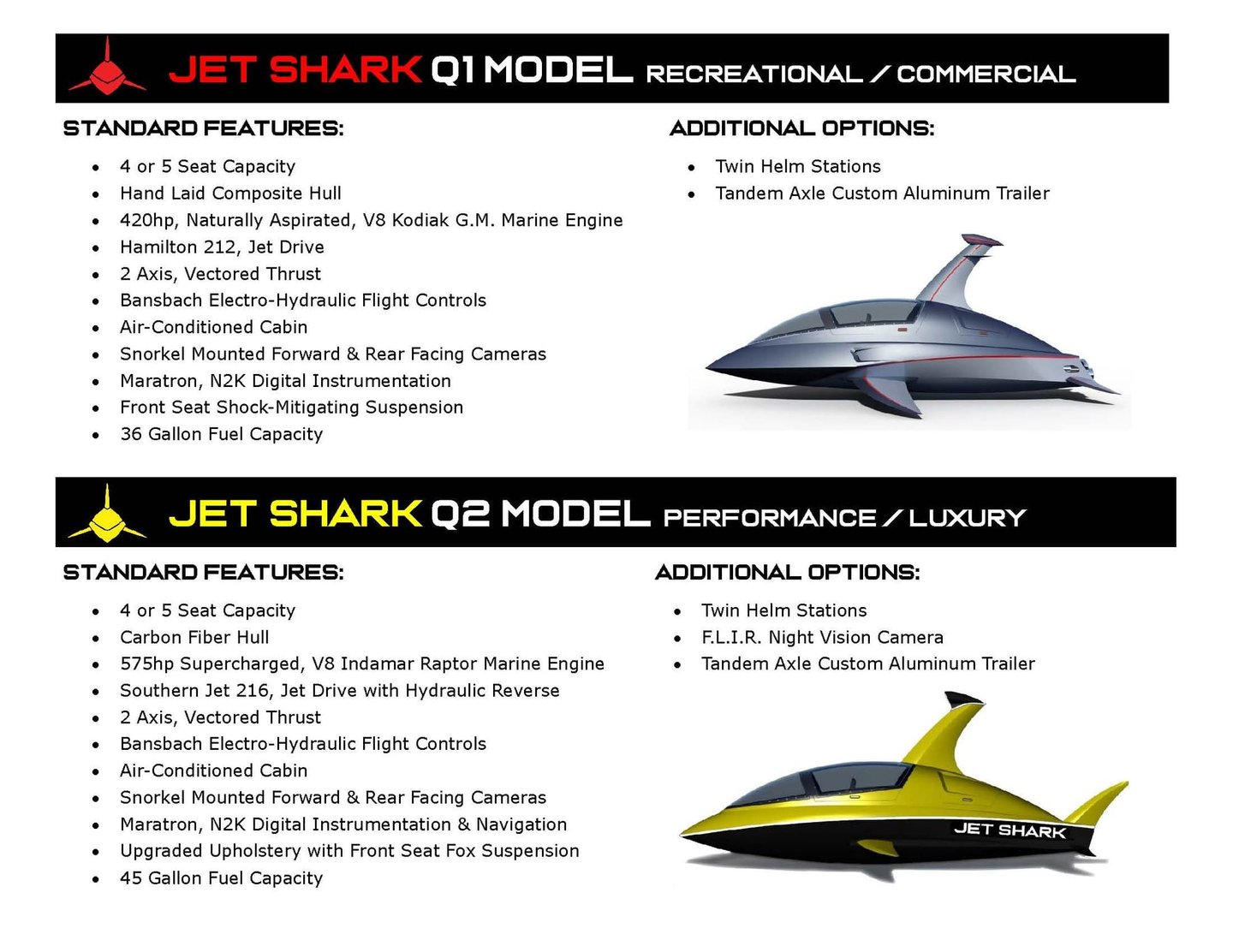

Initially there will be two models of Jet Sharks available; The Q1 model (intended for recreational and commercial use) and the Q2 model (Geared towards Performance and Luxury)

Expected retail price for the standard Q1 model is US$250,000. The Super-charged, carbon fiber, Q2 model is expected to cost approximately US$300,000. Wholesale discounts of 20% - 30% will be offered to qualified dealers/ distributors.

