How Percent is Disrupting a $7 Trillion Market

Workweek

·

Jul 21, 2022

Let's all give a special welcome to one of my sisters who (finally) signed up for The Crossover after 6 weeks! I love you...

Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Percent is a global leader in financial infrastructure solutions. Founded in 2018, the company leverages proprietary technologies, integrations, and data to bring first-of-its-kind transparency and efficiency to lenders and credit transactions. Percent's innovative ecosystem enables lenders of any size to raise the most flexible debt capital at a low cost through dynamic market pricing and standardized terms. To date, its platforms have powered more than $700 million in transaction volume in a multi-trillion-dollar lending market.

This is a special purpose vehicle (SPV) formed to invest in Percent's $25M+ Series B.

Investment Highlights (provided by the company as of August 2022):

—

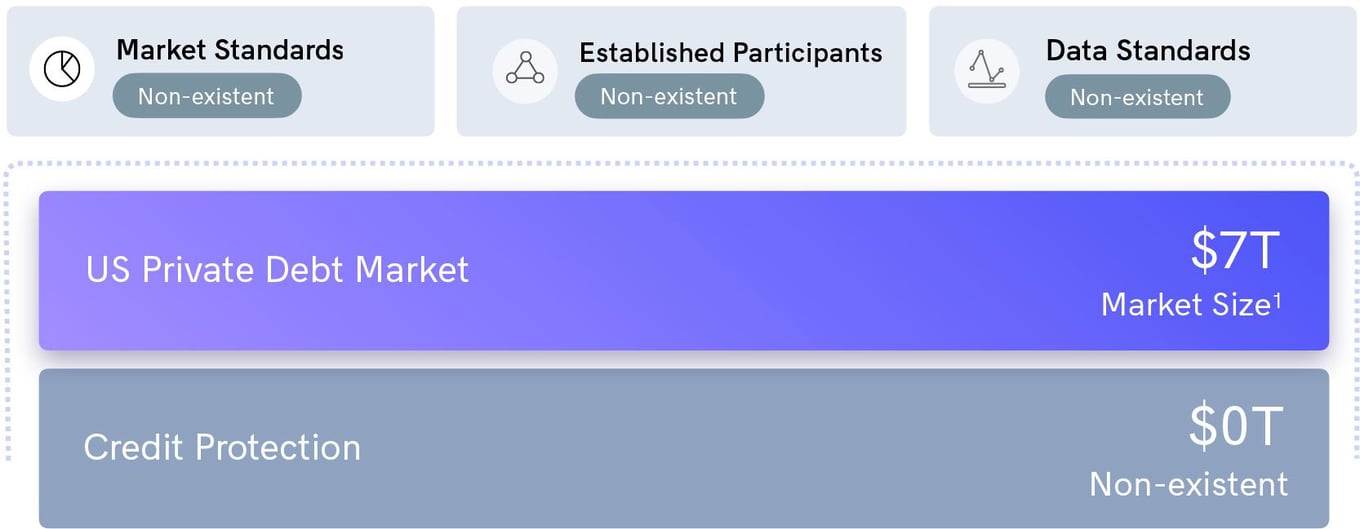

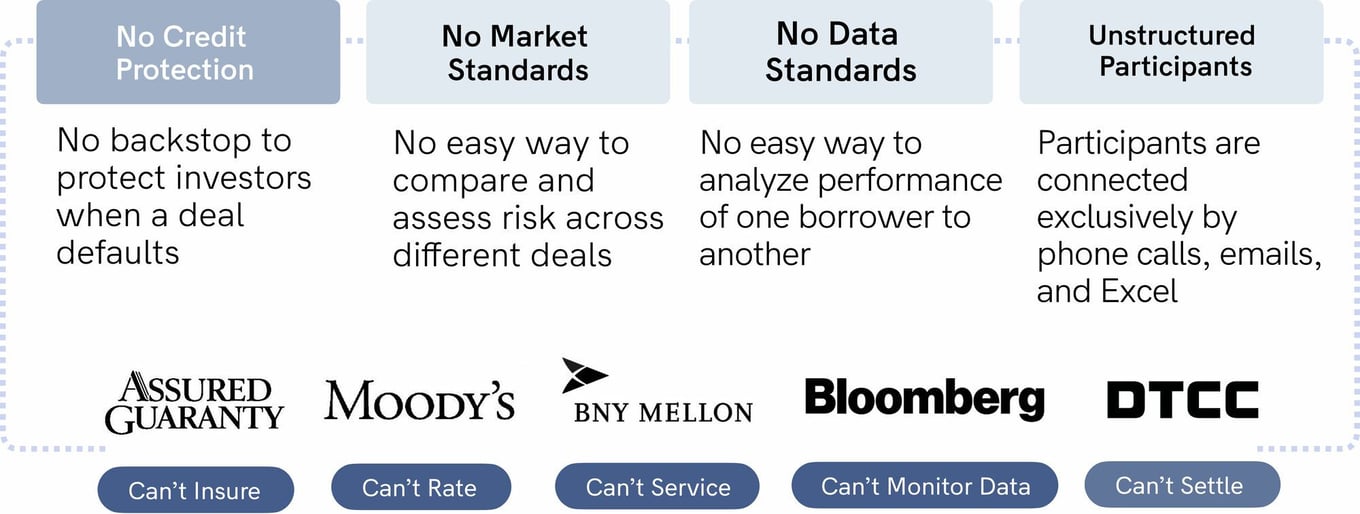

Established parties in public debt markets have been unable to penetrate private debt markets without this core infrastructure in place, forgoing $35B+ in annual revenue

