Jumpstart Parametric Earthquake Firm on Move in West

·

Jan 22, 2021

Jumpstart Insurance Solutions Inc. is on the move in the earthquake-prone West - and the company is now working with insu...

Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

Explore new investment opportunities:

View companies raising now

And most of us have little to no financial cushion:

Public aid? Often too little, too late.

Insurance? Floods and earthquakes are routinely excluded. Even where it's available, only 1 in 10 people opt-in. Disaster coverage is notoriously costly, complicated, and slow.

Savings? What savings? A majority of Americans can't even cope with a $500 surprise.

A recent McKinsey report emphasizes the market opportunity of insuring natural catastrophes.  Building financial resilience is also a social imperative. The UN Sustainable Development Goals emphasize the role of disaster risk reduction.

Building financial resilience is also a social imperative. The UN Sustainable Development Goals emphasize the role of disaster risk reduction.  By building disaster resilience for individuals, Jumpstart speeds up recovery for whole communities.

By building disaster resilience for individuals, Jumpstart speeds up recovery for whole communities.

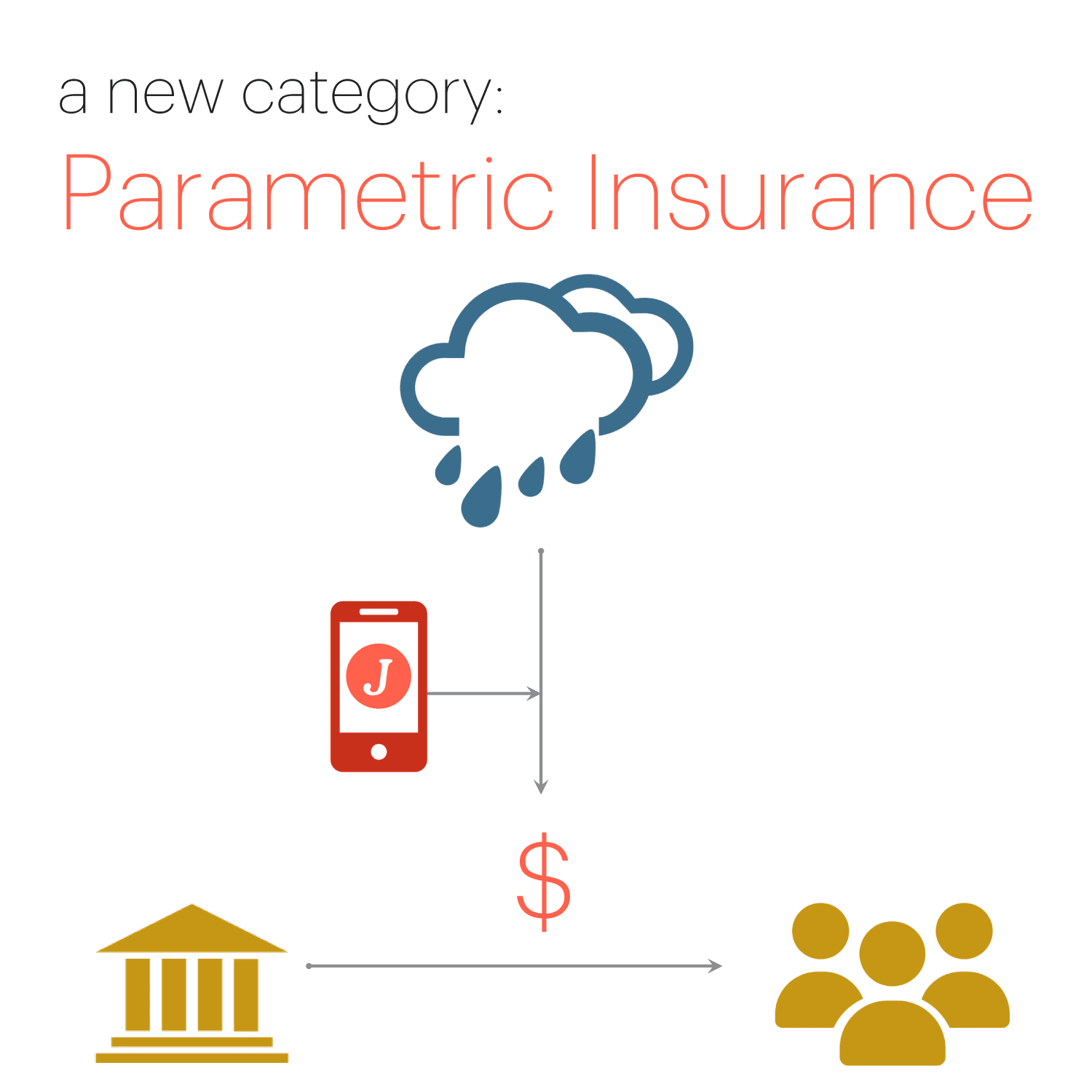

Jumpstart provides a financial jumpstart after the shock of a natural disaster, through a new product category: parametric insurance.

Parametric uses technology to pay a lump-sum immediately after occurrence of a pre-specified data metric. Jumpstart was the first to bring parametric to consumers in the US.

Parametric transforms disaster insurance from being costly, complicated and slow, to frictionless and affordable, and fast. In this way, we fulfill our mission to make money available to more people, right when they need it most.

Jumpstart is like a first-responder for your finances. It's like having a disaster savings account, except for the part where you have to save.

We keep all the good parts of insurance - getting money when you need it - while eliminating the high costs, hassle, and delay.

Our initial product pays customers $10,000 right away after a large earthquake in California.