Beta model Jet Sharks will be delivered to select customers and existing commercial operations at the end of this year for long term evaluation and testing. Production versions are expected to be delivered at the beginning of 2025.

- Refine the vessels engineering and performance

- Expand our molding and tooling production in order to ready the Jet Shark for mass production

- Global certification so the Jet Shark can be registered and operated like any conventional boat

- Extensive marketing campaign to build brand awareness

- Product demonstration and Instructor training events at numerous key market locations

- Expand Distribution and Dealership Network, Training technicians in operation and servicing

- Networking with large Tourist Resorts to establish commercial Jet Shark passenger ride operations

- Moving Jet Shark operation to a larger manufacturing facility

Jet Shark Inc. is currently valued at US$10M. However we are offering a discounted valuation of $8M to early Investors until the first $250k is raised in this crowd funding round. We highly encourage Investors to get in early to take advantage of this discounted share value!

A significant outbreak of contagious diseases, such as COVID-19, in the human population could result in a widespread health crisis. Additionally, geopolitical events, such as wars or conflicts, could result in global disruptions to supplies, political uncertainty and displacement. Each of these crises could adversely affect the economies and financial markets of many countries, including the United States where we principally operate, resulting in an economic downturn that could reduce the demand for our products and services and impair our business prospects, including as a result of being unable to raise additional capital on acceptable terms, if at all.

The Issuer is still in an early phase and we are just beginning to implement our business plan. There can be no assurance that we will ever operate profitably. The likelihood of our success should be considered in light of the problems, expenses, difficulties, complications and delays usually encountered by early stage companies. The Issuer may not be successful in attaining the objectives necessary for it to overcome these risks and uncertainties.

In order to achieve the Issuer’s near and long-term goals, the Issuer may need to procure funds in addition to the amount raised in the Offering. There is no guarantee the Issuer will be able to raise such funds on acceptable terms or at all. If we are not able to raise sufficient capital in the future, we may not be able to execute our business plan, our continued operations will be in jeopardy and we may be forced to cease operations and sell or otherwise transfer all or substantially all of our remaining assets, which could cause an Investor to lose all or a portion of their investment.

We may have difficulty raising needed capital in the future as a result of, among other factors, our lack of revenues from sales, as well as the inherent business risks associated with the Issuer and present and future market conditions. Additionally, our future sources of revenue may not be sufficient to meet our future capital requirements. As such, we may require additional funds to execute our business strategy and conduct our operations. If adequate funds are unavailable, we may be required to delay, reduce the scope of or eliminate one or more of our research, development or commercialization programs, product launches or marketing efforts, any of which may materially harm our business, financial condition and results of operations.

The Issuer’s product is still in the development stage. There is no guarantee that it will ever receive required governmental and other approvals required to sell its products commercially or reach the commercial sales stage. Although the Issuer’s Founder has launched and commercialized other semi-submersible vessels, commercial sales for the Issuer’s products may not occur or such approvals or sales may be significantly delayed. If the Issuer is unable to commercialize its products or such commercialization is delayed, it will have a material impact on our business, financial condition and results of operations.

As an early-stage company, we may implement new lines of business at any time. There are substantial risks and uncertainties associated with these efforts, particularly in instances where the markets are not fully developed. In developing and marketing new lines of business and/or new products and services, we may invest significant time and resources. Initial timetables for the introduction and development of new lines of business and/or new products or services may not be achieved, and price and profitability targets may not prove feasible. We may not be successful in introducing new products and services in response to industry trends or developments in technology, or those new products may not achieve market acceptance. As a result, we could lose business, be forced to price products and services on less advantageous terms to retain or attract clients or be subject to cost increases. As a result, our business, financial condition or results of operations may be adversely affected.

We depend on suppliers and contractors to meet our contractual obligations to our customers and conduct our operations. Our ability to meet our obligations to our customers may be adversely affected if suppliers or contractors do not provide the agreed-upon supplies or perform the agreed-upon services in compliance with customer requirements and in a timely and cost-effective manner. Likewise, the quality of our products may be adversely impacted if companies to whom we delegate manufacture of major components or subsystems for our products, or from whom we acquire such items, do not provide components which meet required specifications and perform to our, and our customers’, expectations. Our suppliers may also be unable to quickly recover from natural disasters and other events beyond their control and may be subject to additional risks such as financial problems that limit their ability to conduct their operations. The risk of these adverse effects may be greater in circumstances where we rely on only one or two contractors or suppliers for a particular component. Our products may utilize custom components available from only one source. Continued availability of those components at acceptable prices, or at all, may be affected for any number of reasons, including if those suppliers decide to concentrate on the production of common components instead of components customized to meet our requirements. The supply of components for a new or existing product could be delayed or constrained, or a key manufacturing vendor could delay shipments of completed products to us adversely affecting our business and results of operations.