—

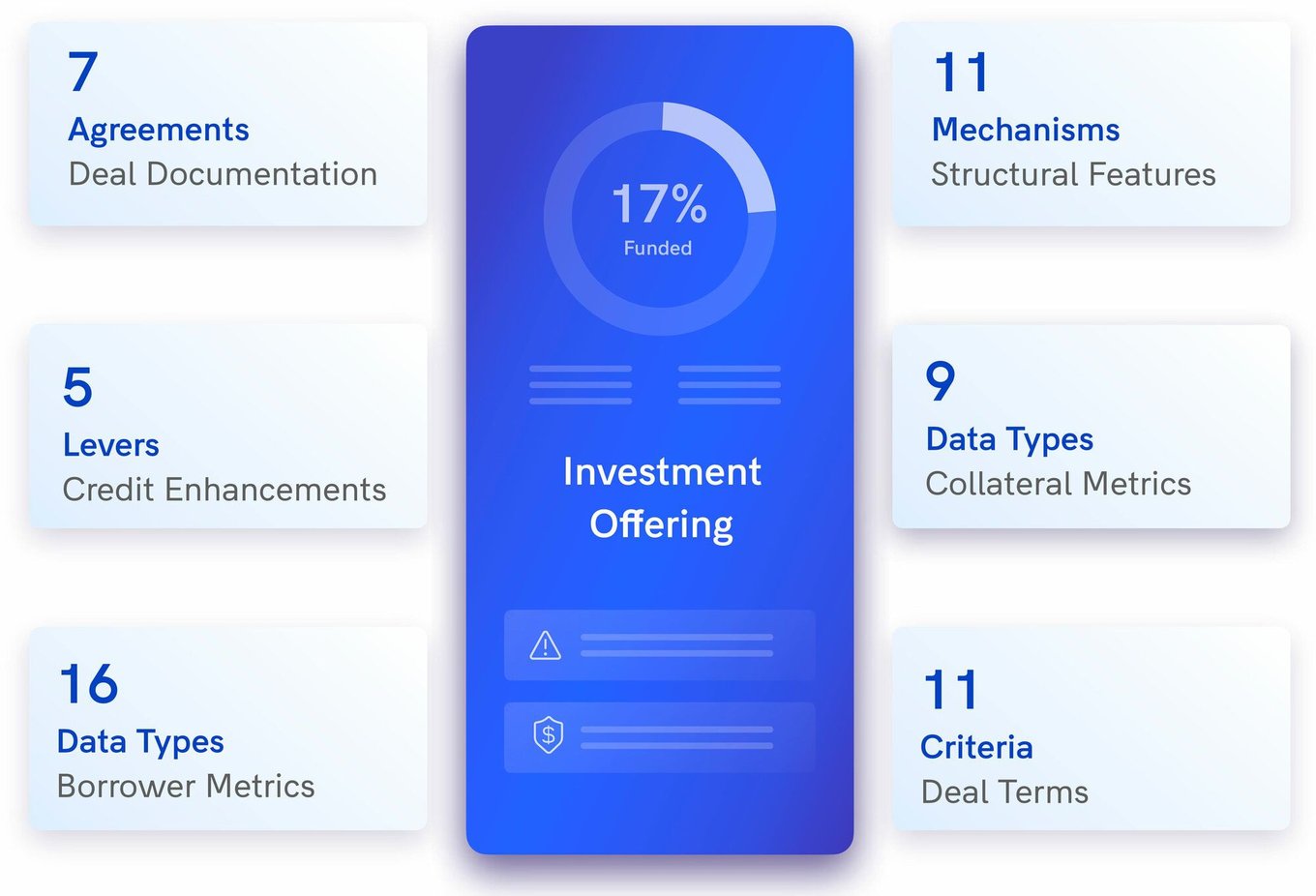

Percent's platform increases the speed and velocity of transactions at a fraction of the cost through proprietary data, tailor-made workflows, and purpose-built automation.

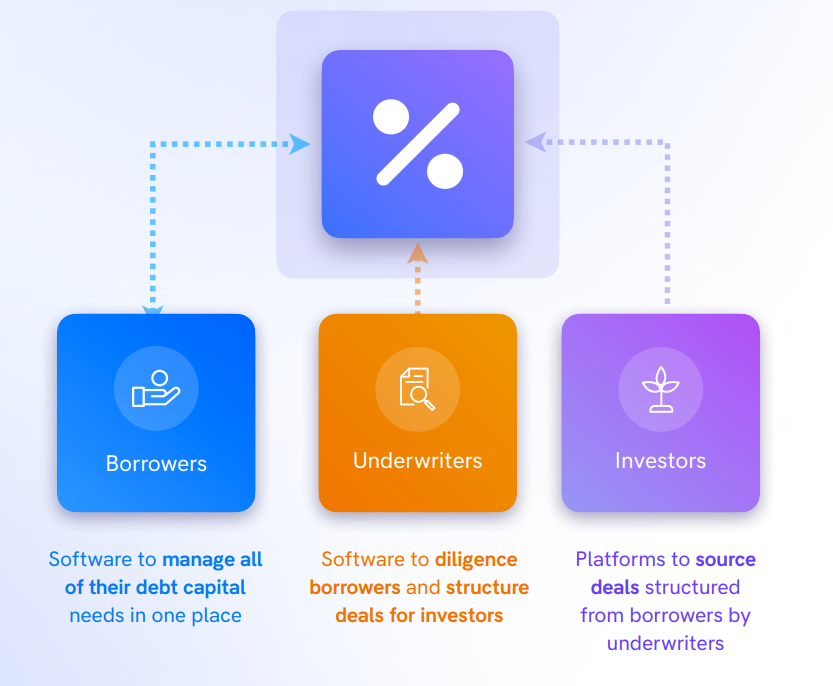

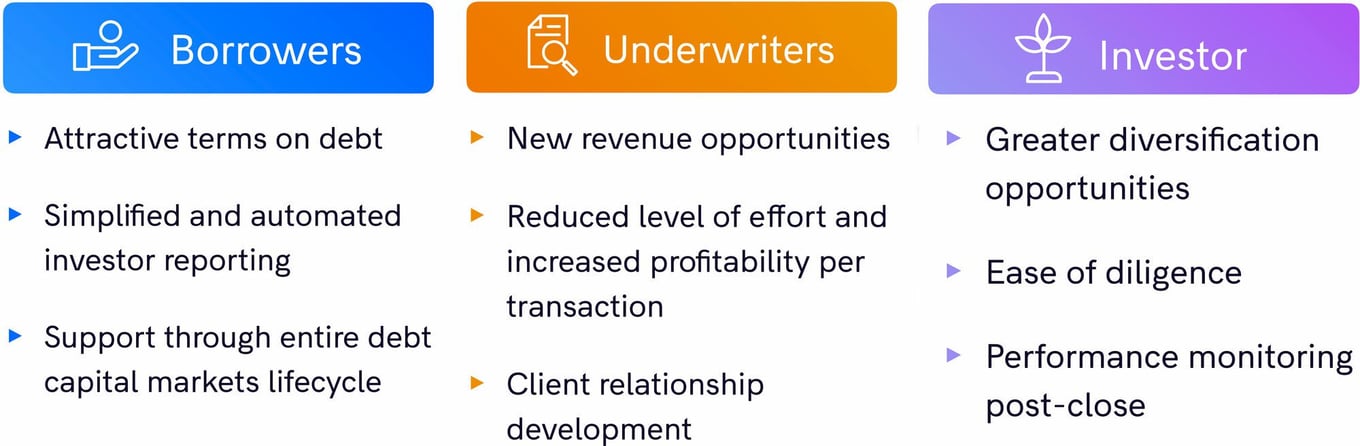

They have developed a comprehensive end-to-end software suite for every market participant:

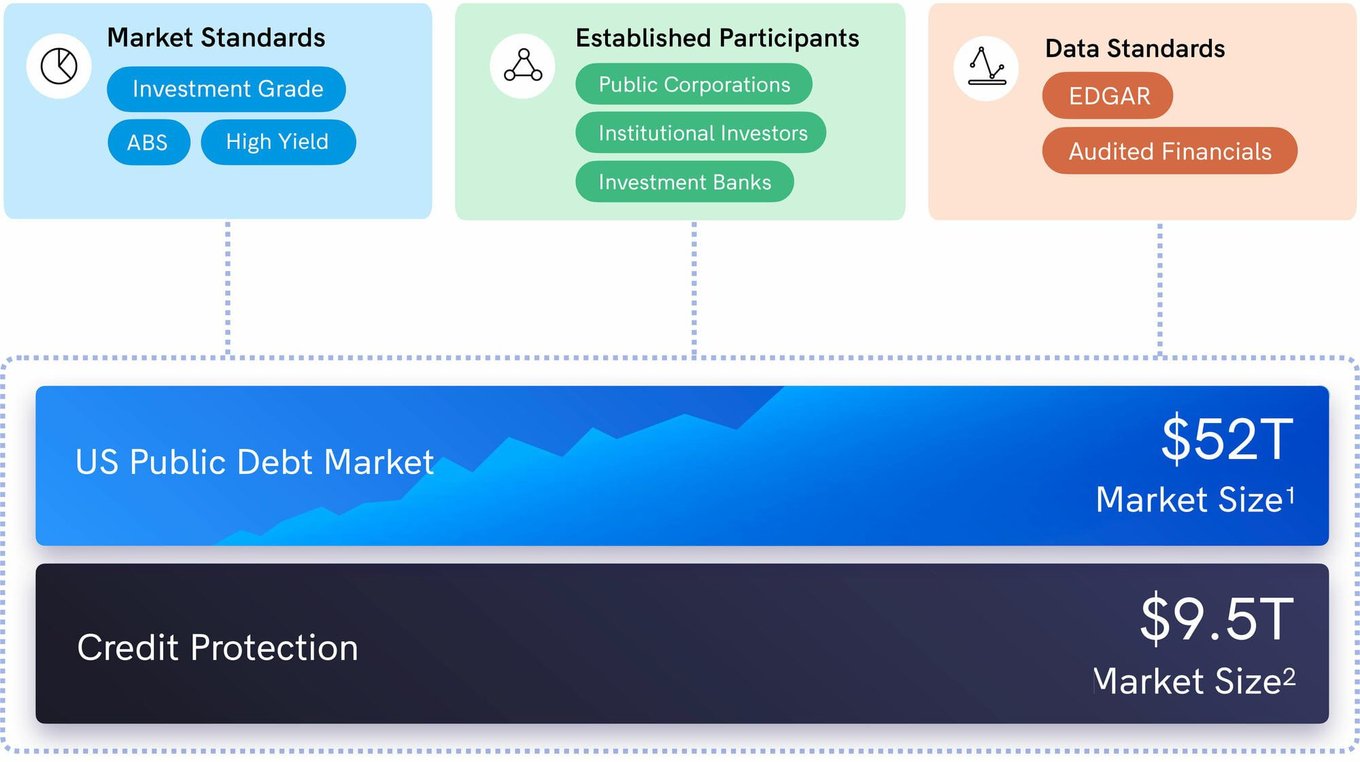

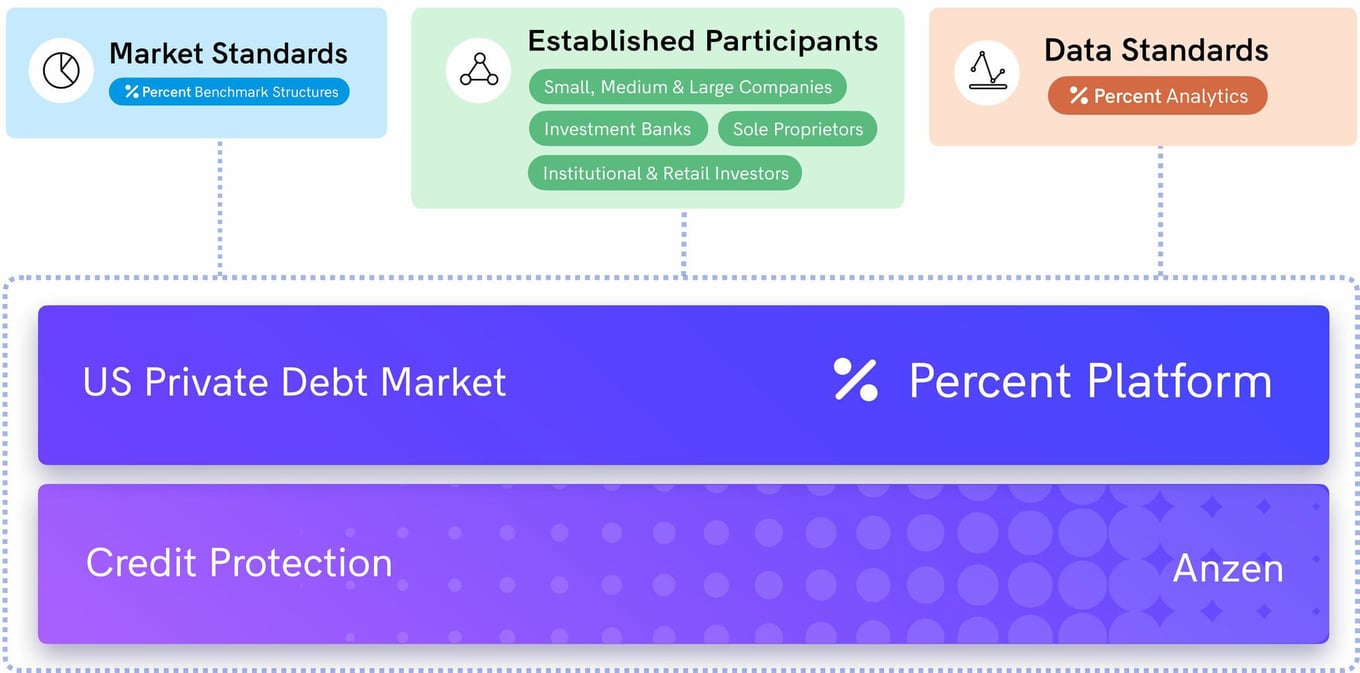

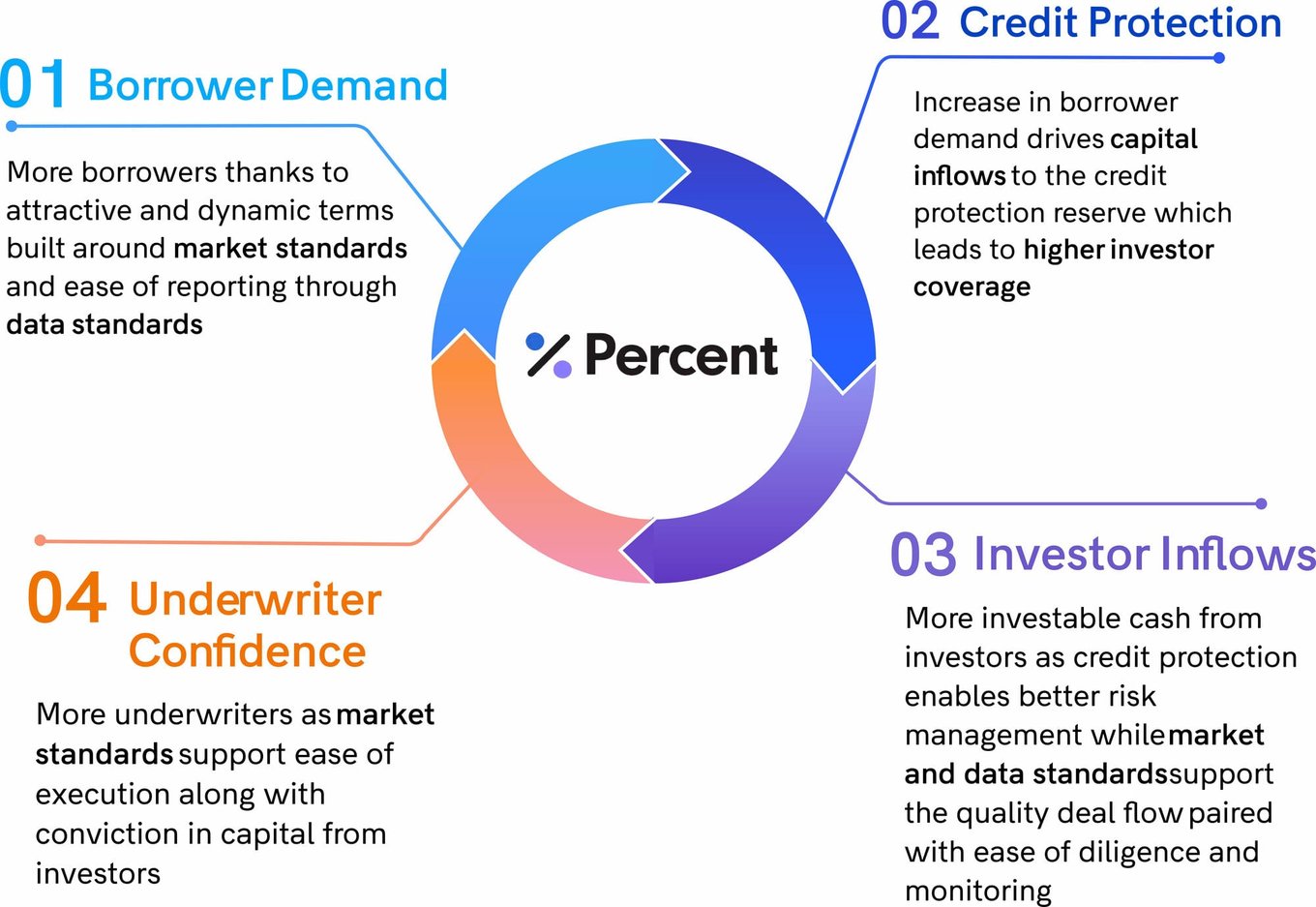

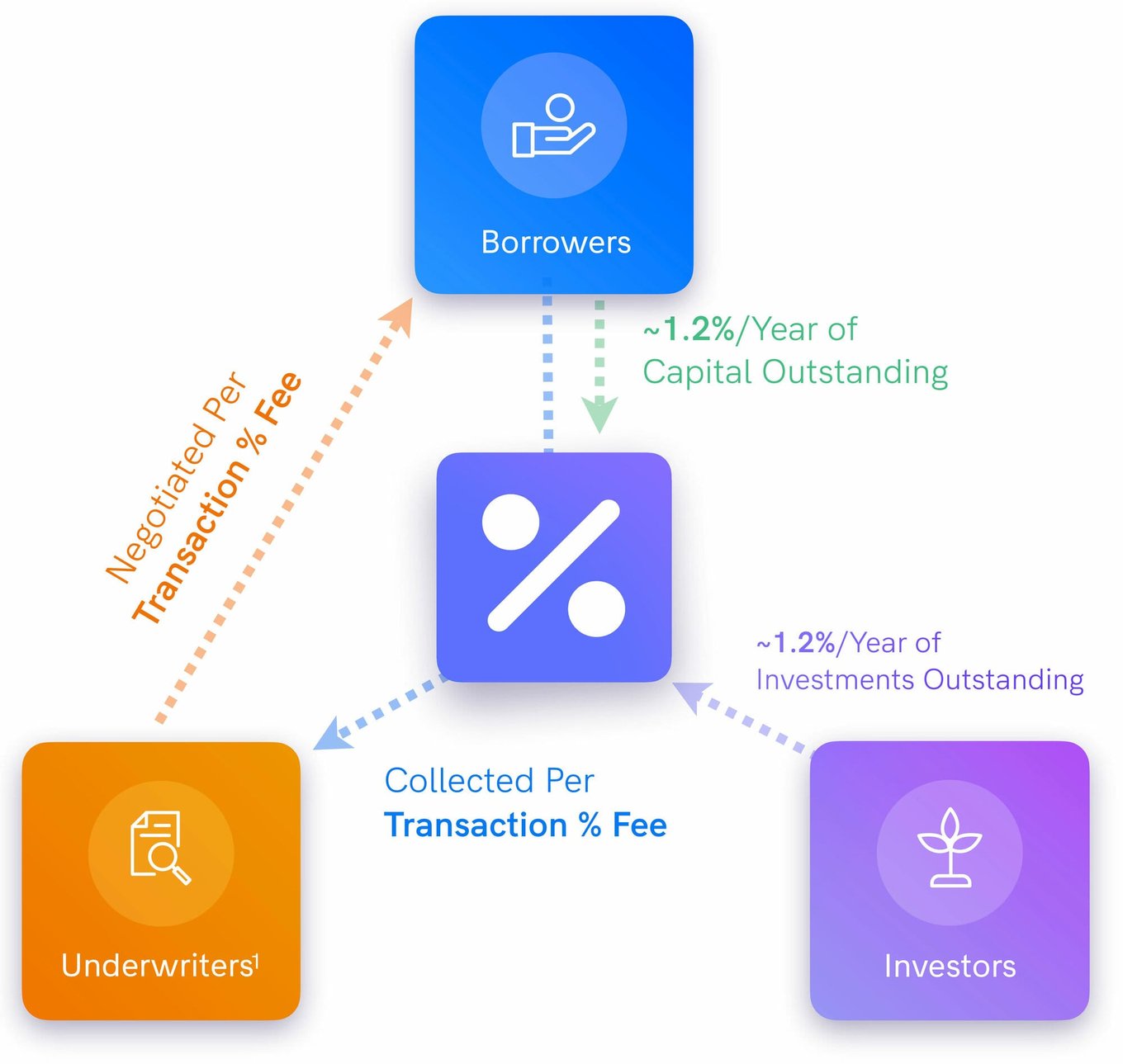

The Percent platform is centered around three core themes for their three target customers. As part of their push to bring public market efficiencies to private markets, they have focused their efforts on creating market standards and data standards while offering credit protection to a well-defined client base. These customers include corporate borrowers seeking debt capital, underwriters structuring these transactions, and investors searching for yield.

Every feature and core technology developed for each of the market participants (borrowers, underwriters, investors) revolves around solving for these main tenets. An overview of these individual platforms below:

While this is not a product in the technology sense, it is foundational for everything they are aiming to accomplish. The past 3 years has taught them the ins and outs of how to structure private debt products. They have applied these learnings towards creating the de facto market standards for the industry that will power the private debt transactions of the future. It is these same market standards that enable new products like credit protection to be developed.