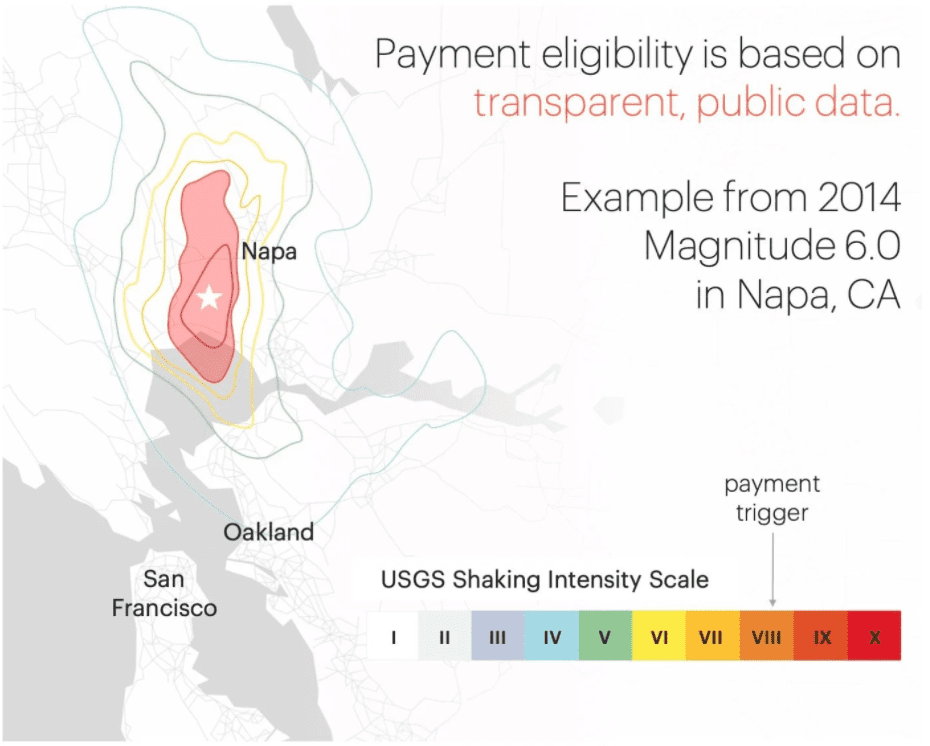

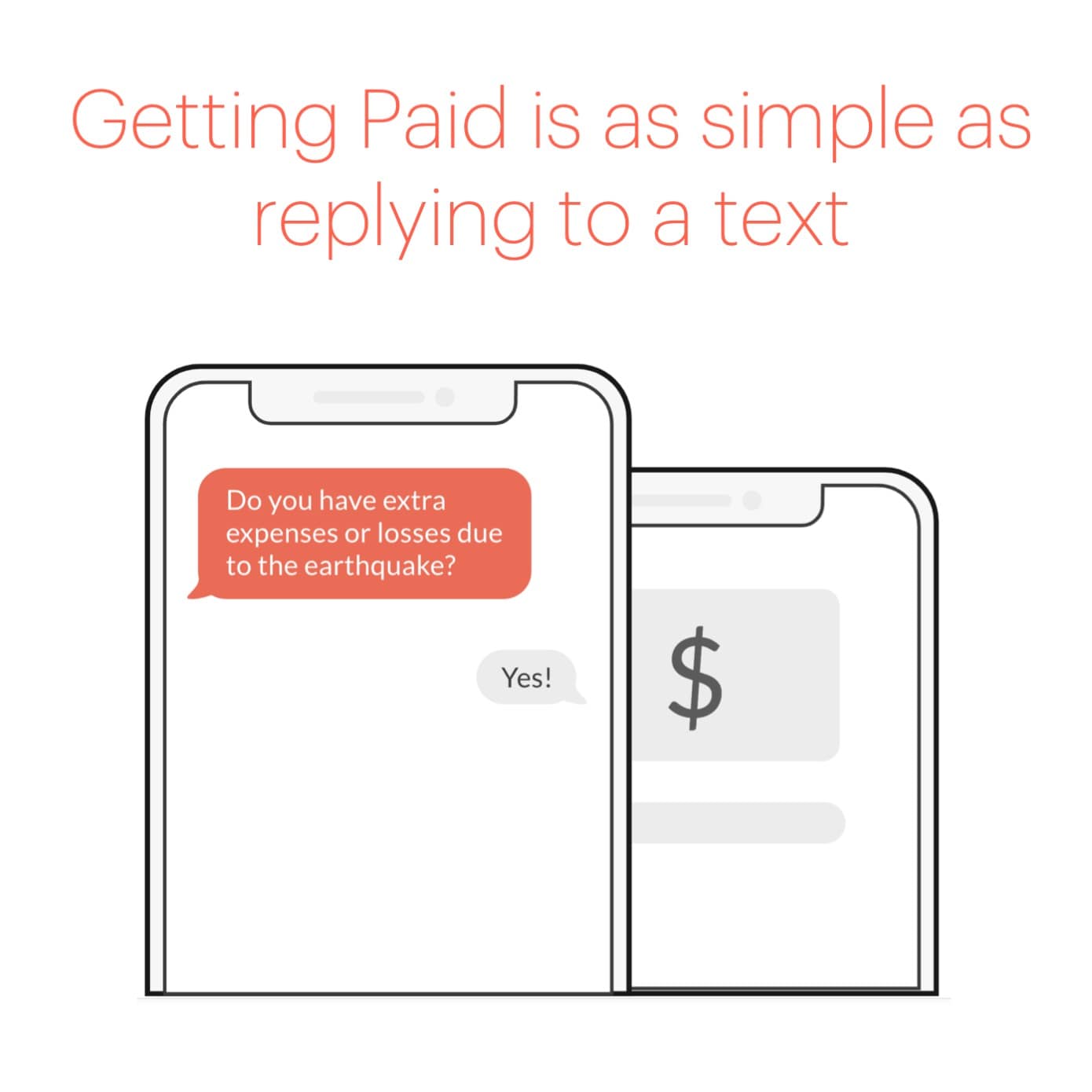

Here's how it works:

Here's how it works:

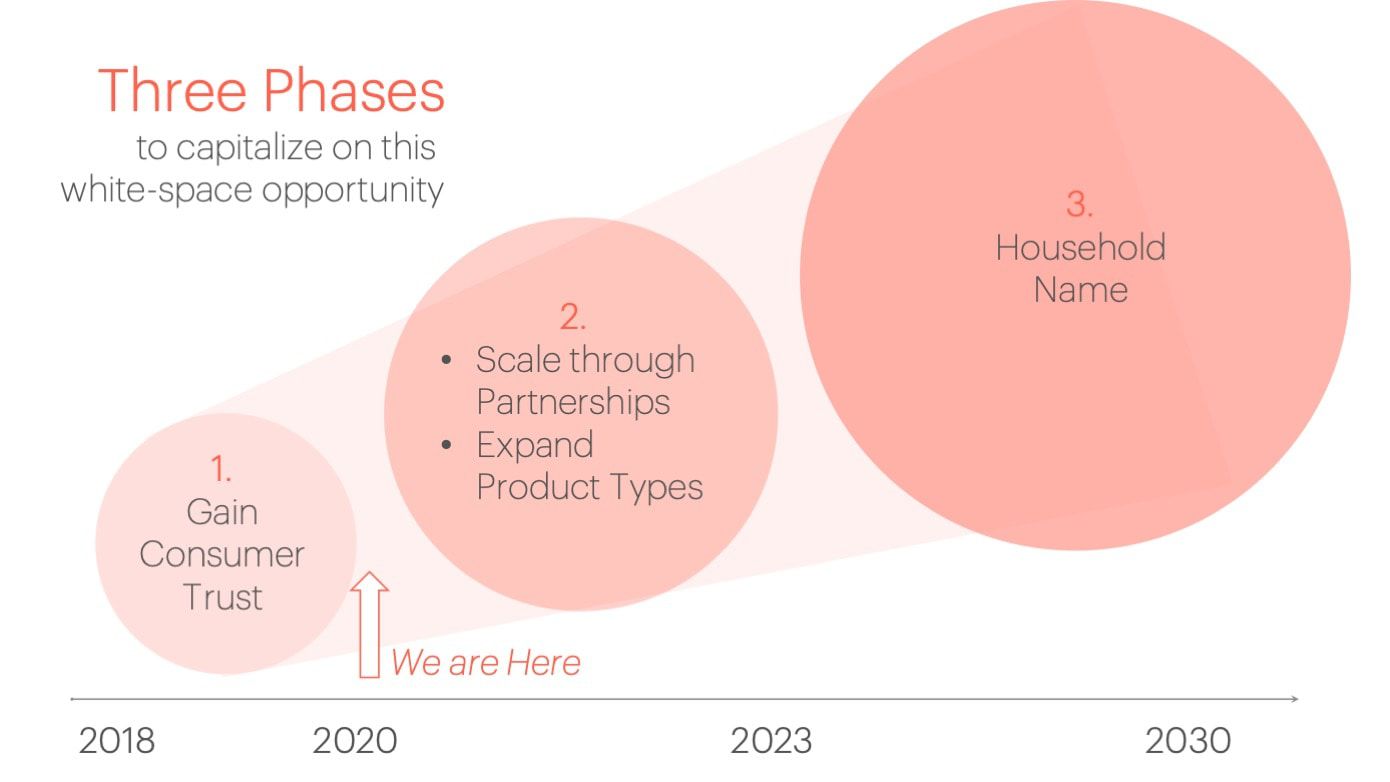

Jumpstart launched our first-of-its-kind parametric product in October 2018. We're executing a growth strategy specifically tailored for a first mover in this new category.

Our prior raise on Republic attracted nearly 4,000 investors and more than $900k. With those funds we accomplished key milestones in our growth strategy:

We've also attracted press coverage: both mainstream and from the insurance industry.