The Issuer relies on certain intellectual property rights to operate its business. The Issuer’s intellectual property rights may not be sufficiently broad or otherwise may not provide us a significant competitive advantage. In addition, the steps that we have taken to maintain and protect our intellectual property may not prevent it from being challenged, invalidated, circumvented or designed-around, particularly in countries where intellectual property rights are not highly developed or protected. In some circumstances, enforcement may not be available to us because an infringer has a dominant intellectual property position or for other business reasons, or countries may require compulsory licensing of our intellectual property. Our failure to obtain or maintain intellectual property rights that convey competitive advantage, adequately protect our intellectual property or detect or prevent circumvention or unauthorized use of such property, could adversely impact our competitive position and results of operations. We also rely on nondisclosure and noncompetition agreements with employees, consultants and other parties to protect, in part, trade secrets and other proprietary rights. There can be no assurance that these agreements will adequately protect our trade secrets and other proprietary rights and will not be breached, that we will have adequate remedies for any breach, that others will not independently develop substantially equivalent proprietary information or that third parties will not otherwise gain access to our trade secrets or other proprietary rights. As we expand our business, protecting our intellectual property will become increasingly important. The protective steps we have taken may be inadequate to deter our competitors from using our proprietary information. In order to protect or enforce our intellectual property rights, we may be required to initiate litigation against third parties, such as infringement lawsuits. Also, these third parties may assert claims against us with or without provocation. These lawsuits could be expensive, take significant time and could divert management’s attention from other business concerns. We cannot assure you that we will prevail in any of these potential suits or that the damages or other remedies awarded, if any, would be commercially valuable.

We are dependent on our executive officers and key personnel. These persons may not devote their full time and attention to the matters of the Issuer. The loss of all or any of our executive officers and key personnel could harm the Issuer’s business, financial condition, cash flow and results of operations.

You should not rely on the fact that our Form C is accessible through the U.S. Securities and Exchange Commission’s EDGAR filing system as an approval, endorsement or guarantee of compliance as it relates to this Offering. The U.S. Securities and Exchange Commission has not reviewed this Form C, nor any document or literature related to this Offering.

We are dependent on certain key personnel in order to conduct our operations and execute our business plan, however, the Issuer has not purchased any insurance policies with respect to those individuals in the event of their death or disability. Therefore, if any of these personnel die or become disabled, the Issuer will not receive any compensation to assist with such person’s absence. The loss of such person could negatively affect the Issuer and our operations. We have no way to guarantee key personnel will stay with the Issuer, as many states do not enforce non-competition agreements, and therefore acquiring key man insurance will not ameliorate all of the risk of relying on key personnel.

Recruiting and retaining highly qualified personnel is critical to our success. These demands may require us to hire additional personnel and will require our existing management and other personnel to develop additional expertise. We face intense competition for personnel, making recruitment time-consuming and expensive. The failure to attract and retain personnel or to develop such expertise could delay or halt the development and commercialization of our product candidates. If we experience difficulties in hiring and retaining personnel in key positions, we could suffer from delays in product development, loss of customers and sales and diversion of management resources, which could adversely affect operating results. Our consultants and advisors may be employed by third parties and may have commitments under consulting or advisory contracts with third parties that may limit their availability to us, which could further delay or disrupt our product development and growth plans.

To succeed, we must continually improve, refresh and expand our product and service offerings to include newer features, functionality or solutions, and keep pace with changes in the industry. Shortened product life cycles due to changing customer demands and competitive pressures may impact the pace at which we must introduce new products or implement new functions or solutions. In addition, bringing new products or solutions to the market entails a costly and lengthy process, and requires us to accurately anticipate changing customer needs and trends. We must continue to respond to changing market demands and trends or our business operations may be adversely affected.