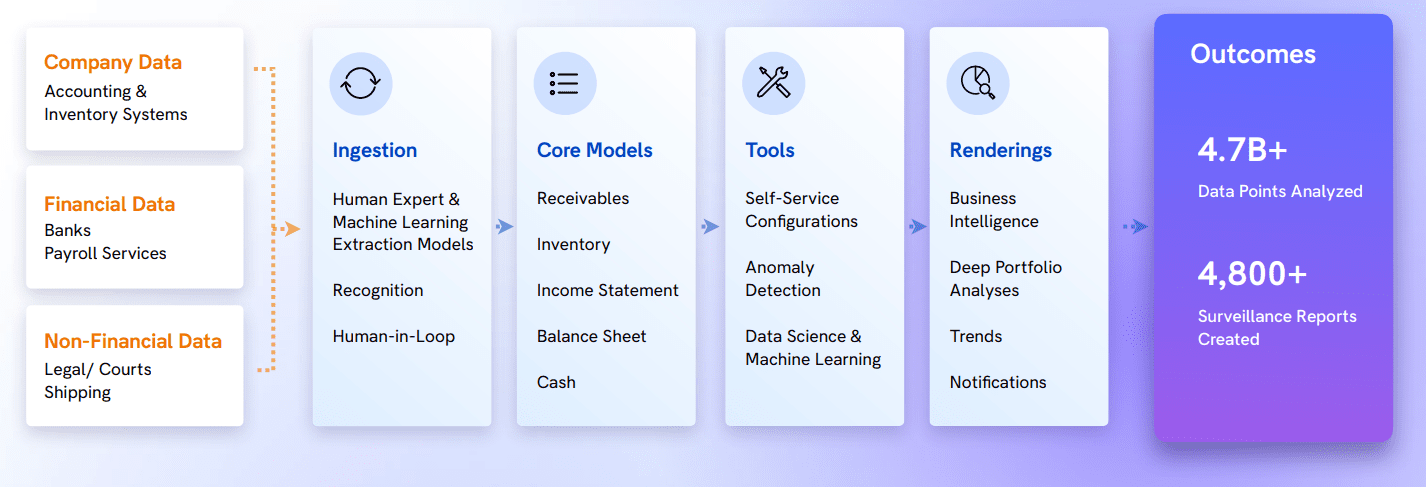

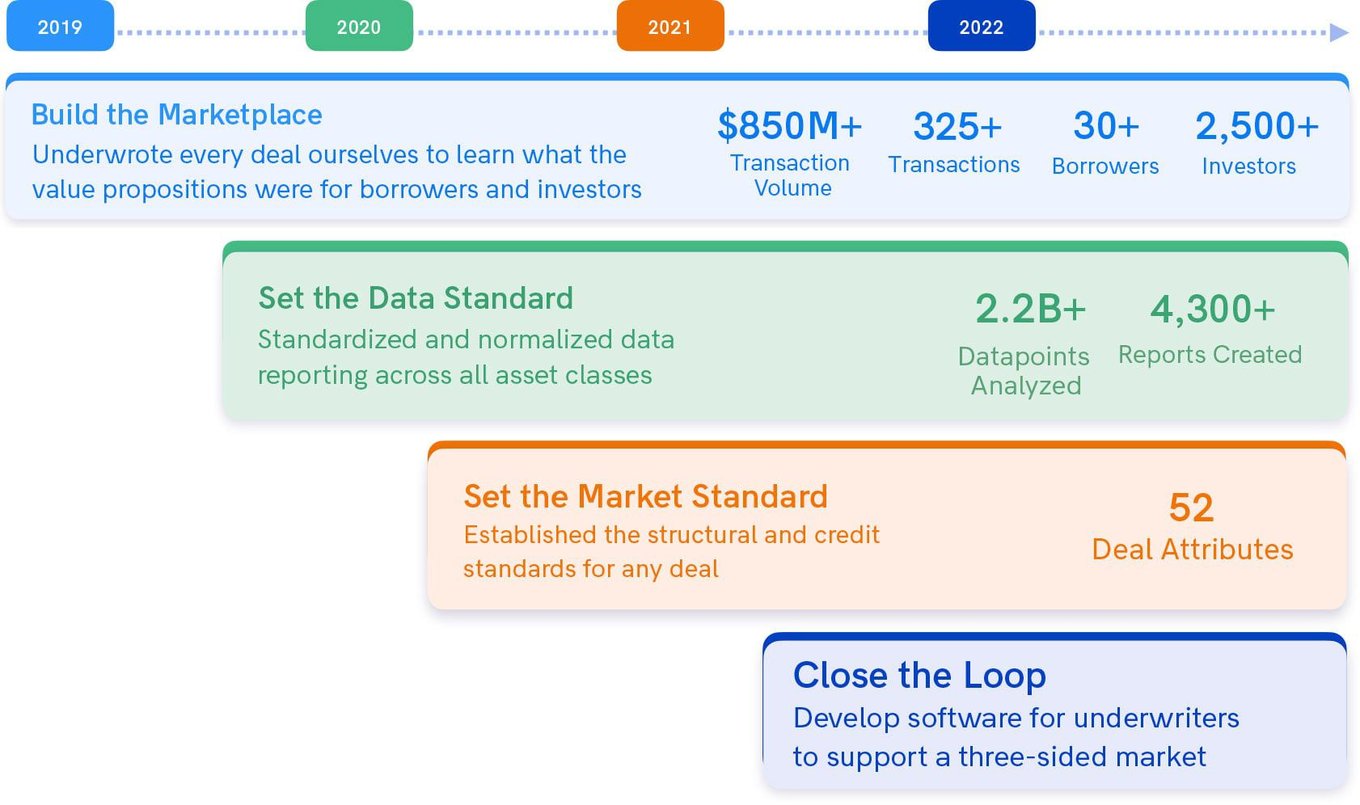

Percent has built out a data product in its own right, having published over 4,800 surveillance reports and analyzed over 4.7 billion data points in the past 3 years. Early on in the company’s life, they recognized the need to standardize the data given how unstructured each borrower’s data were in order to provide consistent reporting and surveillance capabilities for investors.

They have also recently acquired IP from MidCap Financial, a subsidiary of Apollo, which will elevate their data surveillance capabilities even further. While most of the efforts to date have relied on borrowers to upload Excel files, this newly acquired IP enables Percent to directly monitor the underlying assets’ performance in real time. As a result, their surveillance capabilities only become even more robust and they have the potential to be a market leader in this space over time.

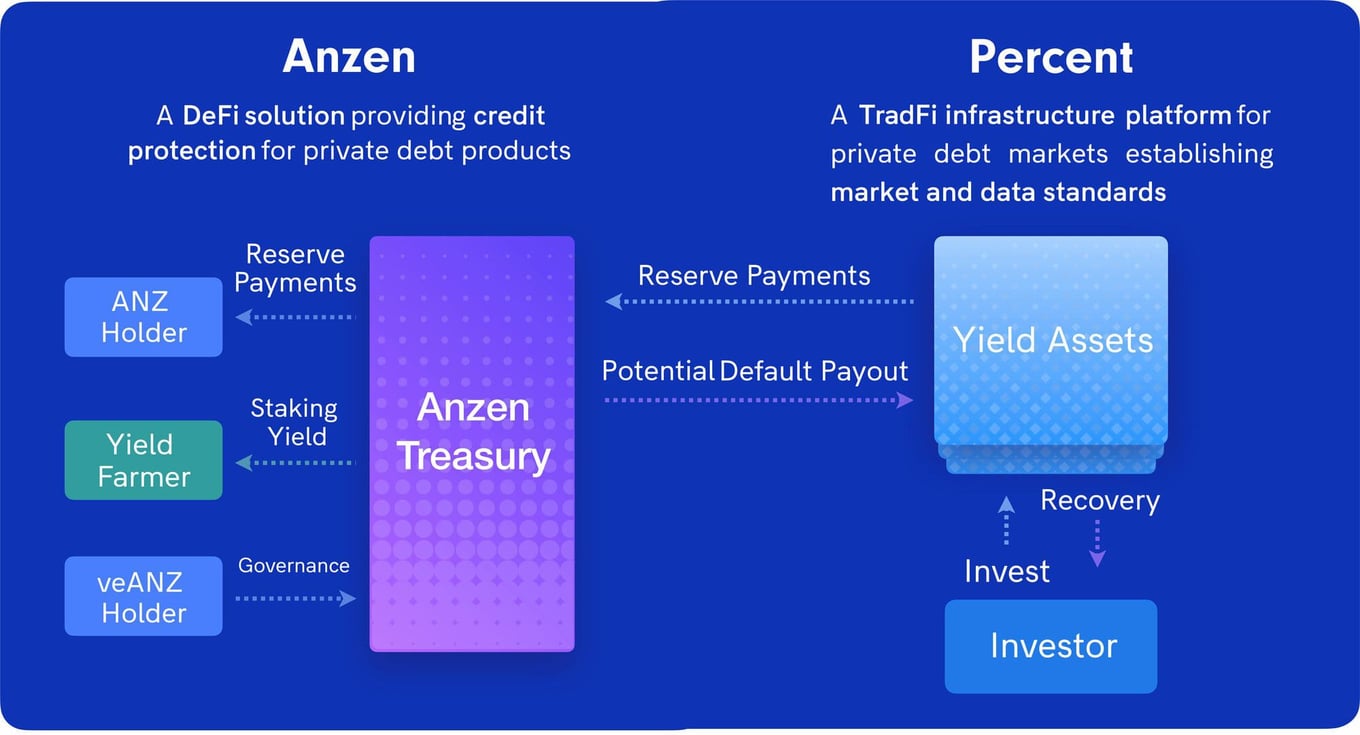

Percent is a strategic launch partner for Anzen, a DeFi protocol providing credit protection for private credit offerings. The company is providing the criteria for what structured products will be considered eligible for coverage by Anzen’s treasury reserve and also defining the workout remedies that must be completed before the treasury reserve pays out in the event of a default. These eligibility criteria were born from the market standards that Percent has created.

As the launch partner for Anzen, Percent has their investment products making payments to Anzen’s treasury reserve, which began in June 2022. This is an industry-first for private debt and another example of how Percent is pushing innovation forward in private markets.

The company booked $1.6M in revenue in 2020, their first full year in operation, of which only $117K (6%) was recurring software fees. They booked $2.1M in revenue in 2021, of which $1.0M (48%) was recurring software fees.

Revenue to date has been limited by their ability to do transactions themselves as the only underwriter on the platform. With the platform opening up for all borrowers, underwriters, and investors in 2022, the company has line of sight into 3X+ in revenue this year, of which 30-40% will come from recurring revenue.

Their conviction on the recurring revenue side stems from the robust pipeline of borrowers and underwriters, many of which are already going through their internal committee approval. The conviction on the transactional underwriting side comes from the mandates that are already signed and actively being marketed for transactions.