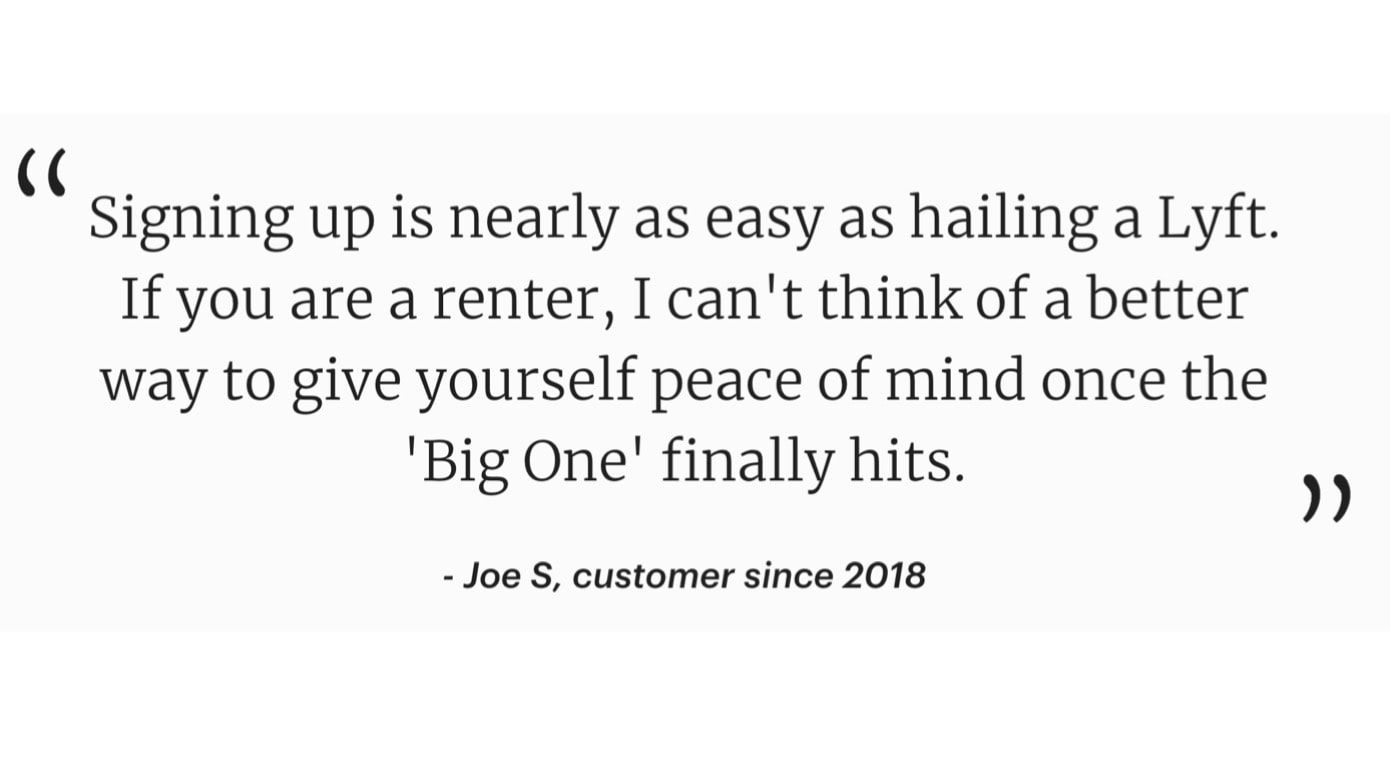

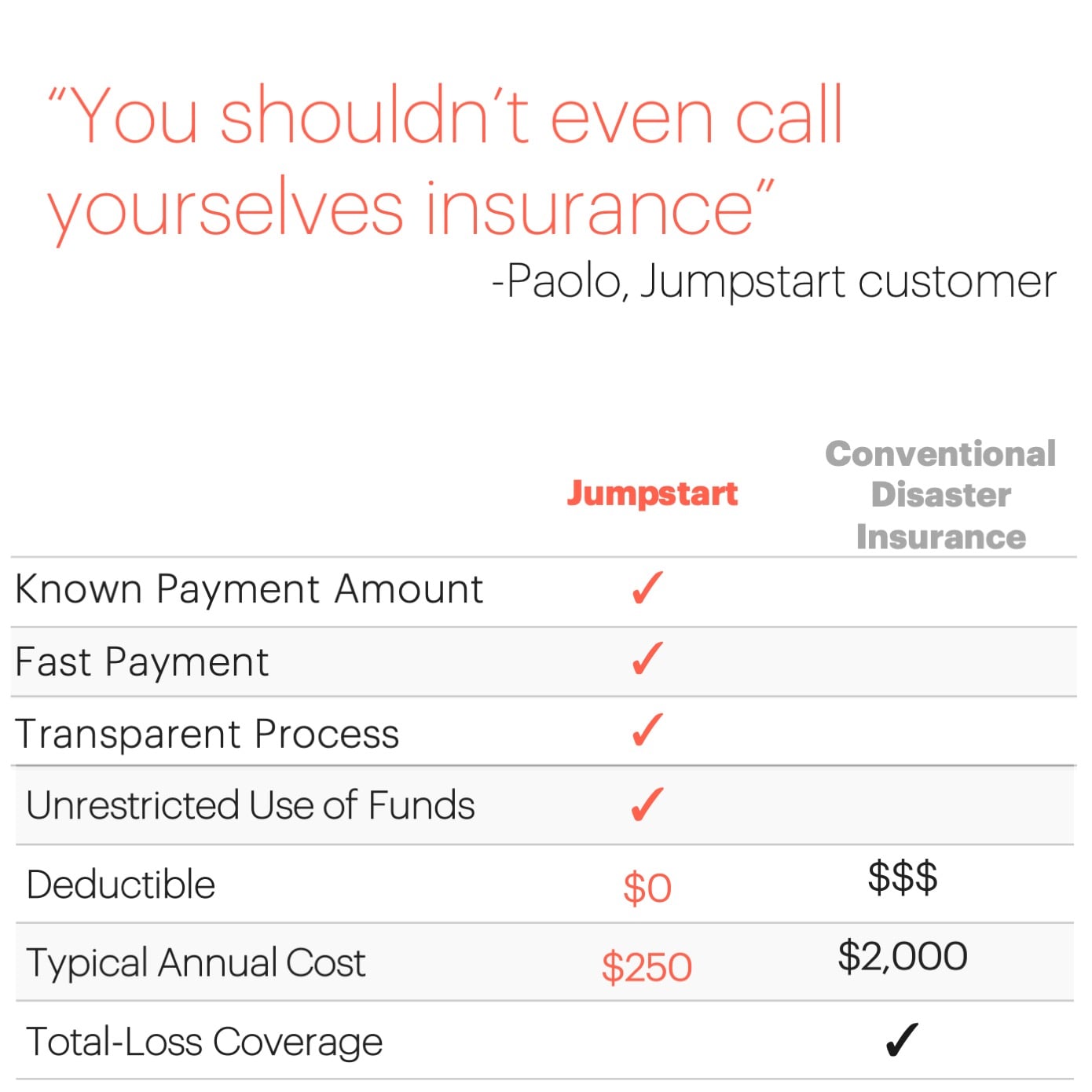

Customers love Jumpstart. We know because we've talked to them - literally hundreds of them. Time and time again we hear testimonials like these:

The data tell the same story. We're seeing metrics that indicate a clear value proposition:

The data tell the same story. We're seeing metrics that indicate a clear value proposition:

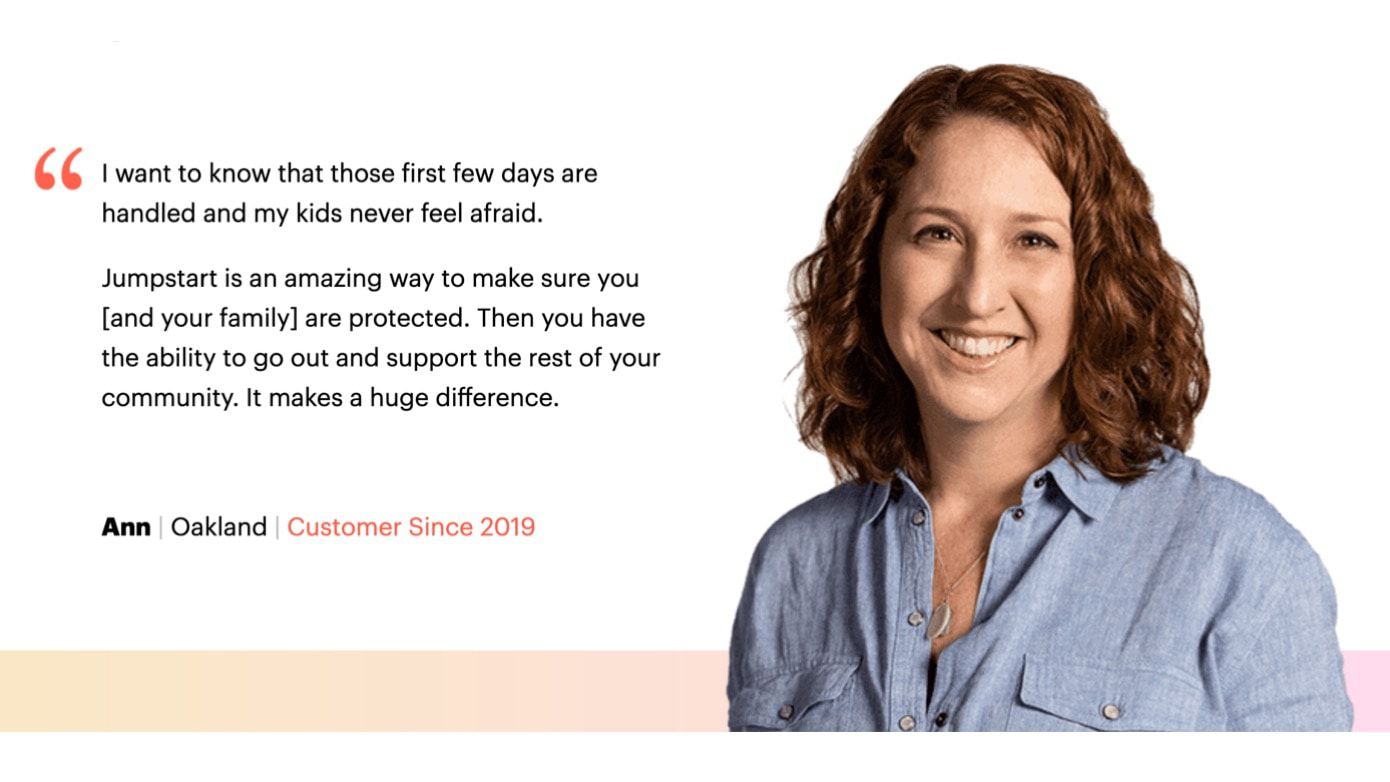

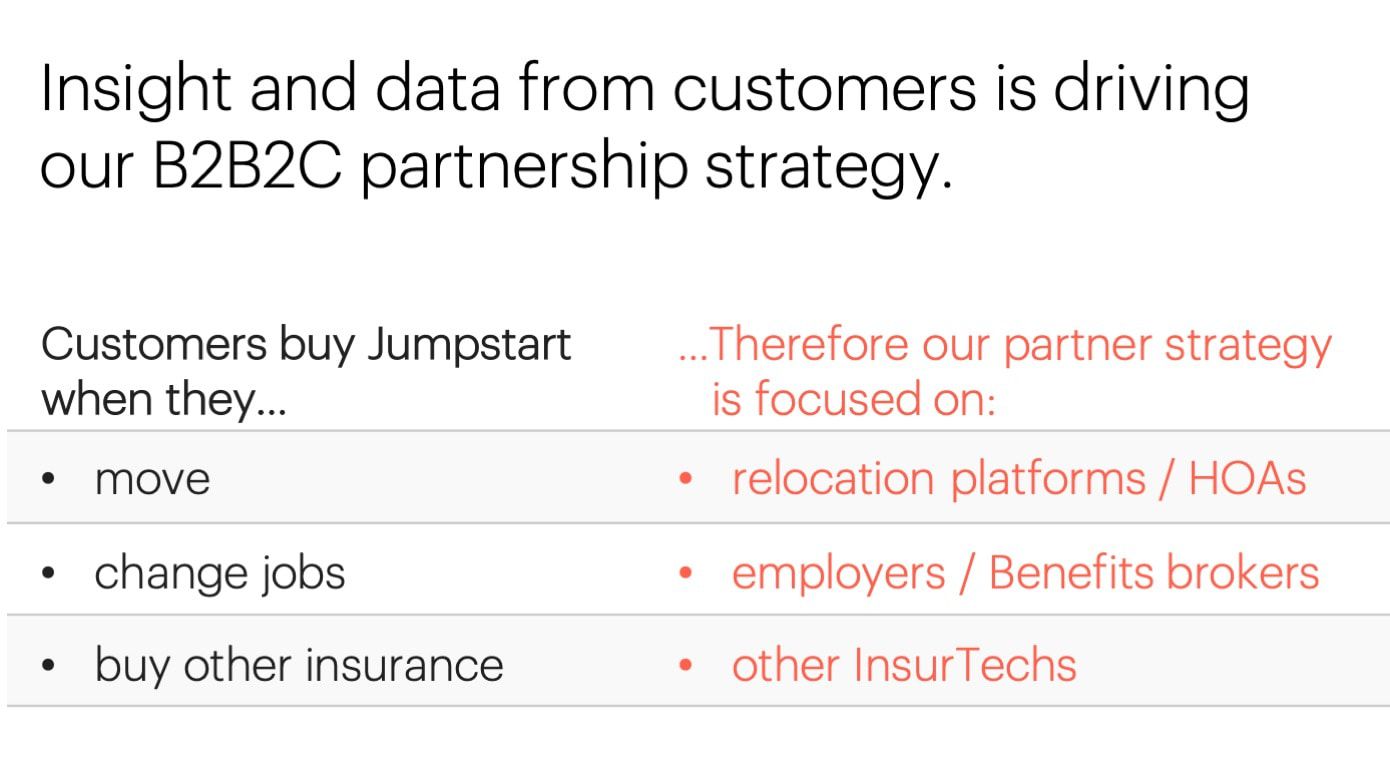

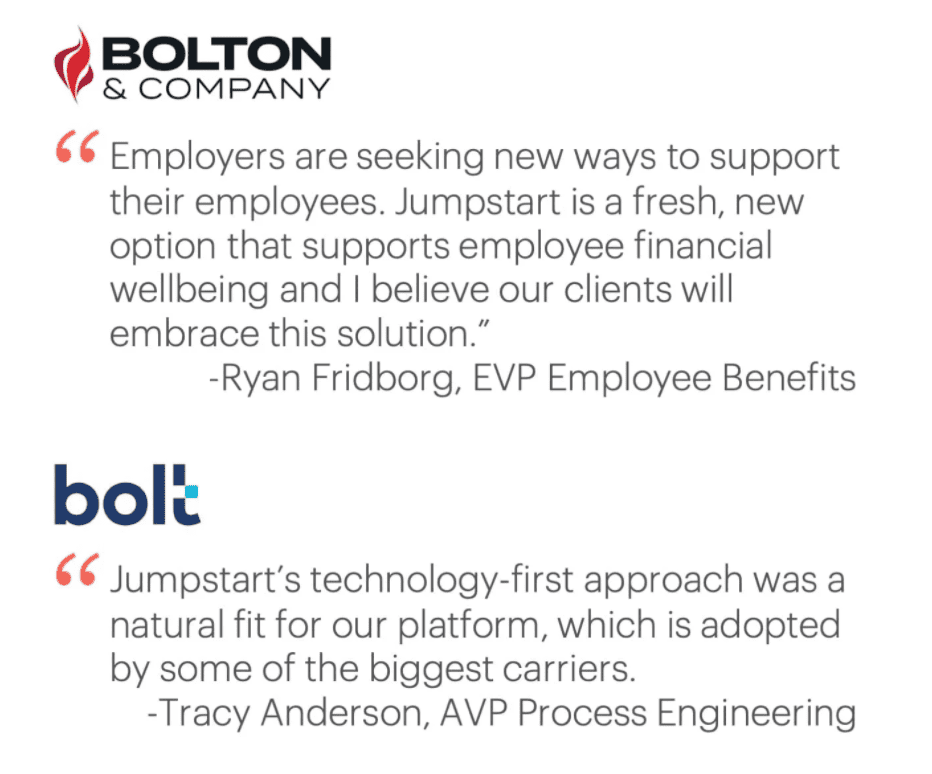

We're also learning from our customers when and why they buy Jumpstart. And as we add B2B2C partners, we're getting more rave reviews:

And as we add B2B2C partners, we're getting more rave reviews:

We earn a recurring-revenue insurance commission, while bearing no risk of making post-disaster payouts. We work with underwriters at Lloyd’s who take responsibility to make payouts.

Customers pay an average of $250 per year, and we retain a typical commission of 25%.