We may face competition with respect to any products that we may seek to develop or commercialize in the future. Our competitors may include major companies worldwide. Many of those competitors could have significantly greater financial, technical and human resources than we have and superior expertise in research and development and marketing approved products and thus may be better equipped than us to develop and commercialize products. These competitors also may compete with us in recruiting and retaining qualified personnel and acquiring technologies. Smaller or early stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large and established companies. Accordingly, our competitors may commercialize products more rapidly or effectively than we are able to, which would adversely affect our competitive position, the likelihood that our products will achieve initial market acceptance, and our ability to generate meaningful additional revenues from our products.

As part of our growth strategy, we will have to make significant investments to build our e-commerce business. We may require additional capital in the future to sustain or grow our e-commerce business. Business risks related to our e-commerce business include our inability to keep pace with rapid technological change, failure in our security procedures or operational controls, failure or inadequacy in our systems or labor resource levels to effectively process customer orders in a timely manner, government regulation and legal uncertainties with respect to e-commerce, and collection of sales or other taxes by one or more states or foreign jurisdictions. If any of these risks materialize, they could have an adverse effect on our business. In addition, we may face competition in the future, from new retailers who enter the market. Our failure to positively differentiate our product and services offerings or customer experience from these new internet retailers could have a material adverse effect on our business, financial condition and results of operations.

The Issuer’s product offering is unique and will be sold as a luxury item to most purchasers. As such, the Issuer’s product may not be accepted by consumers, may be impacted due to changes in consumer tastes or could be impacted by changes in the economy which may restrict luxury purchases. Consumer acceptance and the resulting success of new products will be one of the keys to the success of the Issuer’s business plan. There can be no assurance that the Issuer will succeed in the development of its products or any new products or that these products will achieve market acceptance or generate meaningful revenue for the Issuer.

Our reputation and the quality of our brand are critical to our business and success in existing markets, and will be critical to our success as we enter new markets. Any incident that erodes consumer loyalty for our brand could significantly reduce its value and damage our business. We may be adversely affected by any negative publicity, regardless of its accuracy. Also, there has been a marked increase in the use of social media platforms and similar devices, including blogs, social media websites and other forms of internet-based communications that provide individuals with access to a broad audience of consumers and other interested persons. The availability of information on social media platforms is virtually immediate as is its impact. Information posted may be adverse to our interests or may be inaccurate, each of which may harm our performance, prospects or business. The harm may be immediate and may disseminate rapidly and broadly, without affording us an opportunity for redress or correction.

The financial statements attached as Exhibit A to this Form C have been “reviewed” only and such financial statements have not been verified with outside evidence as to management’s amounts and disclosures. Additionally, tests on internal controls have not been conducted. Therefore, you will have no audited financial information regarding the Issuer’s capitalization or assets or liabilities on which to make your investment decision.

We may face advanced and persistent attacks on our information infrastructure where we manage and store various proprietary information and sensitive/confidential data relating to our operations. These attacks may include sophisticated malware (viruses, worms, and other malicious software programs) and phishing emails that attack our products or otherwise exploit any security vulnerabilities. These intrusions sometimes may be zero-day malware that are difficult to identify because they are not included in the signature set of commercially available antivirus scanning programs. Experienced computer programmers and hackers may be able to penetrate our network security and misappropriate or compromise our confidential information or that of our customers or other third-parties, create system disruptions, or cause shutdowns. Additionally, sophisticated software and applications that we produce or procure from third-parties may contain defects in design or manufacture, including “bugs” and other problems that could unexpectedly interfere with the operation of the information infrastructure. A disruption, infiltration or failure of our information infrastructure systems or any of our data centers as a result of software or hardware malfunctions, computer viruses, cyber-attacks, employee theft or misuse, power disruptions, natural disasters or accidents could cause breaches of data security, loss of critical data and performance delays, which in turn could adversely affect our business.

Our business requires the collection, transmission and retention of personally identifiable information, in various information technology systems that we maintain and in those maintained by third parties with whom we contract to provide services. The integrity and protection of that data is critical to us. The information, security and privacy requirements imposed by governmental regulation are increasingly demanding. Our systems may not be able to satisfy these changing requirements and customer and employee expectations, or may require significant additional investments or time in order to do so. A breach in the security of our information technology systems or those of our service providers could lead to an interruption in the operation of our systems, resulting in operational inefficiencies and a loss of profits. Additionally, a significant theft, loss or misappropriation of, or access to, customers’ or other proprietary data or other breach of our information technology systems could result in fines, legal claims or proceedings.