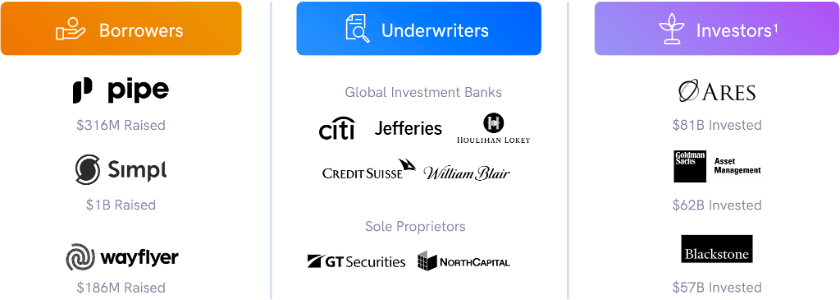

Below are a few examples of the types of potential customers

that could benefit from Percent’s platform:

(1) Private Debt Investor - PDI 100 (2021)

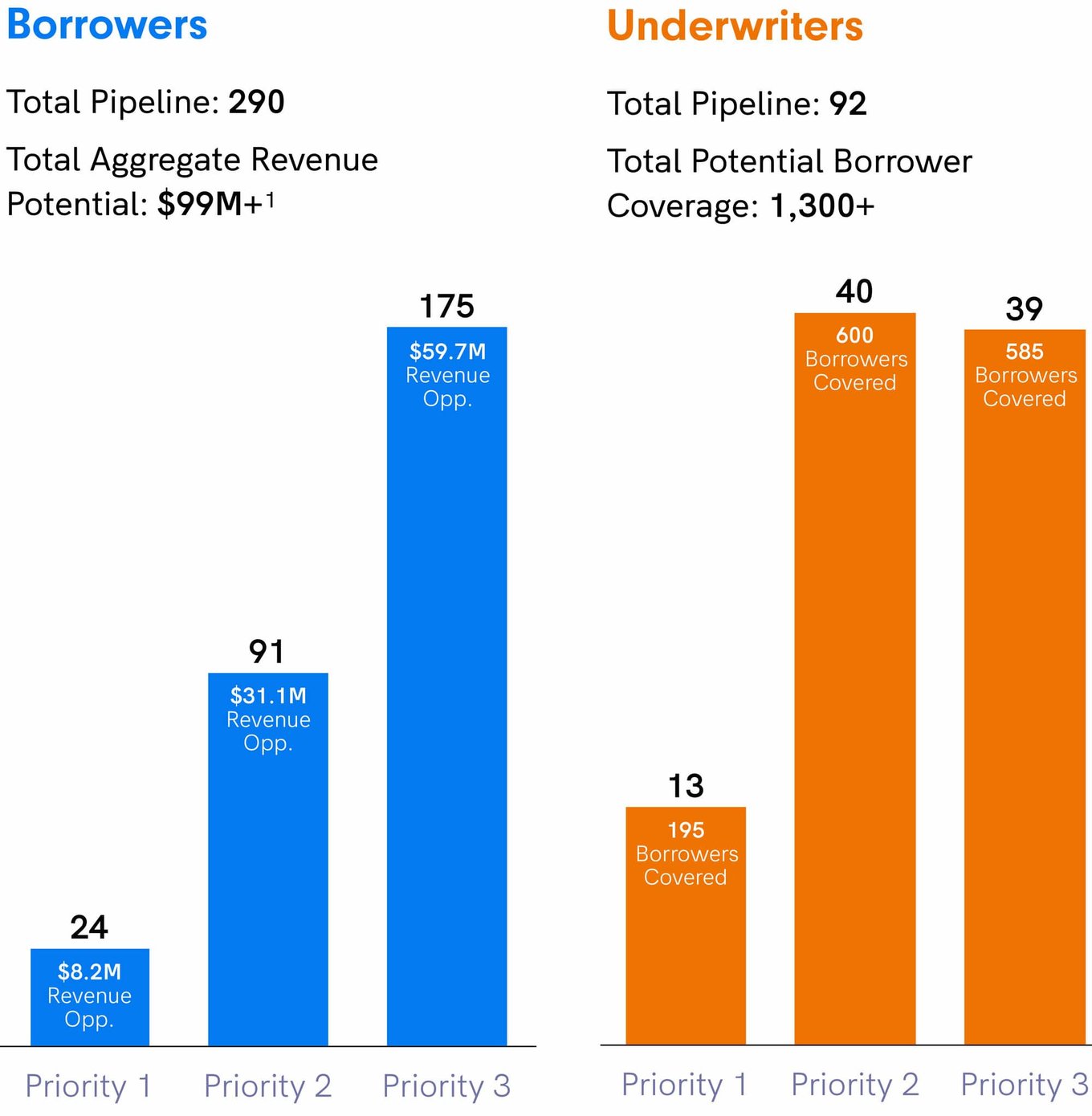

The company’s target borrower for the time being is a fintech lender or venture-backed startup who is seeking debt capital to grow their portfolio or scale their growth. To date, the company has structured or issued investment products for 30+ different borrowers. While they have been in public beta, conversion to date has been limited by their internal team’s ability to underwrite and bring deals to market. This self-imposed limit has led to a robust pipeline of borrowers, with over 290 borrowers making up a $99M+ potential total aggregate revenue opportunity.

A core value proposition of Percent is their ability to see borrowers through their entire debt capital markets life, benefiting their CAC significantly as a borrower only needs to be acquired once before moving them from stage to stage. To augment this, Percent also launched a borrower product with self-registration and access to their proprietary data, leading to a significant increase in sign-ups that they anticipate will bring down CAC even further as they begin to leverage paid acquisition strategies more to reach their target customer.

There are three investor demographics that the company focuses on — small investors (accredited), medium investors (family offices, credit funds), and large investors (institutional asset allocators). Each of these demographics help the platform close on small (<$5M), medium ($5M-$25M), and large ($40M+) transactions respectively. Acquisition has been artificially held back to date as they have been the only underwriters on the platform and deal flow is limited.

Churn is natural on the smaller investor side as they tend to be more fleeting and have different objectives with their investments (e.g. short-term liquidity needs, covering margin calls, life decisions like buying a house, etc.). For these smaller investors, churn has been consistently hovering between 1-3% per month when factoring in a 3 month lookback.

Contrary to borrowers and investors who number in the thousands and hundreds of thousands, the total market of potential underwriters is in the hundreds, ranging from small capital markets deal making teams up through the global investment banks. The company has focused the least amount of effort on acquiring this group since they have been responsible for all underwriting themselves to date.

Still, they have managed to build up a pipeline of over 90 underwriters across the spectrum from small to large. This was built up through the track record and reputation they have built up in the space over the past 3 years and the attention they have been able to garner for their broader vision of being the infrastructure provider for underwriters to generate new revenue opportunities. As a result, acquisition costs are near $0 for the time being, although there will likely be a more defined spend calculated once underwriters come on board by calculating the time effort from the team to convert them into full-fledged customers.

Retention is anticipated to be fairly high as Percent will be relied upon to continue monitoring the performance of their portfolio and no underwriter would want to miss out on the opportunity to source a new potential borrower.

At inception, the company charged a transaction fee model, taking a fixed fee per deal and netting it out of the total capital raised, similar to an investment banking model. The company shifted to a recurring revenue fee structure at the end of 2020 and the impact was immediately felt. Recurring revenue, which made up just 6% of total revenue in 2020, comprised 48% of total revenue in 2021.

In 2022, they have adjusted the model to formalize a recurring fee structure for both borrowers and investors, equating to approximately 1.2% annualized of total assets/investments outstanding for both, booked monthly. Because they play the role of being a core infrastructure provider and as a result, they are also handling all payment flows within their ecosystem. To that end, underwriters who are negotiating their own fees with the borrowers for any transaction will also leverage Percent to collect and distribute payments. While they do not collect a spread on these fees for now, this further entrenches their position as the connection point between all market participants.

Recently, the company has also been able to monetize their data, charging a variable rate of per month, depending on frequency of reporting, to conduct portfolio surveillance for specific borrowers. Credit funds and institutional asset allocators are paying them to offload their surveillance requirements as it is much more efficient and cost effective for a platform like Percent to do the work. Data is core to the company’s business and will play an even greater role in 2023 and beyond.

In the near future, the company will shift beyond just charging borrowers and investors and be able to monetize their underwriters as well. This is expected to be a pure play SaaS model where the company charges per seat per month for access to their underwriter suite of products.

The company's track record of underwriting enabled them to build up a pipeline of borrowers and other underwriters that has the potential to exponentially grow assets outstanding once the platform is opened up for public launch.

1. The rise of embedded finance

Companies like Plaid, Modern Treasury, Rho, and others have laid the groundwork for companies to do better underwriting themselves, becoming more of a fintech company than a traditional lender. The data that is being captured by these companies has never been more available and the ability to create a standardized, normalized dataset off of this firehose of data is now possible for the very first time at scale.