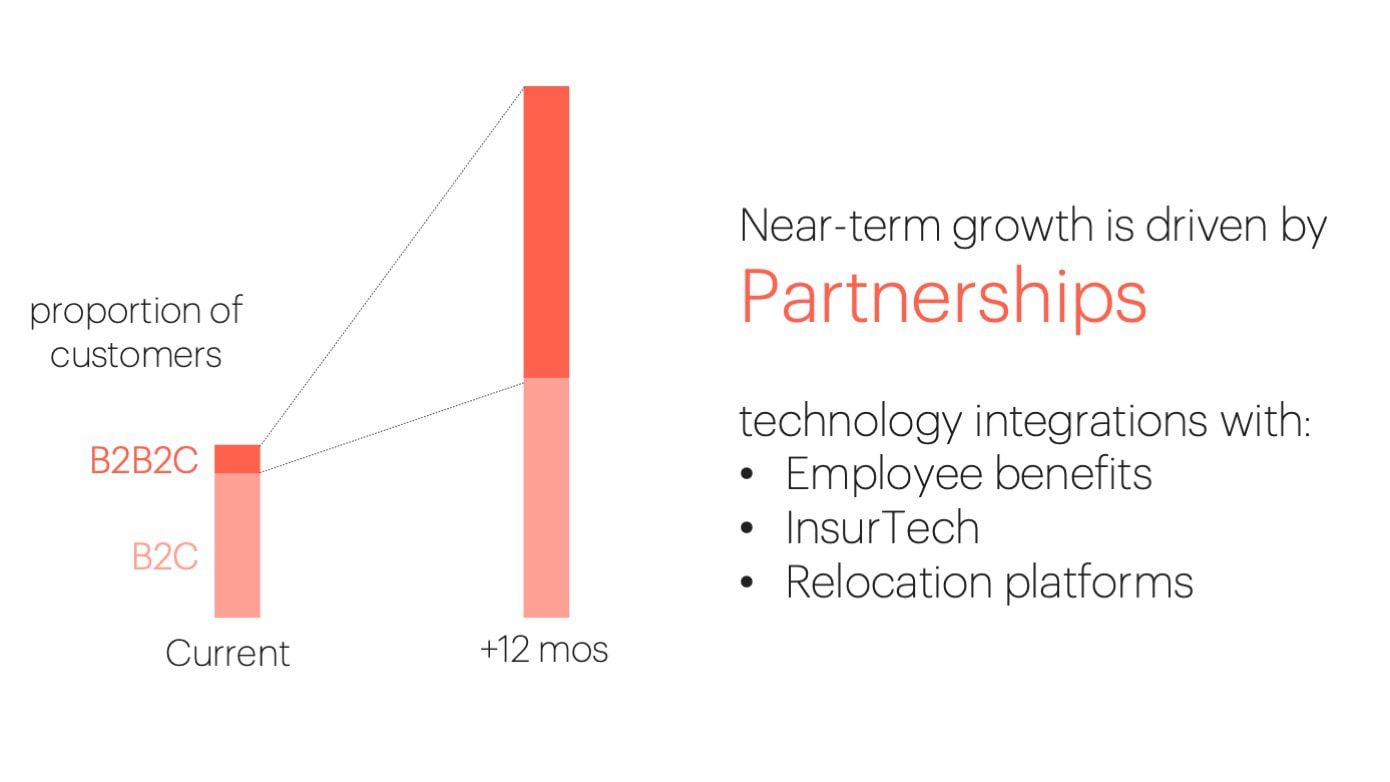

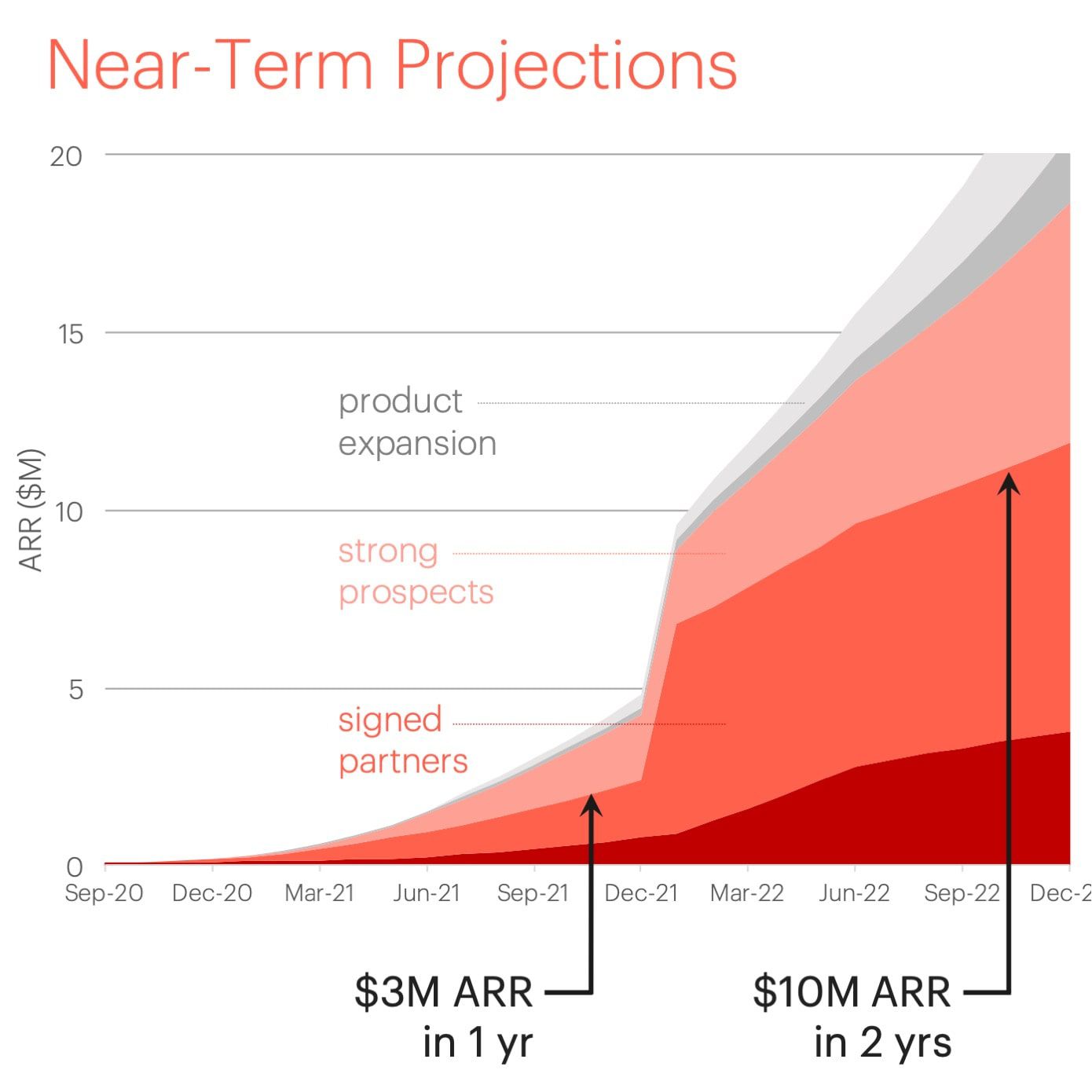

We project 10x growth per year for the next two years, driven mainly by partnerships.  As of December 2020, we have signed agreements with 12 partners with a collective 300,000 potential customers.