The regulation of individual data is changing rapidly, and in unpredictable ways. A change in regulation could adversely affect our business, including causing our business model to no longer be viable. Costs associated with information security – such as investment in technology, the costs of compliance with consumer protection laws and costs resulting from consumer fraud – could cause our business and results of operations to suffer materially. Additionally, the success of our online operations depends upon the secure transmission of confidential information over public networks, including the use of cashless payments. The intentional or negligent actions of employees, business associates or third parties may undermine our security measures. As a result, unauthorized parties may obtain access to our data systems and misappropriate confidential data. There can be no assurance that advances in computer capabilities, new discoveries in the field of cryptography or other developments will prevent the compromise of our customer transaction processing capabilities and personal data. If any such compromise of our security or the security of information residing with our business associates or third parties were to occur, it could have a material adverse effect on our reputation, operating results and financial condition. Any compromise of our data security may materially increase the costs we incur to protect against such breaches and could subject us to additional legal risk.

The Issuer may not have the internal control infrastructure that would meet the standards of a public company, including the requirements of the Sarbanes Oxley Act of 2002. As a privately-held (non-public) issuer, the Issuer is currently not subject to the Sarbanes Oxley Act of 2002, and its financial and disclosure controls and procedures reflect its status as a development stage, non-public company. There can be no guarantee that there are no significant deficiencies or material weaknesses in the quality of the Issuer’s financial and disclosure controls and procedures. If it were necessary to implement such financial and disclosure controls and procedures, the cost to the Issuer of such compliance could be substantial and could have a material adverse effect on the Issuer’s results of operations.

The Issuer is subject to legislation and regulation at the federal and local levels and, in some instances, at the state level. New laws and regulations may impose new and significant disclosure obligations and other operational, marketing and compliance-related obligations and requirements, which may lead to additional costs, risks of non- compliance, and diversion of our management's time and attention from strategic initiatives. Additionally, federal, state and local legislators or regulators may change current laws or regulations which could adversely impact our business. Further, court actions or regulatory proceedings could also change our rights and obligations under applicable federal, state and local laws, which cannot be predicted. Modifications to existing requirements or imposition of new requirements or limitations could have an adverse impact on our business.

We are also subject to a wide range of federal, state, and local laws and regulations. In particular, the Issuer’s products will be required to be certified by the United States Coast Guard and also to comply with the standards of the American Boat and Yachting Council. The violation of these or future requirements or laws and regulations could result in administrative, civil, or criminal sanctions against us, which may include fines, a cease and desist order against the subject operations or even revocation or suspension of our license to operate the subject business. As a result, we may incur capital and operating expenditures and other costs to comply with these requirements and laws and regulations.

No governmental agency has reviewed or passed upon this Offering or the Securities. Neither the Offering nor the Securities have been registered under federal or state securities laws. Investors will not receive any of the benefits available in registered offerings, which may include access to quarterly and annual financial statements that have been audited by an independent accounting firm. Investors must therefore assess the adequacy of disclosure and the fairness of the terms of this Offering based on the information provided in this Form C and the accompanying exhibits.

Unless the Issuer has agreed to a specific use of the proceeds from the Offering, the Issuer’s management will have considerable discretion over the use of proceeds from the Offering. You may not have the opportunity, as part of your investment decision, to assess whether the proceeds are being used appropriately.

The Offering is divided into separate tranches for early investors and standard investors. “Early Investors,” which include investors who invest during the first tranche of the Offering, which includes the initial purchases amounting up to and including a sum of $250,000.00, will receive a SAFE with preferential terms, namely a reduced pre-money valuation cap ($8,000,000 instead of $10,000,000). A SAFE with different terms will be issued to “Standard Investors,” or investors who invest during the second tranche of the Offering, which includes all purchases from

$250,000.01 to $1,235,000. Accordingly, a single investor may be issued two different SAFEs with different terms, depending on the timing of the investor’s investment commitment.