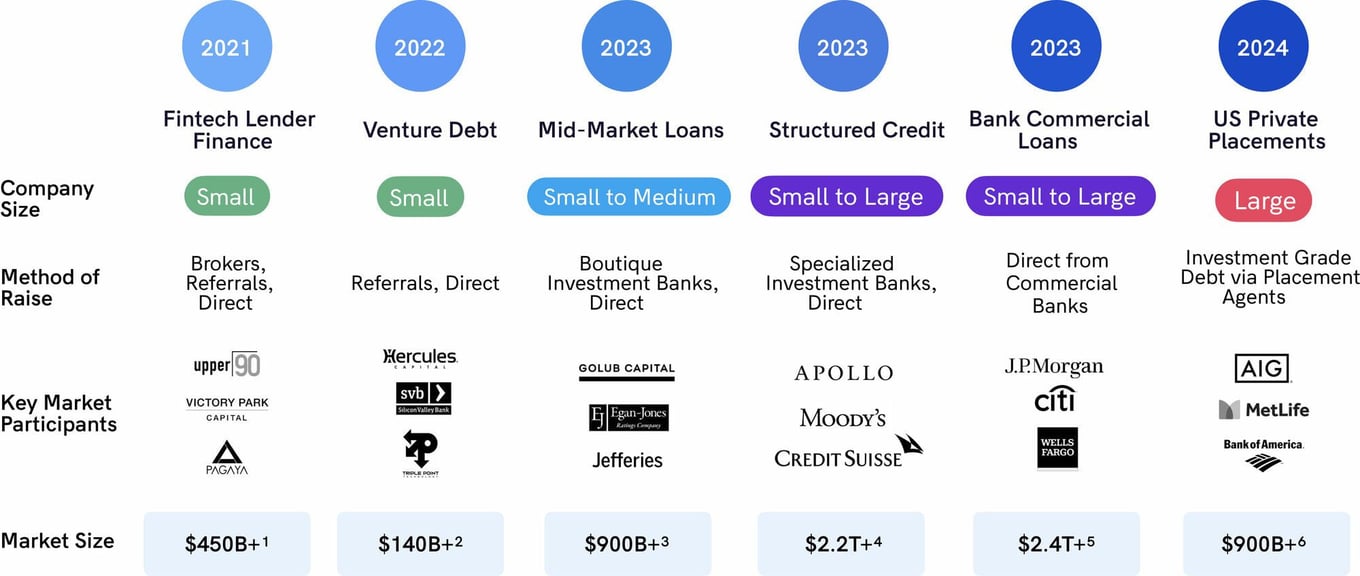

2. The rapid growth of fintech lender finance

Fintech lenders now make up a $450B market. The industry has exploded as a result of the low rate environment and banks stepping back from what once was a core part of their business. COVID made this all the more pronounced, as the number of small businesses and consumers who need capital increased exponentially overnight and the traditional banks struggled to support them. These fintech lenders are now stepping in to fill that gap and will continue to do so for the foreseeable future. The debt capital markets strategy for these companies is the single most critical element of their business as it drives their future growth and the revenue they can generate and still there is no infrastructure for them to turn to today.

3. The demand for private debt

With market dislocation in the broader macro market, there has been a flight to investments backed by real assets. Apollo and Blackstone have indicated they are doubling down on private credit and it is projected to be one of the most important asset classes for the foreseeable future as it is viewed as a recession resilient asset.

Market sizing

There is a tremendous $35B potential annual revenue opportunity that can be captured from this $7T market. Using the high yield market ($1.5T) as a reasonable proxy for annual issuance percentage ($485B issued or 32%) for asset classes that are not readily tracked, approximately $1.8T of the $7T turns over in new issuance every year. A blended take rate of 2%, aligning with Percent’s current business model, of $1.8T equates to the $35B in potential revenue.

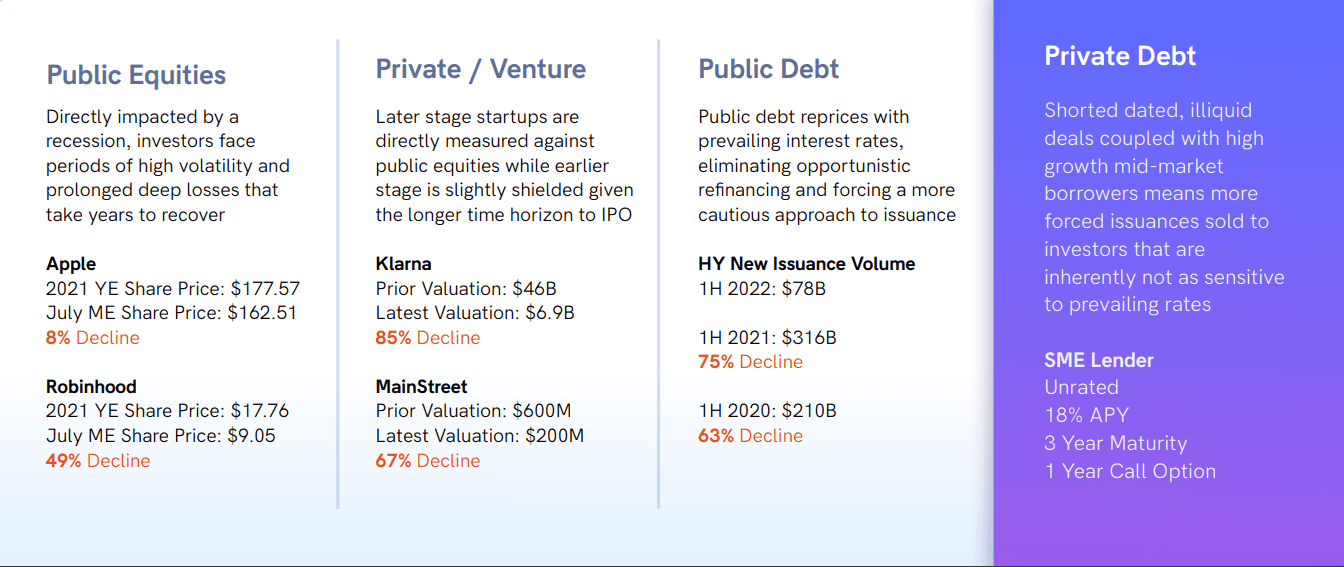

While other asset classes face volatility that materially slow or even shut down new issuance, private debt has historically remained open given the unique dynamics of borrowers and investors.

...in that there is no real direct competition; and if anything, many of these perceived competitors could end up becoming customers if the company reaches true scale.

As part of their asset-based product for lenders seeking debt capital, Percent does not and will never face the underlying SME or consumer who is seeking a loan. These borrowers will continue to rely on the likes of Capchase, Wayflyer, Simpl, and Affirm. It is these types of lenders who need debt capital to fund the growth of their business that become borrowers on the Percent platform.

The majority of these alternative investment platforms have focused so much of their effort around acquiring new assets to syndicate and spending heavily to bring as many investors into their ecosystem as possible. As a result, these companies tend to be extremely sales-, business development-, and operations-heavy when it comes to headcount—instead of staffing up with product and technology.

While some of these platforms view themselves as competitors to Percent, they are essentially underwriters. It is expected that many of these platforms will become customers of Percent’s technology with time.

Private debt market data companies like dv01 are heavily focused on marketplace lending. Only recently have they expanded into mortgage-backed securities and auto loans. These companies are positioning themselves to slot into existing transactions which requires an upsell to investors and underwriters who may be content doing what they do today.

By going downmarket into smaller, earlier stage transactions and solidifying their role in a borrower’s growth story, Percent is integral to the process at a much earlier stage, delivering value where it’s needed most.

There are very few companies actually focused on building the infrastructure for private debt and securitization at all. The industry operates very much on a “that’s the way it’s always been” mentality.