As of December 2020, we have signed agreements with 12 partners with a collective 300,000 potential customers. The late-2021 jump represents one of the largest California employers, who has plans to offer Jumpstart as a voluntary employee benefit.

The late-2021 jump represents one of the largest California employers, who has plans to offer Jumpstart as a voluntary employee benefit.

Our most likely exit opportunity will be acquisition by a large incumbent within 4 to 10 years. By that time, we project 400,000 customers, 3 to 5 disaster types, and $100M of revenue.

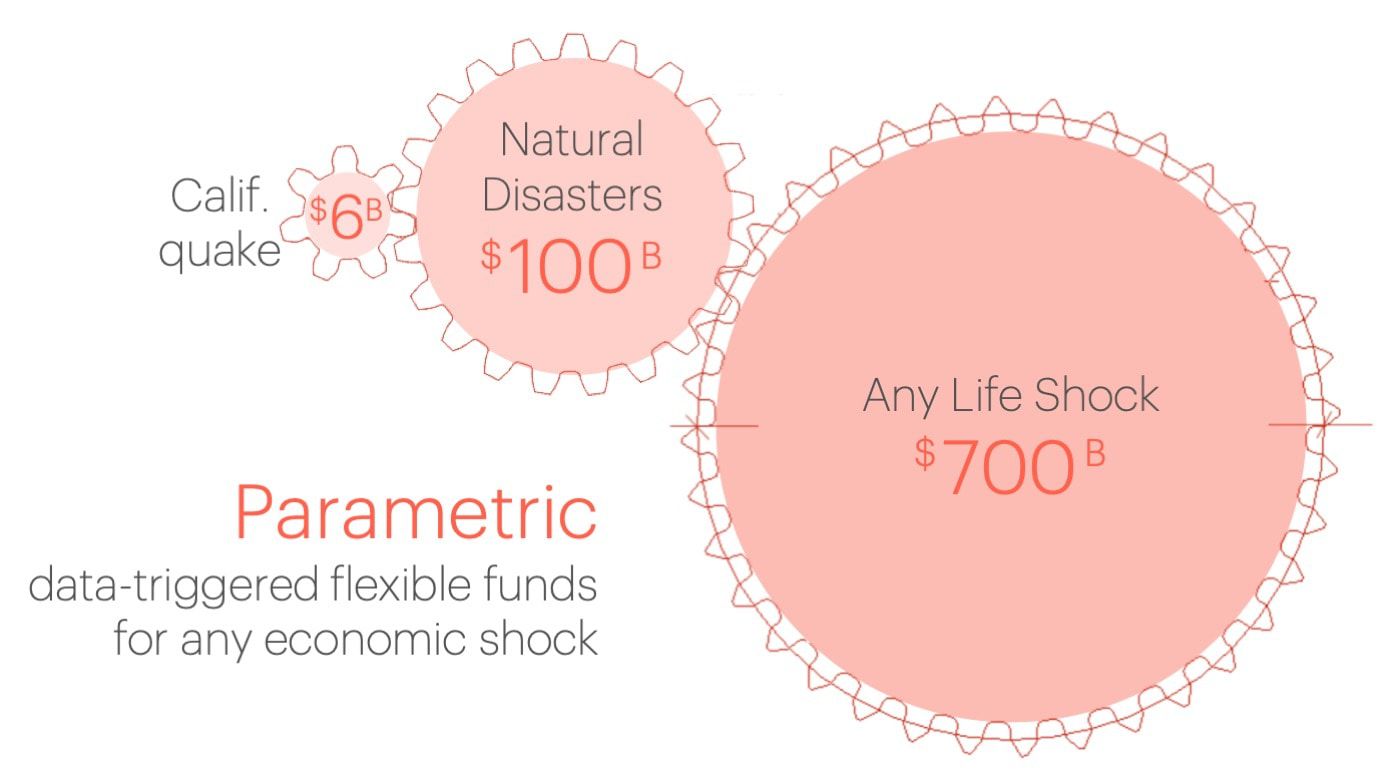

The insurance market is $1.6T. But for each amount insured, untold emerging risks go un- or under-insured: cyber, pandemic, climate change, and more. These create major insurance gaps with a market size in the hundreds of billions.

For natural disasters alone, this "protection gap" exceeds $150B annually. Even if we capture less than 1% market share, we become a billion-dollar company.

Here's how we "gear-up" this massive market potential:

The Jumpstart experience is so opposite from conventional insurance that one customer told us, Our customers love that they can use Jumpstart money for any extra expense, even if they have no damage.

Our customers love that they can use Jumpstart money for any extra expense, even if they have no damage.

We may have been first-mover, but parametric insurance is catching on. It's so appealing that a large-scale incumbent has created a copycat product - but at double the price.

Why? In typical insurance, there are 4 to 5 "middle men" who each skim 5-20%, which can double the cost to the consumer.

With our full-stack of technology, Jumpstart can remain the only intermediary between the customer and the risk-bearing entity.

We pass along this savings to the customer, while keeping enough upside to grow profitably.