At the conclusion of the Offering, the Issuer shall pay the Intermediary the greater of (A) a fee of six percent (6%) of the dollar amount raised in the Offering or (B) a cash fee of twelve thousand dollars ($12,000.00). The compensation paid by the Issuer to the Intermediary may impact how the Issuer uses the net proceeds of the Offering.

The Issuer may prevent any Investor from committing more than a certain amount in this Offering based on the Issuer’s determination of the Investor’s sophistication and ability to assume the risk of the investment. This means that your desired investment amount may be limited or lowered based solely on the Issuer’s determination and not in line with relevant investment limits set forth by the Regulation CF rules. This also means that other Investors may receive larger allocations of the Offering based solely on the Issuer’s determination.

The Issuer may extend the Offering Deadline beyond what is currently stated herein. This means that your investment may continue to be held in escrow while the Issuer attempts to raise the Target Offering Amount even after the Offering Deadline stated herein is reached. While you have the right to cancel your investment in the event the Issuer extends the Offering Deadline, if you choose to reconfirm your investment, your investment will not be accruing interest during this time and will simply be held until such time as the new Offering Deadline is reached without the Issuer receiving the Target Offering Amount, at which time it will be returned to you without interest or deduction, or the Issuer receives the Target Offering Amount, at which time it will be released to the Issuer to be used as set forth herein. Upon or shortly after the release of such funds to the Issuer, the Securities will be issued and distributed to you.

If the Target Offering Amount is met after 21 calendar days, but before the Offering Deadline, the Issuer can end the Offering by providing notice to Investors at least 5 business days prior to the end of the Offering. This means your failure to participate in the Offering in a timely manner, may prevent you from being able to invest in this Offering – it also means the Issuer may limit the amount of capital it can raise during the Offering by ending the Offering early.

If the Issuer meets certain terms and conditions, an intermediate close (also known as a rolling close) of the Offering can occur, which will allow the Issuer to draw down on seventy percent (70%) of Investor proceeds committed and captured in the Offering during the relevant period. The Issuer may choose to continue the Offering thereafter. Investors should be mindful that this means they can make multiple investment commitments in the Offering, which may be subject to different cancellation rights. For example, if an intermediate close occurs and later a material change occurs as the Offering continues, Investors whose investment commitments were previously closed upon will not have the right to re-confirm their investment as it will be deemed to have been completed prior to the material change.

In connection with investing in this Offering to purchase a SAFE (Simple Agreement for Future Equity) investors will designate Republic Investment Services LLC (f/k/a NextSeed Services, LLC) (the “Nominee”) to act on their behalf as agent and proxy in all respects. The Nominee will be entitled, among other things, to exercise any voting rights (if any) conferred upon the holder of the Securities or any securities acquired upon their conversion, to execute on behalf of an investor all transaction documents related to the transaction or other corporate event causing the conversion of the Securities, and as part of the conversion process the Nominee has the authority to open an account in the name of a qualified custodian, of the Nominee’s sole discretion, to take custody of any securities acquired upon conversion of the Securities. Thus, by participating in the Offering, investors will grant broad discretion to a third party (the Nominee and its agents) to take various actions on their behalf, and investors will essentially not be able to vote upon matters related to the governance and affairs of the Issuer nor take or effect actions that might otherwise be available to holders of the Securities and any securities acquired upon their conversion. Investors should not participate in the Offering unless he, she or it is willing to waive or assign certain rights that might otherwise be afforded to a holder of the Securities to the Nominee and grant broad authority to the Nominee to take certain actions on behalf of the investor, including changing title to the Security.

You should be aware of the long-term nature of this investment. There is not now and likely will not ever be a public market for the Securities. Because the Securities have not been registered under the Securities Act or under the securities laws of any state or foreign jurisdiction, the Securities have transfer restrictions and cannot be resold in the United States except pursuant to Rule 501 of Regulation CF. It is not currently contemplated that registration under the Securities Act or other securities laws will be effected. Limitations on the transfer of the Securities may also adversely affect the price that you might be able to obtain for the Securities in a private sale. Investors should be aware of the long-term nature of their investment in the Issuer. Each Investor in this Offering will be required to represent that they are purchasing the Securities for their own account, for investment purposes and not with a view to resale or distribution thereof. If a transfer, resale, assignment or distribution of the Security should occur prior to the conversion of the Security or after, if the Security is still held by the original purchaser directly, the transferee, purchaser, assignee or distribute, as relevant, will be required to sign a new Nominee Rider (as defined in the Security) and provide personally identifiable information to the Nominee sufficient to establish a custodial account at a later date and time. Under the Terms of the Securities, the Nominee has the right to place shares received from the conversion of the Security into a custodial relationship with a qualified third party and have said Nominee be listed as the holder of record. In this case, Investors will only have a beneficial interest in the equity securities derived from the Securities, not legal ownership, which may make their resale more difficult as it will require coordination with the custodian and Republic Investment Services.