Well-known entrants like Figure ave evolved their solution by moving towards vertically integrating their business across verticals, combining HELOCs, student loans, and payments, all under one full-fledged tech-enabled bank—instead of being a technology provider for securitization transactions.

Percent augments the existing workflows for all transaction participants instead of replacing them, taking an altogether different approach to creating differentiated value add tools and services.

The company booked $1.9M in revenue for 2020, which was the first full year their platforms were live, and $2.1M in revenue for 2021. As part of the evolution of their business model, recurring revenues made up just $117K (6%) of the $1.9M in 2020 versus $1.0M (48%) of the $2.1M in 2021.

Revenue as a whole thus far has been capped by virtue of the fact that they were the only underwriters on the platform during their public beta. With the platform coming out of public beta in 2022, it is projected that their revenues will increase materially this year. The company has visibility into 3X+ in revenue for 2022, with 30-40%+ coming from recurring software revenues and 60-70%+ coming from underwriting transaction fees.

There are no direct market comparables to what Percent is building.

However, there are parallels that can be drawn from recent M&A transactions, publicly traded market data companies, and publicly traded fintech lenders, which can serve as a reference for valuation multiples for Percent.

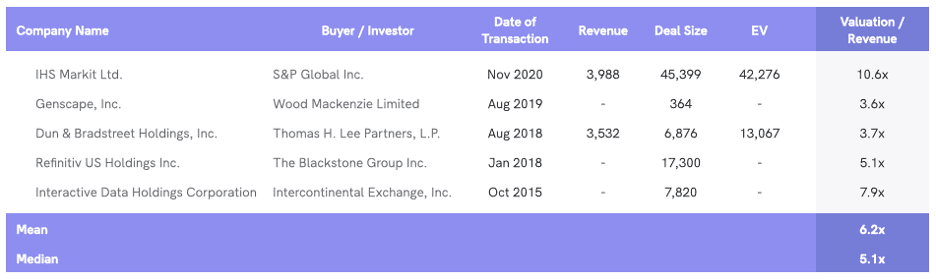

M&A Comparables

Given Percent’s novel platform approach, there have not been many comparable M&A transactions in this specific sector. The most relevant transaction was S&P Global’s $45B acquisition of IHS Markit, a company providing critical information, analytics, and solutions for various industries and markets worldwide. On average, trading platforms and market intelligence companies have been purchased at 6.2x LTM revenue. Given historic trade sales were on traditional data providers, Percent’s tech platform offering should command a higher multiple if it were to pursue a strategic acquisition exit.

This round will be $25M, and the company has raised $21.5M to date prior. Their last priced round was $12.5M at a $43.5M post-money valuation in March 2021.

Nelson Chu is the founder and CEO and Percent is his third company. Prior to Percent, he founded Lumenary—a consulting company for launching startups whose most notable client was BlockFi—and MySupport, a homecare platform that was acquired by a healthcare services company.

Nelson Chu is the founder and CEO and Percent is his third company. Prior to Percent, he founded Lumenary—a consulting company for launching startups whose most notable client was BlockFi—and MySupport, a homecare platform that was acquired by a healthcare services company.

Other key management team members include Prath Reddy, the President, and Vadim Shteynberg, the Head of Engineering. Prath comes with 10 years of institutional debt capital markets experience from investment banks (UBS, Credit Agricole), is a CFA Charterholder, and the architect of the investment products found on their platform. Vadim comes with 25 years of engineering experience, first at IBM and then at IHS Markit before becoming the VP of Engineering at Lukka and Comet prior to joining Percent.

The management team is fairly established at this stage and the primary roles remaining to be filled are the COO/CFO and General Counsel, both of which will be made post-Series B.

Charlie Lienau

Head of Business Development

Mr. Lienau has over 10 years of experience in investment banking, primarily within fixed income. Prior to joining Percent, Charlie was an Executive Director at UBS Investment Bank in New York where he focused on originating and executing public and private financing transactions for Latin American clients across various industries, including government financial institutions, and corporations in the real estate, utilities, and retail sectors. Mr. Lienau obtained his undergraduate degree in Economics from Universidad de San Andres in Argentina and received an MBA from Columbia Business School with graduation honors with distinction.

Gary Reifman

Head of Product

Mr. Reifman has over 20 years of experience delivering solutions to the global financial services industry. Prior to joining Percent, he headed product at several prominent New York-based startups, including Lukka, Orchard Platform and Dataminr. Previously he was a Managing Director at IHS Markit, where he was responsible for real-time data, global desktop and distribution for the firm’s information business. Mr. Reifman earned a Bachelor of Science in Computer Science from Rutgers University.

Jessica Zall

Head of Marketing

Ms. Zall has over 20 years of experience in financial services and financial technology. Prior to joining Percent, she was Senior Vice President and Global Head of Marketing and Communications at Capitolis, where she spearheaded the buildout of the firm’s marketing and brand strategy and helped to lead them through a $90 million Series C funding round. Before joining Capitolis, Ms. Zall was the Global Head of Marketing Strategy at Renitiv where she developed and led marketing strategies that drove commercial value and retention for the firm’s platform and data solutions. Prior to that, she was a senior marketing leader with J.P. Morgan, Envestnet, BNP Paribas, FundQuest, and Reval. Ms. Zall holds a Bachelor’s degree in Psychology and a Master’s degree concentrating in Economics, and is a member of Chief, The Women’s Bond Club, Wall Street Women’s Alliance, and Women in FX.

Michael Kendrot

Head of Capital Markets

Mr. Kendrot has over 25 years of experience in financial services advising corporate issuers seeking to raise debt capital across a variety of industries and currencies. In his most recent role, Mike was Managing Director and Head of the Americas for the debt capital market team at Credit Agricole CIB. Mike was responsible for originating, structuring and executing debt financings for the bank’s clients. Mike has held similar roles within debt capital markets at ABN Amro, Credit Suisse and Barclays. Mr. Kendrot obtained his undergraduate degree from the College of the Holy Cross and his MBA from Columbia Business School.

Nelson Chu

Founder and CEO

Mr. Chu is a third-time founder with one exit in the healthcare vertical. At the outset of his career, he held several positions at top financial services firms, including Bank of America and BlackRock. Prior to Percent, he founded a strategy consulting firm specializing in helping companies build products and scale their business, creating over $1B in equity value. He earned a Bachelors of Arts in Economics and Political Science with a minor in Philosophy from Rutgers University.

Prath Reddy, CFA

President

Mr. Reddy has over 12 years of experience in financial services, primarily within investment banking. Prior to joining Percent, Mr. Reddy was a Director at UBS Investment Bank within their debt capital markets group based in New York. He has originated, structured and executed numerous fixed-income securities for both public and private corporations across various sectors and global markets. Mr. Reddy earned a Bachelor of Science in Business Administration with a Finance concentration from Northeastern University and is a CFA® charterholder.

Rohit Bharill

Head of Credit

Mr. Bharill has over 14 years of experience in structured finance, with expertise in a large variety of synthetic and asset-backed securities from his experience at various credit trading desks and rating agencies. Prior to joining Percent, Rohit was a Managing Director at Morningstar Credit Ratings and headed their ABS and CLO ratings group. Prior to Morningstar, Rohit worked with Moody’s in their ABS group, and with Nomura and Lehman Brothers at their credit flow trading desks. Mr. Bharill earned a Bachelor of Technology in Mechanical Engineering from Indian Institute of Technology – Bombay, and later earned a Master of Arts in Mathematics of Finance from Columbia University.

Vadim Shteynberg

Head of Technology

Mr. Shteynberg has over 20 years of experience in building complex, real-time, high volume products that modernized the global financial services and digital assets industry. He has had extensive experience growing and managing international technology teams from small startups through IPO to multibillion-dollar corporations. Prior to joining Percent, Mr. Shteynberg was heading engineering teams in industry leading machine learning, blockchain, and crypto asset startups. Previously, he was heading software development for IHS Markit's Managed Services division. Mr. Shteynberg earned a Bachelor of Arts in Computer Science from New York University.

Invest in the app