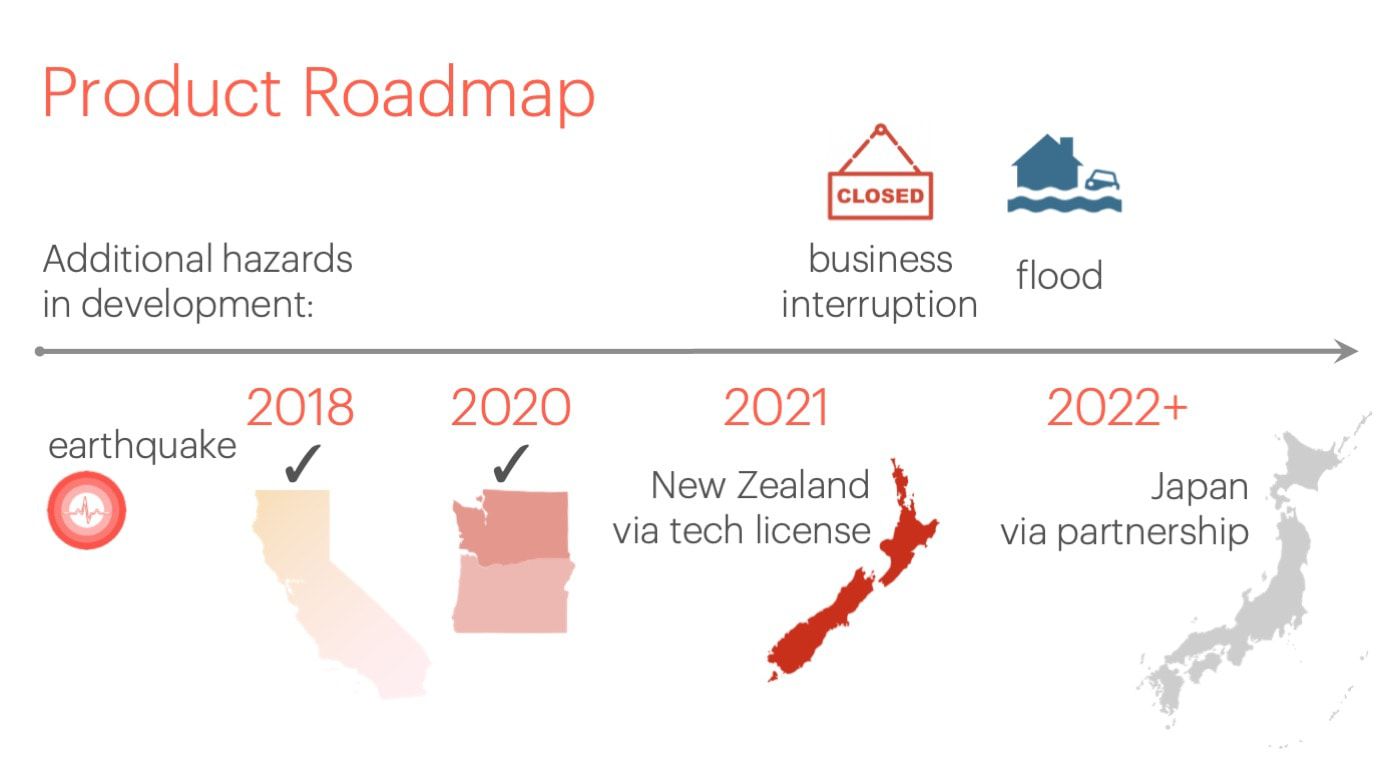

Floods are the natural next step for Jumpstart's parametric approach. Like earthquakes, they are routinely excluded from normal coverage.

However, floods occur more often. The more frequent the hazard, the sooner we'll have "success stories" of delighted customers, and the sooner we'll go viral.

In the meantime, we're exploring how parametric can buffer small businesses from shocks in their revenue - no matter what caused the shock, from natural disaster to pandemic.

Our larger ambition is for a "jumpstart" policy to become synonymous with any insurance that pays an immediate lump sum - to be the defining brand of this new consumer category.

Our larger ambition is for a "jumpstart" policy to become synonymous with any insurance that pays an immediate lump sum - to be the defining brand of this new consumer category.

We're thrilled to be back on Republic. Our previous campaign generated a resounding vote of confidence from almost 4,000 investors.

We're especially heartened to share our journey with those of you who know first-hand what it takes to recover from disaster. (After 2020, that's all of us.)

We'll use funds from the current raise to reach milestones that will fuel our growth and multiply your investment:

Our chances of success have never been higher. We've already received one inquiry from a prospective acquirer. But for now, staying independent will retain more upside for investors.

Founder and CEO Kate Stillwell has 20 years of domain expertise in the science and risk of earthquakes.  Kate recounts the origin story of Jumpstart:

Kate recounts the origin story of Jumpstart:

"At the time of Hurricane Katrina I was a practicing structural engineer. But I realized there's more to disaster recovery than safe buildings. A big missing piece is getting enough post-disaster funding."

In business school Kate learned about large-scale parametric financial instruments. She wondered, why couldn't we create micro-parametric insurance for consumers? Thus the idea for Jumpstart was born.

Kate is joined by a leadership team with the experience and credibility to execute and adapt.

Yes, and we've already started expanding geographically! We also intend to expand to other natural disasters, and that's one of the main reasons we're crowdfunding. We are very keen on the potential of introducing parametric insurance for flood risks.

Many more people than who buy it now! If you ask anyone in California if they believe the Big One is coming, they will answer "of course." What's missing is product options.

Here are some numbers that show untapped demand: Before the 1994 Northridge earthquake, about 28% of people bought it (the cost was about 1/3 in today's dollars). Now about 10% of people buy it. So we believe we can unlock triple the current market simply by introducing a simpler, lower-cost option.

Fundamentally, this is a build-vs-buy question. And the answer is different relative to other startups vs. incumbents.

To other startups, the barrier to entry is enormous - it takes years of prep across multiple disciplines, without a product in market. The startup needs both a 3-year runway as well as domain-expertise credibility with both the regulator and the risk-bearing partners. For an insurance product, you cannot start selling until all the tech is "done" (not just MVP) - thus the appeal of licensing our technology.

To an incumbent, there is significant advantage to waiting on the sidelines until the market is proven by others, rather than large expenditures on an untested product category with regulatory questions.

Technology is the lynchpin of Jumpstart's value proposition. Even though our main product is an insurance policy, selling it wouldn't be possible without the technology we built.

Our technology is so core that we've been sought out by multiple prospective licensees our technology to bring other parametric insurance products to market. This represents an interesting secondary revenue stream.

We built in-house and own four technology platforms:

About 60% of our customers are homeowners and 40% are renters. They span age, gender, and race. The common theme is that our customers think about Jumpstart relative to their savings and their preparedness, not necessarily like "insurance" in the conventional sense. View some of our real customers, and their stories, in this 6-minute video playlist of testimonials, which opens in a new tab.

-You sign up and pay (average cost $20/month)

-The earthquake happens

-We link data from the USGS with our technology to determine who's eligible for payout

-We text you to tell you you're eligible

-You reply yes

-We initiate electronic payout to your account on file

The full list of product FAQs is on our website.

Invest in the app