Prior to the Offering, one individual, Robert Innes, the Issuer’s CEO and Founder, beneficially owns all of the Issuer’s outstanding equity. Subject to any fiduciary duties owed to other stockholders or investors under Delaware law, Mr. Innes will be able to exercise significant influence over matters requiring stockholder approval, including the election of directors and approval of significant Company transactions, and will have significant control over the Issuer’s management and policies. As such, Mr. Innes’ interests may be different than yours. For example, he may support

proposals and actions with which you may disagree. This concentration of ownership could delay or prevent a change in control of the Issuer or otherwise discourage a potential acquirer from attempting to obtain control of the Issuer, which in turn could reduce the price potential investors are willing to pay for the Issuer. In addition, Mr. Innes could use his voting influence to maintain the Issuer’s existing management, delay or prevent changes in control of the Issuer, issue additional securities which may dilute you, repurchase securities of the Issuer, enter into transactions with related parties or support or reject other management and board proposals that are subject to stockholder approval.

Investors will not have an ownership claim to the Issuer or to any of its assets or revenues for an indefinite amount of time and depending on when and how the Securities are converted, the Investors may never become equity holders of the Issuer. Investors will not become equity holders of the Issuer unless the Issuer receives a future round of financing great enough to trigger a conversion and the Issuer elects to convert the Securities. The Issuer is under no obligation to convert the Securities. In certain instances, such as a sale of the Issuer or substantially all of its assets, an initial public offering or a dissolution or bankruptcy, the Investors may only have a right to receive cash, to the extent available, rather than equity in the Issuer. Further, the Investor may never become an equity holder, merely a beneficial owner of an equity interest, should the Issuer or the Nominee decide to move the SAFE or the securities issuable thereto into a custodial relationship.

Investors will not have the right to vote upon matters of the Issuer even if and when their Securities are converted (the occurrence of which cannot be guaranteed). Under the terms of the Securities, a third-party designated by the Issuer will exercise voting control over the Securities. Upon conversion, the Securities will continue to be voted in line with the designee identified or pursuant to a voting agreement related to the equity securities the Security is converted into. For example, if the Securities are converted in connection with an offering of Series B Preferred Stock, Investors would directly or beneficially receive securities in the form of shares of Series B-CF Preferred Stock and such shares would be required to be subject to the terms of the Securities that allows a designee to vote their shares of Series B- CF Preferred Stock consistent with the terms of the Security. Thus, Investors will essentially never be able to vote upon any matters of the Issuer unless otherwise provided for by the Issuer.

Investors will not have the right to inspect the books and records of the Issuer or to receive financial or other information from the Issuer, other than as required by law. Other security holders of the Issuer may have such rights. Regulation CF requires only the provision of an annual report on Form C and no additional information. Additionally, there are numerous methods by which the Issuer can terminate annual report obligations, resulting in no information rights, contractual, statutory or otherwise, owed to Investors. This lack of information could put Investors at a disadvantage in general and with respect to other security holders, including certain security holders who have rights to periodic financial statements and updates from the Issuer such as quarterly unaudited financials, annual projections and budgets, and monthly progress reports, among other things.

Unlike convertible notes and some other securities, the Securities do not have any “default” provisions upon which Investors will be able to demand repayment of their investment. The Issuer has ultimate discretion as to whether or not to convert the Securities upon a future equity financing and Investors have no right to demand such conversion. Only in limited circumstances, such as a liquidity event, may Investors demand payment and even then, such payments will be limited to the amount of cash available to the Issuer.

The Issuer may never conduct a future equity financing or elect to convert the Securities if such future equity financing does occur. In addition, the Issuer may never undergo a liquidity event such as a sale of the Issuer or an initial public offering. If neither the conversion of the Securities nor a liquidity event occurs, Investors could be left holding the Securities in perpetuity. The Securities have numerous transfer restrictions and will likely be highly illiquid, with no secondary market on which to sell them. If a transfer, resale, assignment or distribution of the Security should occur

prior to the conversion of the Security or after, if the Security is still held by the original purchaser directly, the transferee, purchaser, assignee or distribute, as relevant, will be required to sign a new Nominee Rider (as defined in the Security) and provide personally identifiable information to the Nominee sufficient to establish a custodial account at a later date and time. Under the terms of the Securities, the Nominee has the right to place shares received from the conversion of the Security into a custodial relationship with a qualified third party and have said Nominee be listed as the holder of record. In this case, Investors will only have a beneficial interest in the equity securities derived from the Securities, not legal ownership, which may make their resale more difficult as it will require coordination with the custodian and Republic Investment Services. The Securities are not equity interests, have no ownership rights, have no rights to the Issuer’s assets or profits and have no voting rights or ability to direct the Issuer or its actions.

The Issuer’s equity securities will be subject to dilution. The Issuer intends to issue additional equity to employees and third-party financing sources in amounts that are uncertain at this time, and as a consequence holders of equity securities resulting from the conversion of the Securities will be subject to dilution in an unpredictable amount. Such dilution may reduce the Investor’s control and economic interests in the Issuer.

The amount of additional financing needed by the Issuer will depend upon several contingencies not foreseen at the time of this Offering. Generally, additional financing (whether in the form of loans or the issuance of other securities) will be intended to provide the Issuer with enough capital to reach the next major corporate milestone. If the funds received in any additional financing are not sufficient to meet the Issuer’s needs, the Issuer may have to raise additional capital at a price unfavorable to their existing investors, including the holders of the Securities. The availability of capital is at least partially a function of capital market conditions that are beyond the control of the Issuer. There can be no assurance that the Issuer will be able to accurately predict the future capital requirements necessary for success or that additional funds will be available from any source. Failure to obtain financing on favorable terms could dilute or otherwise severely impair the value of the Securities.

In the event the Issuer decides to exercise the conversion right, the Issuer will convert the Securities into equity securities that are materially different from the equity securities being issued to new investors at the time of conversion in many ways, including, but not limited to, liquidation preferences, dividend rights, or anti-dilution protection. Additionally, any equity securities issued at the First Equity Financing Price (as defined in the SAFE agreement) shall have only such preferences, rights, and protections in proportion to the First Equity Financing Price and not in proportion to the price per share paid by new investors receiving the equity securities. Upon conversion of the Securities, the Issuer may not provide the holders of such Securities with the same rights, preferences, protections, and other benefits or privileges provided to other investors of the Issuer.

The forgoing paragraph is only a summary of a portion of the conversion feature of the Securities; it is not intended to be complete, and is qualified in its entirety by reference to the full text of the SAFE agreement, which is attached as Exhibit B.

The offering price was not established in a competitive market. We have arbitrarily set the price of the Securities with reference to the general status of the securities market and other relevant factors. The offering price for the Securities should not be considered an indication of the actual value of the Securities and is not based on our asset value, net worth, revenues or other established criteria of value. We cannot guarantee that the Securities can be resold at the offering price or at any other price.

In the event of the dissolution or bankruptcy of the Issuer, the holders of the Securities that have not been converted will be entitled to distributions as described in the Securities. This means that such holders will only receive distributions once all of the creditors and more senior security holders, including any holders of preferred stock, have been paid in full. No holders of any of the Securities can be guaranteed any proceeds in the event of the dissolution or bankruptcy of the Issuer.

Upon the occurrence of certain events, as provided in the Securities, holders of the Securities may be entitled to a return of the principal amount invested. Despite the contractual provisions in the Securities, this right cannot be guaranteed if the Issuer does not have sufficient liquid assets on hand. Therefore, potential Investors should not assume a guaranteed return of their investment amount.

There is no assurance that an Investor will realize a return on their investment or that they will not lose their entire investment. For this reason, each Investor should read this Form C and all exhibits carefully and should consult with their attorney and business advisor prior to making any investment decision.

Invest in the app